Monday, October 15, 2018

Are published oil price forecasts efficient?

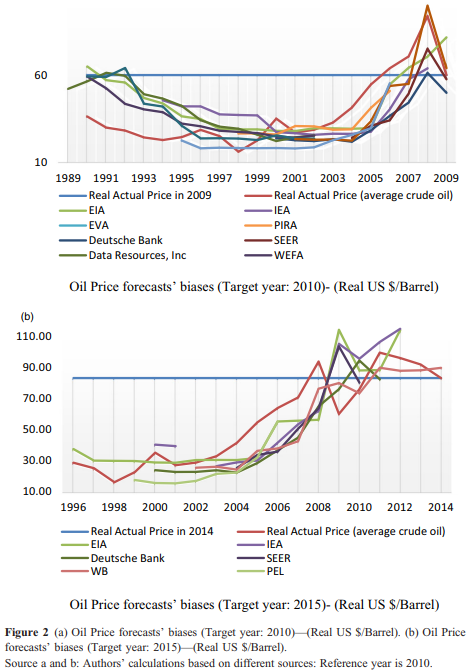

A new paper assesses “the accuracy and efficiency of crude oil price forecasts published by different organisations, think tanks and companies. Since the sequence of published forecasts appears as smooth, the weak efficiency criterion is clearly violated. Even combining forecasts, cannot increase efficiency due to high correlation among various forecasts. This pattern of oil price forecasts can be attributed to combining myopia (use current oil price levels as a basis) with Hotelling-type exponential growth. Another behavioural explanation in source of inefficiencies is that forecasters prefer to harmonise their forecasts with other forecasters in order to be not an outlier.”

A new paper assesses “the accuracy and efficiency of crude oil price forecasts published by different organisations, think tanks and companies. Since the sequence of published forecasts appears as smooth, the weak efficiency criterion is clearly violated. Even combining forecasts, cannot increase efficiency due to high correlation among various forecasts. This pattern of oil price forecasts can be attributed to combining myopia (use current oil price levels as a basis) with Hotelling-type exponential growth.

Posted by at 10:19 AM

Labels: Forecasting Forum

Friday, October 12, 2018

Housing View – October 12, 2018

On cross-country:

- Book: Housing Bubbles – SpringerLink

On the US:

- Mortgage Lending and Housing Markets – NBER

- Dark clouds gather over the US housing market – Financial Times

- 10 years later: How the housing market has changed since the crash – Washington Post

- The Housing Bust Widened the Wealth Gap. Here’s How. – Zillow

- Homeless in US: A deepening crisis on the streets of America – BBC

- Low mortgage rates and securitization: A distinct perspective on the U.S. housing boom – Brunel University of London

- Housing Sentiment Dips Slightly on Interest Rate Concerns – Fannie Mae

- 2018 Cost Burden Report: Despite improvements, affordability issues are immense – Apartment List

On other countries:

- [China] Angry Mobs Show All’s Not Well in China’s Property Sector – Bloomberg

- [Hong Kong] An Early Warning Sign for the World’s Priciest Homes Is Flashing Sell – Bloomberg

- [United Kingdom] What determines UK housing equity withdrawal in later life? – Regional Science and Urban Economics

Photo by Aliis Sinisalu

On cross-country:

- Book: Housing Bubbles – SpringerLink

On the US:

- Mortgage Lending and Housing Markets – NBER

- Dark clouds gather over the US housing market – Financial Times

- 10 years later: How the housing market has changed since the crash – Washington Post

- The Housing Bust Widened the Wealth Gap.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, October 11, 2018

Inequality in and across Cities

From a new article by Jessie Romero and Felipe F. Schwartzman at the Richmond Fed:

“Inequality in the United States has an important spatial component. More-skilled workers tend to live in larger cities where they earn higher wages. Less-skilled workers make lower wages and do not experience similar gains even when they live in those cities. This dynamic implies that larger cities are also more unequal. These relationships appear to have become more pronounced as inequality has increased. The evidence points to externalities among high-skilled workers as a significant contributor to those patterns.”

“A large body of research has identified several key facts about inequality across and within cities. First, larger cities have a greater concentration of high-skilled workers. In the Fifth District, for example, the share of the population over age twenty-five with a bachelor’s degree is 45 percent in the most urban areas, compared with 16 percent in the most rural areas. In the United States as a whole, the proportion ranges from 35 percent in the most urban areas to 17 percent in the most rural areas.”

“Second, nominal wages are higher in larger cities and in cities with a larger proportion of high-skilled workers. In the most urban areas of the Fifth District, average annual pay in 2016 was nearly $64,000; in the most rural areas, it was less than $35,000. Nationwide, workers in the most urban areas earned about $60,000 on average in 2016, while workers in the most rural areas earned about $36,000. (See Figure 2 above.) In recent research, Nathaniel Baum-Snow, Matthew Freedman, and Ronni Pavan find that nominal wages increase 0.065 percent for every percentage point increase in city size (based on data from 2005–07). They also find that the relationship between city size and wages has strengthened over time and that the wage gap between urban and rural areas has increased”

From a new article by Jessie Romero and Felipe F. Schwartzman at the Richmond Fed:

“Inequality in the United States has an important spatial component. More-skilled workers tend to live in larger cities where they earn higher wages. Less-skilled workers make lower wages and do not experience similar gains even when they live in those cities. This dynamic implies that larger cities are also more unequal. These relationships appear to have become more pronounced as inequality has increased.

Posted by at 5:59 PM

Labels: Inclusive Growth

Wednesday, October 10, 2018

Why Has the Stock Market Risen So Much Since the US Presidential Election?

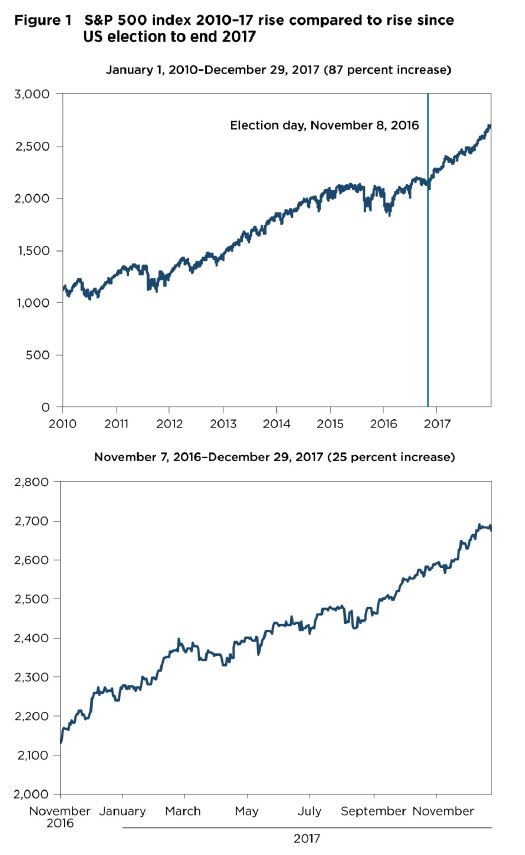

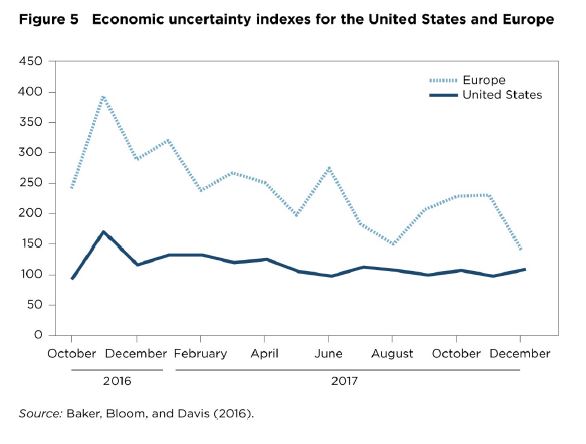

From a new paper by Olivier Blanchard, Christopher G. Collins, Mohammad R. Jahan-Parvar, Thomas Pellet, and Beth Anne Wilson:

“This paper looks at the evolution of U.S. stock prices from the time of the Presidential elections to the end of 2017. It concludes that a bit more than half of the increase in the aggregate U.S. stock prices from the presidential election to the end of 2017 can be attributed to higher actual and expected dividends. A general improvement in economic activity and a decrease in economic policy uncertainty around the world were the main factors behind the stock market increase. The prospect and the eventual passage of the corporate tax bill nevertheless played a role. And while part of the rise in stock returns came from a decrease in the equity risk premium, this decrease was relatively limited and returned the premium to the levels of the first half of the 2000s.”

From a new paper by Olivier Blanchard, Christopher G. Collins, Mohammad R. Jahan-Parvar, Thomas Pellet, and Beth Anne Wilson:

“This paper looks at the evolution of U.S. stock prices from the time of the Presidential elections to the end of 2017. It concludes that a bit more than half of the increase in the aggregate U.S. stock prices from the presidential election to the end of 2017 can be attributed to higher actual and expected dividends.

Posted by at 4:11 PM

Labels: Macro Demystified

Tuesday, October 9, 2018

Georgia: Residential Property Price Index

From the IMF’s latest report on Georgia:

“The compilation of an RPPI will facilitate the assessment of developments and risks in property markets. It will therefore be useful for monetary policy as it will improve the understanding of the linkages between property asset prices and financial assets. The National Bank of Georgia compiles a rudimentary index that tracks residential and commercial property prices in two districts of Tbilisi—one is known for expensive properties and the other for modestly priced properties. The index is therefore quite limited and is not disseminated.

On the RPPI, the mission proposed that, as a start, the index be restricted to the capital city and cover all transactions in new apartments and houses. Initially, the index will not include transactions in existing dwellings because of the complexity in covering these dwellings. Existing dwellings may be covered at a later stage when the RPPI methodology is stabilized and the staff gain the experience and skills in compiling the index.

Geostat should be able to compile the RPPI on a quarterly basis and disseminate the first index for the first quarter of 2021, in mid-May 2021. The RPPI will be developed by the same staff compiling the CPI; however, the production schedule for the RPPI can be arranged around the production and release schedule for the CPI to accommodate the available staff

resources. Based on the current CPI production schedule and the proposed RPPI development plan, additional staff would not be required.The most suitable data source for the RPPI may be the National Agency of Public Registry of Ministry of Justice (NAPR). Geostat informed the mission that it is compulsory to

register all transactions in dwellings with the NAPR. Therefore, the NAPR may collect information on transaction value, transactors, dwelling specifications, and location. An alternative source would be the two main websites for real estate transactions.”

From the IMF’s latest report on Georgia:

“The compilation of an RPPI will facilitate the assessment of developments and risks in property markets. It will therefore be useful for monetary policy as it will improve the understanding of the linkages between property asset prices and financial assets. The National Bank of Georgia compiles a rudimentary index that tracks residential and commercial property prices in two districts of Tbilisi—one is known for expensive properties and the other for modestly priced properties.

Posted by at 1:37 PM

Labels: Global Housing Watch

Subscribe to: Posts