Tuesday, January 18, 2022

Working from home and corporate real estate

From a VoxEU post by Antonin Bergeaud, Jean Benoit Eymeoud, Thomas Garcia, and Dorian Henricot:

“As employers and employees established ways of working remotely to limit physical interaction during outbreaks of Covid-19, teleworking became increasingly routine. This column examines how corporate real-estate market participants adjusted to the growth of teleworking in France, and finds that it has already made a noticeable difference in office markets. In départements more exposed to telework, the pandemic prompted higher vacancy rates, less construction, and lower prices. Forward-looking indicators suggest that market participants believe the shift to teleworking will endure.

One of the primary hysteresis of the Covid-19 pandemic on the organisation of work is probably the dramatic take-off of telework. Forced by circumstances, employers and employees had to implement new ways of working remotely to limit physical interactions during the acute stages of the outbreak. This experience prompted companies to invest more in computer equipment and to adapt their management practices. Teleworking has thus already become a standard practice for many workers and is likely to endure (Barrero et al. 2021).

The polarisation of economic activity has led to a significant increase in real estate prices in dynamic areas. Office real estate is no exception, and the cost of corporate real estate is increasingly weighing on firms’ bottom lines (Bergeaud and Ray 2020). Companies taking advantage of teleworking to reduce office space demand could induce a structural downturn in the corporate real estate market. In the US, Bloom and Ramani (2021) show that the pandemic and the rise of telework is already having a substantial impact on the spatial dynamics of city real estate, producing a ‘doughnut effect’. In a recent study (Bergeaud et al. 2021), we look at the first signs of such an adjustment in France.

Local heterogeneity of the propensity to telework

We first define an index that measures exposure to the deployment of telework at the county (département) level. The index is the product of two components. First, we use the indicator constructed by Dingel and Neiman (2020) at the occupation level and apply it to the local composition of labour in France. We interpret it as a maximum potential for teleworking. However, this upper bound is unlikely to be reached in practice (Bartik et al. 2020). Also, we introduce frictions (quality of the internet infrastructure, average commuting time, number of families with children) that prevent the full use of the telework potential. We extract a principal component from these frictions and combine it with the maximum potential to construct a single index that measures the actual propensity of teleworking by county.”

Continue reading here.

From a VoxEU post by Antonin Bergeaud, Jean Benoit Eymeoud, Thomas Garcia, and Dorian Henricot:

“As employers and employees established ways of working remotely to limit physical interaction during outbreaks of Covid-19, teleworking became increasingly routine. This column examines how corporate real-estate market participants adjusted to the growth of teleworking in France, and finds that it has already made a noticeable difference in office markets. In départements more exposed to telework,

Posted by at 7:07 AM

Labels: Global Housing Watch

Monday, January 17, 2022

Understanding the Declining Share of Labor in USA’s National Income

Source: VoxEU

“After a century of stability, the labour share of national income began to decline around 2000 in the US and many other countries. This column reviews the growing literature examining the potential reasons for the decline of the labour share, which include (1) capital-biased technical change, (2) globalisation and the rise of China, (3) increasing industry concentration and market power, (4) unionisation, and (5) population growth. The column also discusses pitfalls associated with common empirical strategies in the literature and suggests that more work is needed to understand fundamental, rather than proximate, causes of the decline.“

Also Read:

Is Something Different this Time about the Effect of Technology on Labor Markets (2019)

Source: VoxEU

“After a century of stability, the labour share of national income began to decline around 2000 in the US and many other countries. This column reviews the growing literature examining the potential reasons for the decline of the labour share, which include (1) capital-biased technical change, (2) globalisation and the rise of China, (3) increasing industry concentration and market power, (4) unionisation, and (5) population growth. The column also discusses pitfalls associated with common empirical strategies in the literature and suggests that more work is needed to understand fundamental,

Posted by at 10:46 AM

Labels: Inclusive Growth

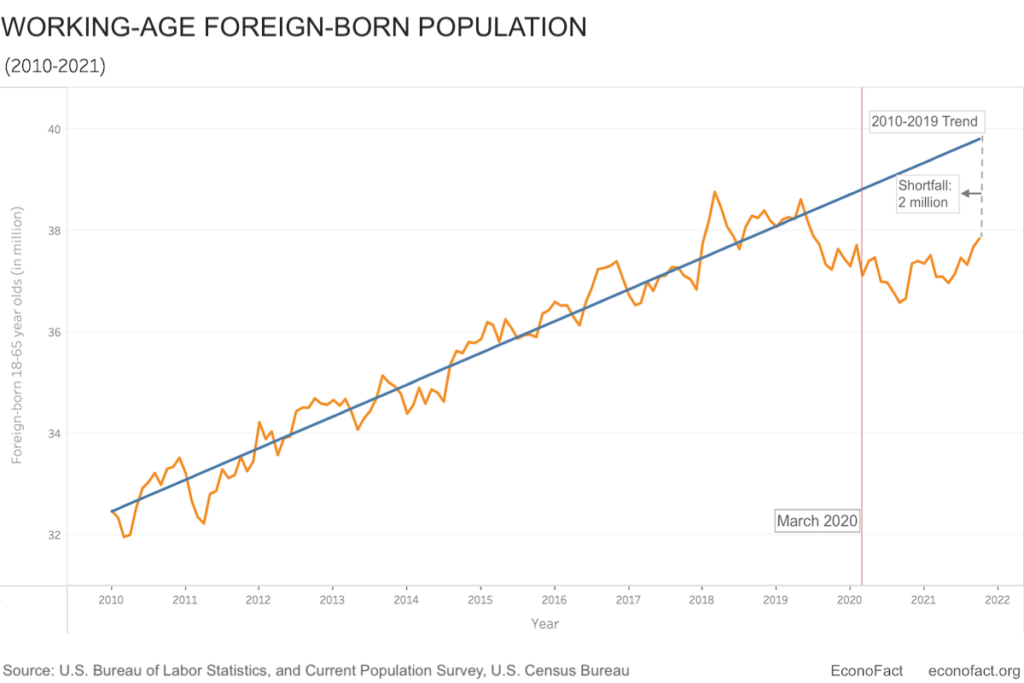

Labor Shortages and the Immigration Shortfall

The COVID-19 pandemic brought with it numerous travel and immigration-related restrictions throughout the globe. For the USA, this translated into a shortfall of nearly 2 million working-age immigrants compared to how many there would have been if the pre-2020 immigration trend had continued unchanged.

Metadata within this shows that out of these 2 million immigrants nearly one million would have been college graduates, implying a loss to the US labor market in terms of skilled workers, entrepreneurs, and a huge loss to American Universities which annually attract several foreign students. The drop in numbers of highly-skilled immigrants is significant due to its “long-run effects on productivity, innovation, and entrepreneurship”. The blog sheds light on these and several such issues.

Click here to read the full blog.

The COVID-19 pandemic brought with it numerous travel and immigration-related restrictions throughout the globe. For the USA, this translated into a shortfall of nearly 2 million working-age immigrants compared to how many there would have been if the pre-2020 immigration trend had continued unchanged.

Source: Labor Shortages and the Immigration Shortfall (2022). Econofact.org

Metadata within this shows that out of these 2 million immigrants nearly one million would have been college graduates,

Posted by at 10:33 AM

Labels: Inclusive Growth, Macro Demystified

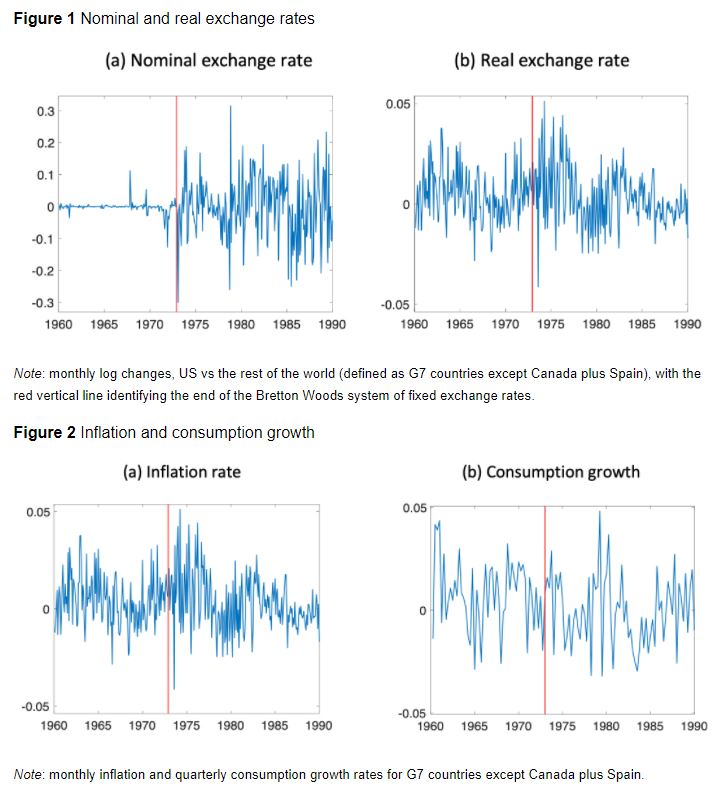

The Mussa puzzle and the optimal exchange rate policy

From a VoxEU post by Oleg Itskhoki and Dmitry Mukhin:

“The Mussa puzzle refers to the existence of a large and sudden jump in the volatility of the real exchange rate after the adoption of a floating exchange rate regime in 1973. It is a central piece of evidence in favour of monetary non-neutrality. In contrast to conventional wisdom, this column argues that the puzzle cannot be explained with sticky prices, and instead provides strong evidence in favour of monetary transmission via the financial market. This has important consequences for the design of optimal monetary and exchange rate policy.

What is the most convincing evidence that monetary shocks affect real outcomes? When Nakamura and Steinsson (2018) surveyed prominent macroeconomists, “the three most common answers were: the evidence presented in Friedman and Schwartz (1963) regarding the role of monetary policy in the severity of the Great Depression; the Volcker disinflation of the early 1980s and accompanying twin recession; and the sharp break in the volatility of the US real exchange rate accompanying the breakdown of the Bretton Woods System of fixed exchange rates in 1973”. This third fact, famously documented by Mussa (1986), is especially appealing as it relies on a simple and clear identification of the causal real effect from a shift in monetary policy: a large and discontinuous change in the nominal exchange rate process makes it hard to attribute the increased volatility of the real exchange rate to any other factors (see Figure 1)

What is missing from this narrative, however, is that there was no simultaneous change in the properties of other macro variables – neither nominal like inflation, nor real like consumption and output (Baxter and Stockman 1989, Flood and Rose 1995, and Figure 2). One could interpret this as an extreme form of neutrality, where a major shift in the monetary regime, which increases the volatility of the nominal exchange rate by an order of magnitude, does not affect the equilibrium properties of any macro variables, apart from the real exchange rate. In fact, this is a considerably more puzzling part of the larger set of ‘Mussa facts’ summarised in Figures 1 and 2. In a recent paper, we argue that this evidence points to a particular unconventional transmission mechanism of monetary policy and has important normative implications for both open and closed economies (Itskhoki and Mukhin 2021b).”

Continue reading here.

From a VoxEU post by Oleg Itskhoki and Dmitry Mukhin:

“The Mussa puzzle refers to the existence of a large and sudden jump in the volatility of the real exchange rate after the adoption of a floating exchange rate regime in 1973. It is a central piece of evidence in favour of monetary non-neutrality. In contrast to conventional wisdom, this column argues that the puzzle cannot be explained with sticky prices,

Posted by at 9:51 AM

Labels: Macro Demystified

The Agglomeration of Urban Amenities: Evidence from Milan Restaurants

From a NBER paper by Marco Leonardi & Enrico Moretti:

“In many cities, restaurants and retail establishments are spatially concentrated. Economists have long recognized the presence of demand externalities that arise from spatial agglomeration as a possible explanation, but empirically identifying this type of spillovers has proven difficult. We test for the presence of agglomeration spillovers in Milan’s restaurant sector using the abolition of a unique regulation that until recently restricted where new restaurants could locate. Before 2005, Milan mandated a minimum distance between restaurants that kept the spatial distribution of restaurants artificially uniform. As a consequence, restaurants were evenly distributed across neighborhoods. The regulation was abolished in 2005 by a nationwide reform that allowed new restaurants to locate anywhere in the city. Using administrative data on the universe of restaurants and retail establishments in Milan between 2000 and 2012, we study how the spatial distribution of restaurants changed after the reform. Consistent with the existence of significant agglomeration externalities, we find that after 2005, the geographical concentration of restaurants increased sharply. By 2012, 7 years after the liberalization of restaurant entry, the city’s restaurants had agglomerated in some neighborhoods and deserted others. By contrast, not much happened to the spatial concentration of retail establishments or even retail establishments that sell food, which were never covered by the minimum distance regulations and therefore were not directly affected by its reform. We also find that in neighborhoods where the number of restaurants grew the most after the reform, restaurants reacted to the increased competition by becoming more differentiated based on price, quality and type of cuisine.”

From a NBER paper by Marco Leonardi & Enrico Moretti:

“In many cities, restaurants and retail establishments are spatially concentrated. Economists have long recognized the presence of demand externalities that arise from spatial agglomeration as a possible explanation, but empirically identifying this type of spillovers has proven difficult. We test for the presence of agglomeration spillovers in Milan’s restaurant sector using the abolition of a unique regulation that until recently restricted where new restaurants could locate.

Posted by at 7:44 AM

Labels: Global Housing Watch

Subscribe to: Posts