Thursday, September 13, 2018

Housing Market Developments in Austria

The IMF’s latest report on Austria says:

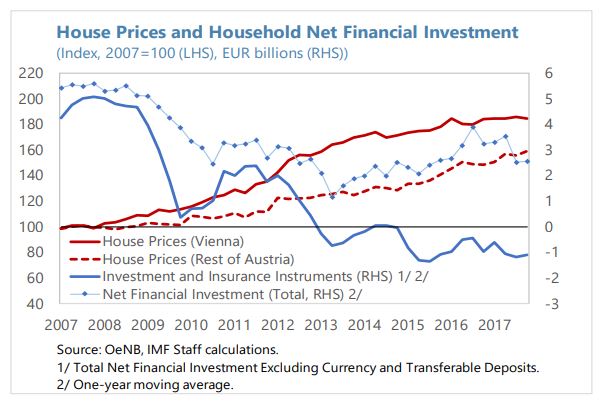

“The Austrian housing market has shown a strong trend rise in valuations over the last decade, mainly driven by price increases in Vienna. Prices stagnated through the mid-2000s

but have since outpaced most of Austria’s EU peers. In September 2016, the ESRB issued Austria a warning on medium-term residential real estate vulnerabilities because of the robust price and credit growth and the risk of further loosening in credit standards. Recently, price growth moderated to 4.7 percent (y/y) at end-2017, due to a slowdown in Vienna, though prices accelerated in the rest of the country.”

While the robust price growth has largely reflected underlying market fundamentals, the nationwide market has recently started to show signs of modest overvaluation. Housing demand has been buoyed by demographic factors, including the spike in immigration in 2015–16, and low interest rates which also have increased the attractiveness of housing assets as a form of saving. Supply-side constraints, such as land availability, have also played a role, despite some recent pickup in construction activity. The OeNB’s fundamentals indicator for residential property prices suggests a modest overvaluation of around 10 percent for Austria in 2017 (and a larger overvaluation for Vienna of about 20 percent), broadly corresponding to a range of ECB indicators as of end-2017.

Real estate related financial stability risks are nonetheless contained. The rise in mortgage debt in Austria has been modest compared to other EU countries experiencing large property price increases, and its share relative to households’ incomes has remained stable and among the lowest in the Euro Area. Residential real estate exposures account for only about a fifth of Austrian banks’ total loan stock and about 150 percent of consolidated CET-1 capital. Furthermore, the prevalence of rental accommodation (about half and three-quarters of housing nationwide and in Vienna, respectively) shield a large share of the population from adverse price developments. Less than half of homeowners have outstanding mortgages, and they also typically have higher incomes and net wealth relative to the rest of the population.

Some pockets of vulnerability and early signs of increasing risks nonetheless warrant continued close monitoring. The share of foreign exchange denominated housing loans at around

15 percent remains high relative to Austria peers, although it has declined significantly in recent years. Furthermore, the recent prolonged period of low lending rates saw a significant increase in the share of variable interest rate mortgages, which despite a recent decline still amount to about three-quarters of the total stock. There are also signs of some easing in banks’ lending standards, with a rising—albeit still limited—share of relatively high loan-to-value, debt service-to-income, and debt-to-income ratios in new housing loans to households.Supply side measures could help ease the modest price imbalances over time, while the recently expanded macroprudential toolkit can help prevent a build-up of systemic risks.

Measures to address supply-side constraints could include reviewing zoning regulations and other restrictions on construction. Addressing outdated property tax valuations could help improve residential mobility and market efficiency. At the same time, the new real-estate specific macroprudential policy tools provide additional scope for tailored preventive measures to ensure systemic risks arising from the mortgage market remain contained. These are accompanied by new reporting requirements, expected to be introduced in 2019, to facilitate evaluation of risks and impact of potential policy changes. They also complement a 2016 call by the Financial Market Stability Board for the Austrian banks to maintain sustainable lending standards, although the guidance does not specify quantitative limits for the vulnerability ratios.”

The IMF’s latest report on Austria says:

“The Austrian housing market has shown a strong trend rise in valuations over the last decade, mainly driven by price increases in Vienna. Prices stagnated through the mid-2000s

but have since outpaced most of Austria’s EU peers. In September 2016, the ESRB issued Austria a warning on medium-term residential real estate vulnerabilities because of the robust price and credit growth and the risk of further loosening in credit standards.

Posted by at 10:57 AM

Labels: Global Housing Watch

House Prices in Portugal

The IMF’s new report on Portugal says:

“Housing prices continue to increase, but there is no significant overvaluation yet. Following a decline of 18 percent in real terms over 2010–13, housing prices have since increased by

about 20 percent in real terms (7.9 percent in 2017), especially in Lisbon, Porto and the Algarve region. While the increases have been driven largely by transactions on existing dwellings by non-residents, the share of housing transactions financed by Portuguese mortgages has been growing since 2015 (reaching 41 percent in the last quarter of 2017). Estimates in the ECB’s May 2018 Financial Stability Review suggest that there are incipient signs of overvaluation in the residential real estate market. The authorities should continue to improve the quality of real estate data and related analytical tools, and to monitor mortgage markets and the evolution of risks to banks from developments in real estate markets.”

The IMF’s new report on Portugal says:

“Housing prices continue to increase, but there is no significant overvaluation yet. Following a decline of 18 percent in real terms over 2010–13, housing prices have since increased by

about 20 percent in real terms (7.9 percent in 2017), especially in Lisbon, Porto and the Algarve region. While the increases have been driven largely by transactions on existing dwellings by non-residents, the share of housing transactions financed by Portuguese mortgages has been growing since 2015 (reaching 41 percent in the last quarter of 2017).

Posted by at 10:44 AM

Labels: Global Housing Watch

Wednesday, September 12, 2018

Carbon Taxation for International Maritime Fuels: Assessing the Options

From a new IMF working paper by Ian Parry, Dirk Heine, Kelley Kizzier, and Tristan Smith:

“The International Maritime Organization (IMO) announced in April 2018 a target of cutting greenhouse gas (GHG) emissions from the sector by 50 percent below 2008 levels by 2050

and subsequent meetings of the IMO will develop a strategy for making headway on this commitment. This paper seeks to inform dialogue about the possibility of a carbon tax as a

key element of GHG mitigation policy for international maritime transport. The paper discusses the case for the tax over alternative mitigation instruments, options for the practical

design issues, and then presents estimates of the impacts of carbon taxation and other instruments from an analytical model of the maritime sector.”

From a new IMF working paper by Ian Parry, Dirk Heine, Kelley Kizzier, and Tristan Smith:

“The International Maritime Organization (IMO) announced in April 2018 a target of cutting greenhouse gas (GHG) emissions from the sector by 50 percent below 2008 levels by 2050

and subsequent meetings of the IMO will develop a strategy for making headway on this commitment. This paper seeks to inform dialogue about the possibility of a carbon tax as a

key element of GHG mitigation policy for international maritime transport.

Posted by at 9:59 AM

Labels: Energy & Climate Change

Friday, September 7, 2018

New Evidence that Unions Raise Wages for Less-Skilled Workers

From a new post by Steve Maas:

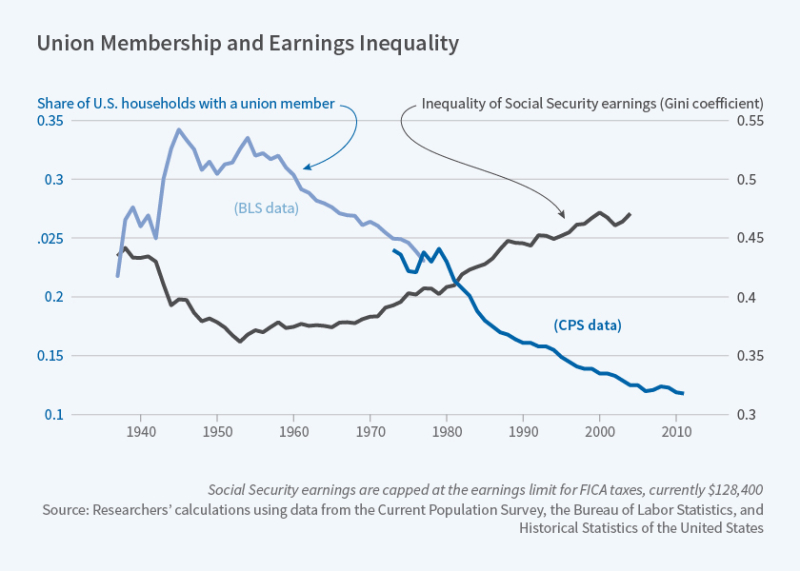

“New Evidence that Unions Raise Wages for Less-Skilled Workers: Tapping into eight decades of private and public surveys, a new study finds evidence that unions have historically reduced income inequality.

For Unions and Inequality over the Twentieth Century: New Evidence from Survey Data (NBER Working Paper No. 24587), Henry S. Farber, Daniel Herbst, Ilyana Kuziemko, and Suresh Naidu assembled a household-level database on union membership dating back to 1936.

The U.S. Bureau of the Census has tracked wages and education consistently since 1940. Aggregate data on union membership goes back to the early 20th century, but data on individual workers were not readily available until the Census Bureau started asking about union affiliation in 1973. By that time, unions were already in decline, and higher-skilled workers accounted for an increasing share of their membership.

The researchers draw on more than 500 surveys conducted by Gallup and other pollsters from 1936 through 1986, extending their dataset into the present day with information from government surveys and other sources.

Their study finds that the salary premium for union members compared to workers with comparable skills and demographic characteristics has remained relatively steady over the last 80 years despite large swings both in the overall number of union members and in their education levels. The less skilled the workers were, the greater the wage premium associated with their union membership. The researchers find a negative correlation between unionization rates and measures of inequality such as the Gini coefficient.

Between 1940 to 1970, when unionization peaked and income inequality narrowed, unions were drawing in the least-skilled workers. Before and after that period, unions were smaller and a higher fraction of their members were drawn from the ranks of high-skill workers. The 1940 – 1970 period also coincided with the highest share of union members drawn from minority groups.

The clear implication of the researchers’ analysis is that, because unions offer a larger wage premium to less-skilled workers, unions have an important equalizing effect on the income distribution to the extent that they are successful in organizing the less-skilled. Recent decades have seen growth in educational attainment in the workforce, and, importantly, not only has the overall share of workers who are unionized declined, but unions have also become relatively less successful in organizing less-skilled workers. The remaining unionized workforce is more highly educated than it was earlier. The combination of the declining presence of unions in the labor market and the increased skill level of the remaining union workers means that the important equalizing effect of unions on the income distribution that was seen in the middle of the 20th century has diminished substantially.”

From a new post by Steve Maas:

“New Evidence that Unions Raise Wages for Less-Skilled Workers: Tapping into eight decades of private and public surveys, a new study finds evidence that unions have historically reduced income inequality.

For Unions and Inequality over the Twentieth Century: New Evidence from Survey Data (NBER Working Paper No. 24587), Henry S. Farber,

Posted by at 12:45 PM

Labels: Inclusive Growth

A Shorter Work Week?

From a new Conversable Economist post by Timothy Taylor:

“The biggest European union has managed to achieve a long-standing goal: German metal-workers can now work a 28-hour week, if they wish. […] What do German employers get out of this deal? They get flexibility, in the sense that if some workers want to work longer hours, the firm can hire them to do so. Furthermore, Pencavel argues that for many workers, labor exhibits diminishing marginal productivity over the work-week: that is, the 25th hour worked in a week is on average more productive than the 35th or the 45th hour worked. Thus, employers will be getting the more productive hours from workers, for the same hourly pay.”

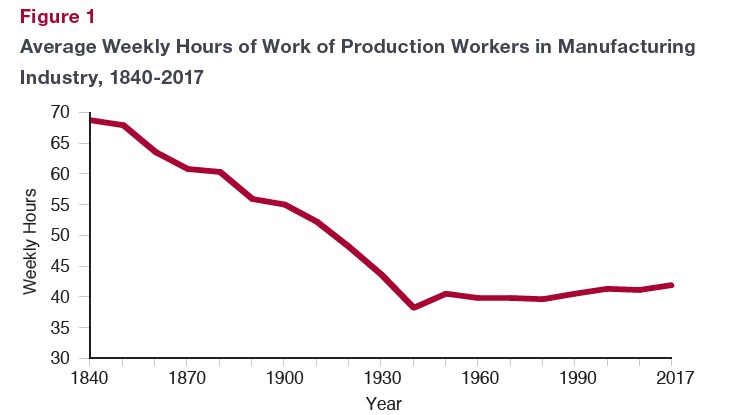

“Does a drive for lower hours have any resonance in the US economy? Pencavel points out that in the US labor market, weekly hours worked dropped sharply in the decades leading up to 1930 or so, but since then, the decline has largely stopped. (And for the record, American unions in certain induistries remained quite powerful in the 1950s and 1960s, and they might well have succeeded in pushing for lower weekly hours if it had been a priority for them.)”

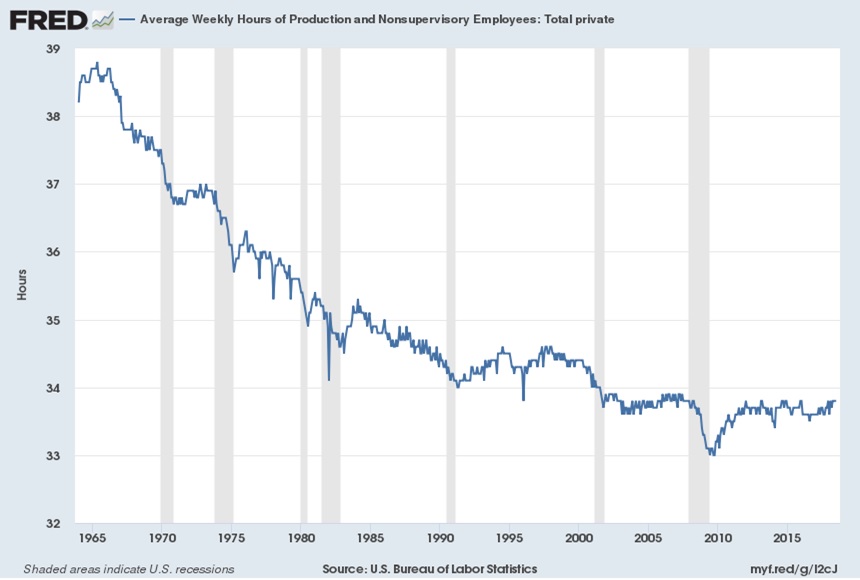

“Here’s a different figure, not from Pencavel’s brief, showing average weekly hours for production and nonsupervisory workers in all industries, not just manufacturing. This average includes part-timers. This shows an ongoing drop over time, although it may have levelled out around the year 2000. Specifically: “Average weekly hours relate to the average hours per worker for which pay was received and is different from standard or scheduled hours. Factors such as unpaid absenteeism, labor turnover, part-time work, and stoppages cause average weekly hours to be lower than scheduled hours of work for an establishment. … Average weekly hours are the total weekly hours divided by the employees paid for those hours.””

“It’s an interesting Labor Day question as to how many US workers would we willing to make the tradeoff of lower hours for less total income (assuming they would not see diminished job security as a result). From a US context, one interesting pattern is that lower-wage workers used to be the ones who on average worked the longest hours, but now it’s higher-wage workers. “

From a new Conversable Economist post by Timothy Taylor:

“The biggest European union has managed to achieve a long-standing goal: German metal-workers can now work a 28-hour week, if they wish. […] What do German employers get out of this deal? They get flexibility, in the sense that if some workers want to work longer hours, the firm can hire them to do so. Furthermore, Pencavel argues that for many workers,

Posted by at 11:29 AM

Labels: Inclusive Growth

Subscribe to: Posts