Sunday, October 2, 2022

A Tale of Tier 3 Cities

From a new IMF working paper by Kenneth Rogoff and Yuanchen Yang:

“This paper provides new estimates of the housing stock, construction rates and price developments by city tier in China in order to understand where imbalances might be concentrated, and the implications of any significant contraction. We also update estimates of the size of China’s rapidly evolving real estate sector through 2021, allowing one to look at the initial impact of COVID-19, as well as extending the analysis to incorporate urban-expansion related infrastructure construction. We argue that China overall faces imbalances between supply and demand for housing stock, but the problem is significantly deeper outside tier 1 cities.”

From a new IMF working paper by Kenneth Rogoff and Yuanchen Yang:

“This paper provides new estimates of the housing stock, construction rates and price developments by city tier in China in order to understand where imbalances might be concentrated, and the implications of any significant contraction. We also update estimates of the size of China’s rapidly evolving real estate sector through 2021, allowing one to look at the initial impact of COVID-19,

Posted by at 6:32 PM

Labels: Global Housing Watch

Friday, September 30, 2022

Housing View – September 29, 2022

On cross-country:

- How long can the super-prime property boom continue? The super-rich seem to have been largely unaffected by rising mortgage rates, spiralling inflation and the threat of recession — so far – FT

On the US—developments on house prices, rent, permits and mortgage:

- FOMO Helped Drive Up Housing Prices in the Pandemic. What Can We Expect Next? – New York Times

- Home Prices Suffer First Monthly Decline in Years. S&P CoreLogic Case-Shiller National Home Price Index fell 0.3% in July from June, the first month-over-month decline since January 2019 – Wall Street Journal

- Housing Paralysis Engulfs US Buyers With Prices Starting to Fall. Soaring mortgage rates have led to the worst affordability in almost four decades, while sellers are also trapped in place. – Bloomberg

- Unless Rents Rise, Housing Is Set Up for an Epic Crash. All of the reasons to suggest residential real estate is not facing a disaster have melted away. – Bloomberg

- Your City’s Housing Boom Could Go Bust. A national decline in home prices is unlikely, but markets that have experienced outsized increases over the past few years may be hit harder than most by rising mortgage rates – Wall Street Journal

- A Fundamental Reason House Prices Will Fall This Fall. The prices people expect tomorrow affect demand and supply today. – Real Estate Decoded

- The Housing Market Is Slowing. Just Look at Lumber Prices. – Barron’s

- Housing Starts Expected to Find Pre-Pandemic Levels Next Year, Analyst Says – Wall Street Journal

- Pace of Rent Increases Continues to Slow. Higher Rents will continue to impact measures of inflation in 2022 – Calculated Risk

- AEI Housing Market Indicators, September 2022 – American Enterprise Institute

- Inflation Adjusted House Prices Declined Further in July. House Price-to-Rent Ratio also Declined in July – Calculated Risk

On the US—other developments:

- Peaks in Housing Construction as a Recession Signal – St. Louis Fed

- Remote Work and Housing Demand – San Francisco Fed

- Unpacking Shelter Inflation – Philadelphia Fed

- Remote Work Drove Over 60% of House-Price Surge, Fed Study Finds – Bloomberg

- Why Wall Street is snapping up family homes. The opportunity is unprecedented, but comes with risks – The Economist

- Why Measures of Existing Home Inventory appear Different – Calculated Risk

- Whatever Happened to the Starter Home? The economics of the housing market, and the local rules that shape it, have squeezed out entry-level homes. – New York Times

- John Paulson on Frothy US Housing Market: This Time Is Different. Unlike subprime era, financial system is not at risk, he says. Real interest rates blamed for lackluster gold price – Bloomberg

- The U.S. Is Running Short of Land for Housing. Land-use restrictions and lack of infrastructure have made it harder for developers to find sites to build homes; ‘almost across the board, you’re fighting for land’ – Wall Street Journal

- Fed’s Harker says housing shortage a key inflation driver – Reuters

On China:

- A Ponzi scheme by any other name: the bursting of China’s property bubble. Only state intervention can save the day, but the pain is likely to fall on ordinary citizens, say observers – The Guardian

- World Bank Cuts China Growth Forecast as Covid-19, Real-Estate Crunch Take Toll. Emerging economies in Asia are seen outpacing China for the first time since 1990 – Wall Street Journal

On other countries:

- [Canada] Renters occupy rising share of newer homes in Canada, census shows – Reuters

- [Hong Kong] Hong Kong finance chief says no sharp risk to property prices – Reuters

- [Hong Kong] Hong Kong’s reduced bar for mortgages may not be enough to spur home sales – S&P Global

- [Hong Kong] Hong Kong home prices drop 2.3% in August to lowest in 3-1/2 years – Reuters

- [Indonesia] Indonesia’s house prices falling, despite improving demand – Global Property Guide

- [Nigeria] Nigeria to Allow Savers to Dip Into Pension Funds for Mortgages – Bloomberg

- [Portugal] Portugal House Prices Rise Most Since 2010 as Lisbon Struggles With Shortage of Homes. Lisbon is trying to increase the supply of homes in the city. Country has attracted foreign investors seeking golden visas – Bloomberg

- [United Kingdom] UK Unleashes Slew of Property Tax Cuts to Stoke Market. Threshold for property taxes will be doubled to £250,000. Tax threshold for first-time buyers increased to £425,000 – Bloomberg

- [United Kingdom] ‘It’s bittersweet’: what home-buyers think of chancellor’s stamp duty cut. Property-hunters on how permanent reduction for purchases in England and Northern Ireland will affect them – The Guardian

- [United Kingdom] Room to rent? UK housesharing on the rise due to energy bills and living costs. Taking in lodgers and sharing meals with family and friends are just some of the ways people can bear down on heating expenses – The Guardian

- [United Kingdom] House sellers ‘putting up prices despite rate rises and cost of living crisis’. Average price of homes coming to market in September increased by 0.7% on previous month to £367,760, says Rightmove – The Guardian

- [United Kingdom] UK House Asking Prices Rebound With Strongest Growth Since May. Rightmove says buyer demand is 20% higher than before pandemic. Lack of supply is likely to support market through recession – Bloomberg

- [United Kingdom] UK lenders pause new mortgages amid market turmoil. Virgin Money and Skipton among those to suspend loans as wholesale rates whipsaw – FT

- [United Kingdom] Where this UK mortgage meltdown will really bite. For both banks and consumers, the shock will jar some more than others – FT

- [United Kingdom] Jump in mortgage rates threatens UK property price crash. Market turmoil leaves more than 2mn homeowners facing sharp rise in borrowing costs over next two years – FT

- [United Kingdom] UK housing market may face perfect storm as mortgage rates rise, house prices drop – Reuters

- [United Kingdom] Almost 1,000 mortgage deals pulled as panic grips UK housing market. Borrowers unable to secure loans and provisional offers withdrawn as some pay huge penalties to lock in longer fixed rates – The Guardian

- [United Kingdom] UK house prices may fall 20% amid mortgage ‘carnage’, warn experts. Lack of supply will prevent crash, say some, while others predict ‘simple maths’ mean property price bubble poised to burst – The Guardian

On cross-country:

- How long can the super-prime property boom continue? The super-rich seem to have been largely unaffected by rising mortgage rates, spiralling inflation and the threat of recession — so far – FT

On the US—developments on house prices, rent, permits and mortgage:

- FOMO Helped Drive Up Housing Prices in the Pandemic. What Can We Expect Next? – New York Times

- Home Prices Suffer First Monthly Decline in Years.

Posted by at 5:00 AM

Labels: Global Housing Watch

Friday, September 23, 2022

Housing View – September 23, 2022

On cross-country:

- ECB Says Pandemic Behavioral Shifts May Cushion Housing Market – Bloomberg

- The impact of rising mortgage rates on the euro area housing market – European Central Bank

- Who escapes the great mortgage reset? Higher interest rates make refinancing an increasingly grim prospect for homeowners and businesses – FT

- Affordable housing attracts institutional investment. The need for affordable homes has never been greater. At the same time, the institutional interest in Australian housing has never been stronger. – Financial Review

- The World Got $41 Trillion Wealthier Last Year. U.S. Households Were Big Gainers. – Wall Street Journal

- Affordable Homes for the Poor Can Boost Collective Well-Being – Insead

On the US—developments on house prices, rent, permits and mortgage:

- Powell Warns of Correction in Once ‘Red-Hot’ Housing Market. Fed chief says US property price-gains were unsustainable. ‘Good thing’ for prices to decelerate, Powell says Wednesday – Bloomberg

- Home prices see biggest drop in 9 years, thanks to higher mortgage rates – NPR

- U.S. home sales drop for 7th straight month, house price growth cooling – Reuters

- Climbing Housing Costs Could Prop Up Inflation for a While. Economists say rents will eventually moderate. Question is when? – Wall Street Journal

- Biden Adviser Says Fed Hikes Are Helping to Cool Housing Prices – Bloomberg

- Decline in Single-Family Permits in July 2022 – NAHB

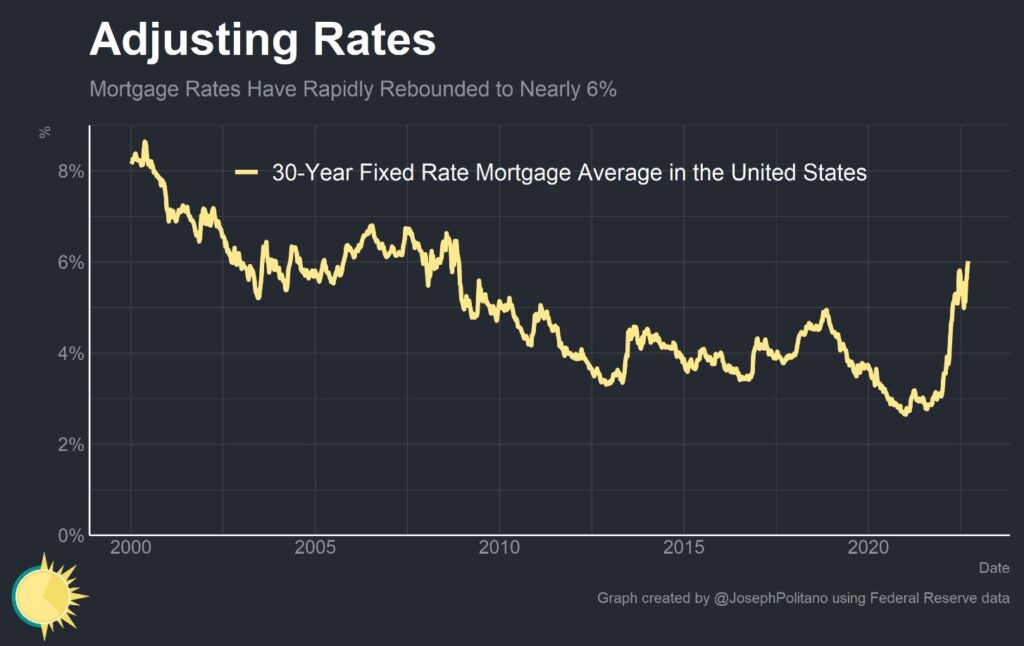

- As Mortgage Rates Top 6%, More Borrowers Choose Adjustable-Rate Loans. Although riskier, this type of mortgages offers buyers chance to make lower payments now, refinance later – Wall Street Journal

- These Are the US Areas Most at Risk of Housing Downturn, According to Attom Report. Counties seen most vulnerable to price declines in ranking. Rising rates are hurting home sales, boosting unaffordability – Bloomberg

- US Housing Starts Rise Unexpectedly Though Building Permits Drop. Pace of new construction rose 12.2% in August to 1.58 million. Permit applications decline to slowest pace since mid-2020 – Bloomberg

- August Housing Starts: Record Number of Housing Units Under Construction. Housing Starts Increased to 1.575 million Annual Rate in August – Calculated Risk

On the US—other developments:

- America’s Fractured Housing Market. The Pandemic Broke America’s Housing Market in More Ways Than One – Apricitas Economics

- There’s an Unusual Thing Happening in the Housing Market – Bloomberg

- Homeownership for All Is a Dying Dream. The U.S. economy evolved to spread affordable homes to the masses. A Columbia historian describes how it happened, and why the trend has broken down. – New York Times

- Rate-Hike Fears Are Hitting People Where They Live. The Fed could wreak damage on housing markets that were already strained by affordability. Homebuilder confidence is falling sharply. – Bloomberg

- 3rd Look at Local Housing Markets in August. Sales and New Listings Down Sharply Year-over-year – Calculated Risk

- The Long March of the YIMBYs. Slowly, the tide is starting to turn. – Noah Smith

- A New Set of Housing Winners and Losers Is Emerging. Economic inequality this decade will largely be defined by those who bought homes before 2022 and those who didn’t. – Bloomberg

- NAR: Existing-Home Sales Decreased Slightly to 4.80 million SAAR in August – Calculated Risk

- Economic Indicators Continue to Point to Likely Recession in 2023. Housing Expected to Cool Even Further as Mortgage Rates Move Higher – Fannie Mae

- Covid Era Impacts on Working from Home and Housing Market Impacts – Calculated Risk

On China:

- China’s property crisis hasn’t gone away: it is getting worse. Officials may have little choice but to bail out the industry – The Economist

- China’s local government financing vehicles go on land-buying spree. Property purchases seen as bailout for cities and provinces after exodus of private developers – FT

- China’s Housing Market Is Still on Life Support. Without firmer, broader commitment from Beijing, China’s housing woes will continue to spread – Wall Street Journal

- Even State-Backed China Developers at Risk of Surging Default, Citi Says. SOE developers are biggest drivers of this year’s increase. Overall systemic risk is still ‘manageable’ for Chinese banks – Bloomberg

- Housing Wealth and Online Consumer Behavior: Evidence from Xiong’an New Area in China – NBER

- Chinese buyers snap up luxury homes as ‘hard currency’ in soft property market – Reuters

- China Mortgage Boycotts Grow as Home Buyers Regroup Online. GitHub list shows homebuyers boycotting 342 projects in China. Government has sought to ease crisis with more funds, loans – Bloomberg

On other countries:

- [Australia] Interest Rates and the Property Market – Reserve Bank of Australia

- [Australia] Australia Property CEOs Give Diverging Outlooks as Rates Rise. Lendlease’s Lombardo sees tailwinds growing for real estate. Dexus CEO sees one of toughest environments of his career – Bloomberg

- [Australia] Houses to be hit harder than flats by price falls, RBA says. Head of domestic markets says rate rises will depress commercial and residential property prices but wider risks appear contained – The Guardian

- [Australia] Australian sprawl: why developing our way to affordable housing could backfire – The Guardian

- [Canada] Housing Prices Grind Lower in Canada, Aiding Fight Against Inflation. Benchmark prices drop 1.6% in August and are 7.4% below peak. Declines won’t change central bank’s approach, BMO says – Bloomberg

- [Canada] Canada housing starts fall 3% in August as multi-units decline – Reuters

- [Canada] Cool housing market puts a freeze on flipping – The Globe and Mail

- [Ireland] ‘It’s absolutely buzzing’: Dublin house prices rebound. Ireland’s capital city has seen immigration rise and a return to ‘Celtic Tiger’ prices – FT

- [Mexico] Mexico’s sluggish housing market – Global Property Guide

- [Norway] Norway’s housing market losing steam – Global Property Guide

- [Sweden] Swedish Housing Prices Continue Lower as Cost Surge Looms. Apartment prices rose 0.6% in August, while house prices fell. Rising power costs may worsen the slump in home prices – Bloomberg

On cross-country:

- ECB Says Pandemic Behavioral Shifts May Cushion Housing Market – Bloomberg

- The impact of rising mortgage rates on the euro area housing market – European Central Bank

- Who escapes the great mortgage reset? Higher interest rates make refinancing an increasingly grim prospect for homeowners and businesses – FT

- Affordable housing attracts institutional investment. The need for affordable homes has never been greater.

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, September 21, 2022

America’s Fractured Housing Market

From Joseph Politano:

“In early 2020, COVID-19 represented arguably the biggest negative shock to the housing market since 2008. With unemployment rising to 14%, millions of people being forced to move back in with friends or family, and a large share of homeowners becoming at risk of foreclosure, the outlook for the housing market appeared grim.

Policymakers, though, are famously good at fighting the last war—remembering how bad the 2008 crisis was, they pulled out all the stops this time. The Federal Reserve started buying billions in Mortgage-Backed Securities, the federal government spun up a mortgage forbearance program for homeowners, cities and states implemented broad eviction moratoriums, and large amounts of money were disbursed in the form of unemployment benefits and stimulus checks to help workers make rent

By 2021, COVID-19 represented arguably the biggest positive shock to the housing market since 2008—making the initial panic about a possible housing market collapse seem almost ridiculous in retrospect. The feared surge in evictions and foreclosures never came to pass. Prices started skyrocketing as America’s preexisting acute housing shortage mixed with cash-flush buyers who suddenly desired much more space for more home-bound lifestyles. A working paper by John Mondragon and Johannes Wieland attributed half of the 30% increase in housing prices from the end of 2019 to the end of 2021 to the pandemic-driven shift to remote work.“

Continue reading here.

From Joseph Politano:

“In early 2020, COVID-19 represented arguably the biggest negative shock to the housing market since 2008. With unemployment rising to 14%, millions of people being forced to move back in with friends or family, and a large share of homeowners becoming at risk of foreclosure, the outlook for the housing market appeared grim.

Policymakers, though, are famously good at fighting the last war—remembering how bad the 2008 crisis was,

Posted by at 9:01 AM

Labels: Global Housing Watch

Monday, September 19, 2022

Housing Market in Norway

From the IMF’s latest report on Norway:

“Further improvements were made to the macroprudential policy framework, but some recommendations remain outstanding, especially with respect to housing (Annex IV). Following the introduction of the consumer credit regulation in 2019 and the establishment of credit registries, the volume of consumer credit declined, and there are now substantially fewer borrowers with very high consumer debt. Temporary relaxation of mortgage lending regulation that facilitated debt restructuring and home-equity withdrawals ended, and support measures to households were rolled back. Staff continues to recommend to permanently preserve tighter mortgage regulation limits for Oslo now that the recovery is sustained and given still high house price growth in the capital (Box 3). As emphasized during pervious consultations, other targeted measures, including easing restrictions on the supply of new housing, altering regulations to boost construction efficiency, and curbing demand through a gradual phasing out of mortgage interest deductibility should also be implemented. In September 2021, Norges Bank was granted decision-making responsibility for setting the countercyclical capital buffer (CCyB), which is set four times a year, and advisory responsibility for the systemic risk buffer, in line with the 2020 FSAP recommendation. Recommendation powers on other tools should also be granted (Annex IV).”

From the IMF’s latest report on Norway:

“Further improvements were made to the macroprudential policy framework, but some recommendations remain outstanding, especially with respect to housing (Annex IV). Following the introduction of the consumer credit regulation in 2019 and the establishment of credit registries, the volume of consumer credit declined, and there are now substantially fewer borrowers with very high consumer debt. Temporary relaxation of mortgage lending regulation that facilitated debt restructuring and home-equity withdrawals ended,

Posted by at 10:07 AM

Labels: Global Housing Watch

Subscribe to: Posts