Friday, March 24, 2023

Housing View – March 24, 2023

On cross-country:

- The Anglosphere needs to learn to love apartment living. Housebuilding rates in English-speaking states have fallen behind the rest of the developed world – FT

- Credit Suisse Brings US Bank Panic Home for European Real Estate. Investors worry about contagion at annual Cannes conference. Concern over rates and further turmoil chills property lending – Bloomberg

- Where High Interest Rates Have Sent Home Prices Sliding. In Sweden, the central bank’s fight against inflation is crimping economic growth and has contributed to a 15 percent drop in home prices. – New York Times

- 2023 Demographia International Housing Affordability Survey – Demographia

On the US—developments on house prices, rent, permits and mortgage:

- February Housing Starts: Housing Starts Increase More Than Expected As Builder Confidence Edged Higher. The increase in builder confidence and housing starts are signs housing demand is thawing from last year’s deep freeze. – Zillow

- U.S. single-family housing starts, building permits rebound in February – Reuters

- NAHB 2023 “Priced Out” Estimates – State and Local Estimates – NAHB

- House Prices: Rust or Bust? It is possible the Median House Price will be Down YoY in February – Calculated Risk

- Home Prices Inched Up in February, as Some Home Shoppers Braved the Gauntlet of Low Inventory and High Mortgage Rates (February 2023 Market Report) – Zillow

On the US—other developments:

- How the Housing Market Could Be Affected by Bank Failures – Barron’s

- US mortgage market suffers fallout from bank failures. Volatility in bonds and stocks has left lenders on sidelines of $11tn home loans-backed securities market – FT

- Black-White Homeownership Gap Narrows During Pandemic – Zillow

- Lawler: Early Read on Existing Home Sales in February. 3rd Look at Local Housing Markets in February – Calculated Risk

- California Wildfires, Property Damage, and Mortgage Repayment – Philadelphia Fed

- Households Priced Out by Higher Interest Rates – NAHB

- NAR: Existing-Home Sales Increased to 4.58 million SAAR in February; Median Prices Declined YoY. Median Prices Down 12.3% from Peak in June 2022 – Calculated Risk

- Existing Home Sales Surged in February – NAHB

- New Home Sales at 640,000 Annual Rate in February – Calculated Risk

On China:

- China Real Estate Showing Signs of Recovery After Slump. Home sales, prices snapped losing streak of more than a year. Investment continued to fall but at a much slower pace – Bloomberg

- Long-run mechanism for house price regulation in China: Real estate tax, monetary policy or macro-prudential policy? – IDEAS

- Measuring real estate policy uncertainty in China – China Economic Quarterly International

On other countries:

- [Mexico] Mexico’s housing market improving gradually – Global Property Guide

- [Netherlands] Netherlands’ house prices are now falling rapidly – Global Property Guide

- [Turkey] Turks Are Latest to Rebel Over Foreigners Buying Homes, Want Ban – Bloomberg

- [United Kingdom] UK Property Sellers Lift Asking Prices Despite Worry About Slump. Rightmove survey indicates strength in the UK housing market. Some indicators show housing market is headed for a decline – Bloomberg

On cross-country:

- The Anglosphere needs to learn to love apartment living. Housebuilding rates in English-speaking states have fallen behind the rest of the developed world – FT

- Credit Suisse Brings US Bank Panic Home for European Real Estate. Investors worry about contagion at annual Cannes conference. Concern over rates and further turmoil chills property lending – Bloomberg

- Where High Interest Rates Have Sent Home Prices Sliding.

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, March 17, 2023

Housing View – March 17, 2023

On cross-country:

- Global house prices set to extend declines, risk of more with higher rates: Reuters poll – Reuters

On the US—developments on house prices, rent, permits and mortgage:

- Three Million U.S. Households Making Over $150,000 Are Still Renting. High cost of homeownership and limited supply of homes for sale drive renters – Wall Street Journal

- House Prices and Rents in the 21st Century – NBER

- Rent control policies are gaining support nationwide. Here’s why economists still think it’s a bad idea. – CNBC

- A Short History of Long-Term Mortgages. Americans take today’s selection of mortgages for granted, but financing a home is a much different experience than it was a century ago – Richmond Fed

- Mortgage Payments Hit Record High. The typical homebuyer’s monthly bill rose to $2,563 this week thanks to higher borrowing costs and prices that remain elevated. – Bloomberg

- Permits Decline At The Start of 2023 – NAHB

- Single-Family Starts Remain Lackluster but Will Rebound Later This Year – NAHB

- February Housing Starts: Average Length of Time from Start to Completion increased Sharply in 2022. Near Record Number of Housing Units Under Construction in February 2023 – Calculated Risk

On the US—other developments:

- President Biden’s Budget Lowers Housing Costs and Expands Access to Affordable Rent and Home Ownership – White House

- Zillow’s panel of experts: Fix zoning to improve housing affordability – Zillow

- Why There Are No Houses to Buy in Many U.S. Metro Areas – Time

- ‘Stalemate’: Sellers aren’t selling, and buyers aren’t buying. Rising interest rates are locking up Boston’s housing market. Nearly everyone who currently holds a 30-year fixed rate mortgage has an interest lower than they could get today. So why sell? – Boston.com

- Forum on the future of the Federal Home Loan Bank system: Highlights from the Brookings and BU Law event – Brookings

- Pandemic Economics, Housing and Monetary Policy: Part 2 – Calculated Risk

- 2nd Look at Local Housing Markets in February. Early reports suggest NAR reported sales will rebound in February – Calculated Risk

- 10 States With The Most Valuable Housing Markets. California remains the clear leader, and Florida surpassed New York as the state with the second most valuable real estate market in the country. – Zillow

- What Employers Can Do to Address High Housing Costs – Harvard Business Review

- Despite Multiple States Abolishing Single-Family-Only Zoning, Very Few Duplexes and Triplexes Are Being Built. A new report illustrates that the middle of the housing market is still missing. – Reason

- Current State of the Housing Market; Overview for mid-March. Purchasing Same House, Monthly Payments Up 44% Year-over-year – Calculated Risk

On other countries:

- [Canada] Canada’s housing market continues to lose steam – Global Property Guide

- [Hong Kong] Hong Kong’s house prices plummeting – Global Property Guide

- [Netherlands] ‘How will I buy?’: housing crisis grips the Netherlands as Dutch go to polls. Housing is key in this week’s provincial elections after years of soaring prices and government neglect – The Guardian

- [New Zealand] New Zealand house prices fall in February as economic headwinds continue – Reuters

- [Sweden] Sweden faces recession as housing market troubles take toll on economy – Reuters

- [United Arab Emirates] Dubai Housing Boom Shows No Sign of Slowing as Prices Jump Again. Average Dubai villa rents jump 26% in the year to February. The number of off-plan property sales are also increasing – Bloomberg

- [United Kingdom] Is the UK housing market cooling? Agents and analysts agree that there is a shift after two years of superheated growth – FT

On cross-country:

- Global house prices set to extend declines, risk of more with higher rates: Reuters poll – Reuters

On the US—developments on house prices, rent, permits and mortgage:

- Three Million U.S. Households Making Over $150,000 Are Still Renting. High cost of homeownership and limited supply of homes for sale drive renters – Wall Street Journal

- House Prices and Rents in the 21st Century – NBER

- Rent control policies are gaining support nationwide.

Posted by at 5:00 AM

Labels: Uncategorized

Thursday, March 16, 2023

Housing Market in Sweden

From the IMF’s latest report on Sweden:

“The real estate market is experiencing substantial weakening. Mortgage and CRE borrowing grew strongly during the pandemic. Like in other advanced countries, house prices were fueled by the easing of monetary policy and macroprudential regulation, fiscal support, and a change in dwelling preferences towards larger units. Both residential real estate (RRE) prices and total household debt in relation to income peaked in Q4 2021. RRE prices started to decline in the second half of 2022, registering a 16 percent decline by end-year from their March peak. Shares of CRE firms listed in Stockholm have lost more than 40 percent of their value in 2022, and more companies face the risk of downgrades spurred by their deteriorating debt profiles as they need to rollover maturing bonds at higher interest rates

(…)

Limited reforms are taking place to address housing market distortions. Recent actions focused mainly on the supply side of the market through providing investment subsidies for rental and student housing, shortening planning processes, and simplifying permits application. These reforms should be supplemented with lowering taxes on deferred capital gains, a gradual removal of interest rate deductibility, and increasing the extremely low property taxes (Annex VII; Box 4). In lieu of the tax breaks, social protection could be provided in a more efficient way, including through expanding the housing allowance. Easing rental controls and simplifying building codes is also vital to bringing more dynamism to the market.”

Also see a special chapter on “Sweden’s Corporate Vulnerabilities: A Focus on Commercial Real Estate“, and Sweden’s Financial System Stability Assessment report.

From the IMF’s latest report on Sweden:

“The real estate market is experiencing substantial weakening. Mortgage and CRE borrowing grew strongly during the pandemic. Like in other advanced countries, house prices were fueled by the easing of monetary policy and macroprudential regulation, fiscal support, and a change in dwelling preferences towards larger units. Both residential real estate (RRE) prices and total household debt in relation to income peaked in Q4 2021.

Posted by at 10:46 AM

Labels: Global Housing Watch

Friday, March 10, 2023

Housing View – March 10, 2023

On the US—developments on house prices, rent, permits and mortgage:

- U.S. home prices to fall 4.5% in 2023 despite higher rates: Reuters poll – Reuters

- Inflation Adjusted House Prices 3.9% Below Peak. Price-to-rent index is 7.1% below recent peak – Calculated Risk

- Black Knight Mortgage Monitor: Home Prices Declined in January, “on pace to fall below 0% by March/April”. Home Prices Off 5.5% from Peak NSA, Prices up 3.4% Y – Calculated Risk

- 1st Look at Local Housing Markets in February. Closed Sales: 18th consecutive month with a YoY decline – Calculated Risk

- Sorry, Fed, Most US Mortgage Rates Were Locked In During Pandemic Lows – Bloomberg

- Mortgage Activity Increases Despite Mortgage Rate Volatility – NAHB

- House Prices and Rents in the 21st Century – Boston Fed

- Boston Advances Rent-Control Measure as Costs Climb. State must sign off on mayor’s plan to combat surging housing costs – Wall Street Journal

On the US—other developments:

- In Most US Cities, Homes Still Sell Faster Than Before the Pandemic – Bloomberg

- Black-White Homeownership Gap Widened During Pandemic – Wall Street Journal

- Everything you think you know about homelessness is wrong – Noahpinion

- Yes, There’s a Housing Crisis. No, You Can’t Build Here. A modest redevelopment proposal meets Nimby resistance in my ‘quirky’ suburban Virginia neighborhood. – Wall Street Journal

- Foreign Buyers, Who Nearly Disappeared During Covid, Finally Return to the U.S. Housing Market. Real-estate agents say they’ve seen an acceleration in purchases by overseas buyers amid looser Covid restrictions and political-economic shifts abroad – Wall Street Journal

- Americans Need to Be Richer Than Ever to Buy Their First Home. The pandemic boom has given way to higher mortgage rates and tight inventory, further squeezing entry-level house hunters. – Bloomberg

- Housing Market Momentum Stalls as Critical Spring Season Approaches. Rising interest rates squeeze affordability, drive mortgage applications to lowest levels in decades – Bloomberg

- Housing Market Momentum Stalls as Critical Spring Season Approaches. Rising interest rates squeeze affordability, drive mortgage applications to lowest levels in decades – Wall Street Journal

- Is Spring the Make-or-Break Moment for 2023’s Housing Market? A Brutally Honest Look Ahead for Buyers, Sellers – Realtor.com

- Pandemic Economics, Housing and Monetary Policy: Part I. The Economic Fireworks have been in Housing! – Calculated Risk

- Single-Family Market Share Continues to Shift from Large Population Centers – NAHB

- Housing Sentiment Returns to Near-Survey Low Amid Affordability Constraints and Job Security Concerns. Both Homebuyers and Home-Sellers Express Caution About Current Market Conditions – Fannie Mae

- Cost of Constructing a Home in 2022 – NAHB

- Housing Advocates Urge Congress to Enact Tax Policies for New Homebuyers – Reuters

On China:

- China’s Property Recovery Is Held Back by Hesitant Buyers. Second-hand home viewings have jumped 86% in big cities. Weakening expectations over housing prices remains overhang – Bloomberg

- China to guard against risks among property developers – Premier Li – Reuters

- China to Target ‘Unregulated’ Expansion in Property Market. Premier Li calls for risk prevention in major developers. China sets modest growth target as economic headwinds persist – Bloomberg

- Property Shares Fall After China Targets ‘Unregulated’ Expansion. Premier Li calls for risk prevention in major developers. China sets modest growth target as economic headwinds persist – Bloomberg

- Land Supply and House Prices in China – Applied Economics Letters

On other countries:

- [Australia] Is the auction market causing a false dawn for property prices? – The Sydney Morning Herald

- [India] India housing market to remain resilient despite higher interest rates: Reuters poll – Reuters

- [Singapore] Will Singapore’s housing supply rise amid rising interest rates, recession fears and tightening wallets? Supply has dropped since 2018, and rental market is expected to remain tight despite about 30,000 potential completions forecast for the next two years. Singapore developers are still grappling with high costs, shortage of labour thanks to the upheavals in supply chains caused by pandemic, analysts note – South China Morning Post

- [Sweden] Sweden Housing Market Takes a Break From Worst Rout in Years. Apartment prices rise for the first time since March 2022. Sales volumes continue to be subdued, Maklarstatistik says – Bloomberg

- [United Kingdom] Falling house prices may seem like a good thing – but it’s renters who are paying the price. With first-time buyers unable to get a mortgage and landlords hiking up rents, it’s a vicious cycle – The Guardian

- [United Kingdom] UK house prices bounce unexpectedly in February: Halifax – Reuters

- [United Kingdom] Are UK House Prices Rebounding Already? The latest Halifax data is much more upbeat than we’ve grown used to in recent months. – Bloomberg

- [United Kingdom] UK house prices slide further but market pessimism eases: RICS – Reuters

On the US—developments on house prices, rent, permits and mortgage:

- U.S. home prices to fall 4.5% in 2023 despite higher rates: Reuters poll – Reuters

- Inflation Adjusted House Prices 3.9% Below Peak. Price-to-rent index is 7.1% below recent peak – Calculated Risk

- Black Knight Mortgage Monitor: Home Prices Declined in January, “on pace to fall below 0% by March/April”. Home Prices Off 5.5% from Peak NSA,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, March 9, 2023

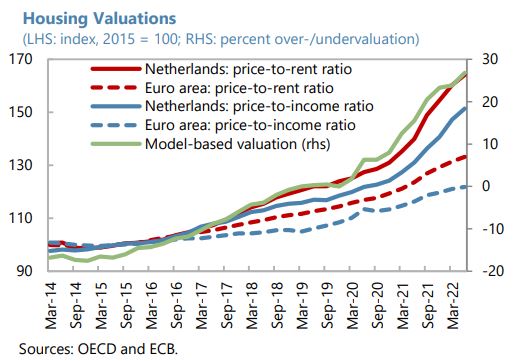

Housing Market in Netherlands

From the IMF’s latest report on Netherlands:

“Credit has grown at a robust pace, but the phase out of monetary accommodation has contributed to tighter financial conditions and the cooling of a buoyant housing market. Mortgage lending has expanded at a brisk rate (…), reflecting strong housing demand, yet prices for homes have recently started to decline, falling 2 percent below their July 2022 peak. Echoing the scaling back of monetary accommodation, interest rates for housing and corporate loans have started to rise from historic lows. At the same time, banks have tightened credit standards, primarily on the back of deteriorating risk perceptions due to an uncertain economic outlook.”

(…)

“The cooling of a richly valued housing market calls for ongoing alertness towards emerging strains and readiness to deploy existing buffers if needed. Recently flagging house price momentum accentuates vulnerabilities from a residential real estate sector deemed overvalued on a broad range of measures (…). Household indebtedness, at more than 100 percent of GDP, is among the highest in the euro area while a large part of assets is concentrated in (illiquid) pension and insurance claims (…). With house prices acting as a potential amplifier, this raises the risk of borrower distress in the event of an economic downturn, although the large share of fixed-rate mortgages (more than 90 percent of the total) and long maturities (typically 30 years) provides some comfort. Still, vulnerabilities are heightened by about a quarter of outstanding mortgages facing an interest rate reset in the coming five years, overextended balance sheets of recent home buyers, a prevalence of interest-only mortgages (around two fifths of the total), and debt service to income ratios (DSTIs) becoming more binding for new mortgages due to rising interest rates. In this context, maintaining minimum risk weight floors for mortgage loans (activated in January 2022) until December 1, 2024, is appropriate as it helps stabilize the housing cycle and preserves buffers that should be released to absorb credit losses in the event of a more severe housing market downturn. Likewise, efforts to increase awareness about the risks from interest-only lending among borrowers and lenders are welcome. Structurally, the Dutch housing market remains unbalanced, requiring determined policy intervention. Policy measures should strive to lessen incentives for households to live in highly leveraged, owner-occupied housing. The government’s program to address housing shortages and ensure affordability contain important elements to tackle underlying imbalances but means-testing for social housing eligibility could be strengthened and the need for expansive rent control should be re-evaluated.”

From the IMF’s latest report on Netherlands:

“Credit has grown at a robust pace, but the phase out of monetary accommodation has contributed to tighter financial conditions and the cooling of a buoyant housing market. Mortgage lending has expanded at a brisk rate (…), reflecting strong housing demand, yet prices for homes have recently started to decline, falling 2 percent below their July 2022 peak. Echoing the scaling back of monetary accommodation,

Posted by at 10:37 AM

Labels: Global Housing Watch

Subscribe to: Posts