Monday, January 17, 2022

The Mussa puzzle and the optimal exchange rate policy

From a VoxEU post by Oleg Itskhoki and Dmitry Mukhin:

“The Mussa puzzle refers to the existence of a large and sudden jump in the volatility of the real exchange rate after the adoption of a floating exchange rate regime in 1973. It is a central piece of evidence in favour of monetary non-neutrality. In contrast to conventional wisdom, this column argues that the puzzle cannot be explained with sticky prices, and instead provides strong evidence in favour of monetary transmission via the financial market. This has important consequences for the design of optimal monetary and exchange rate policy.

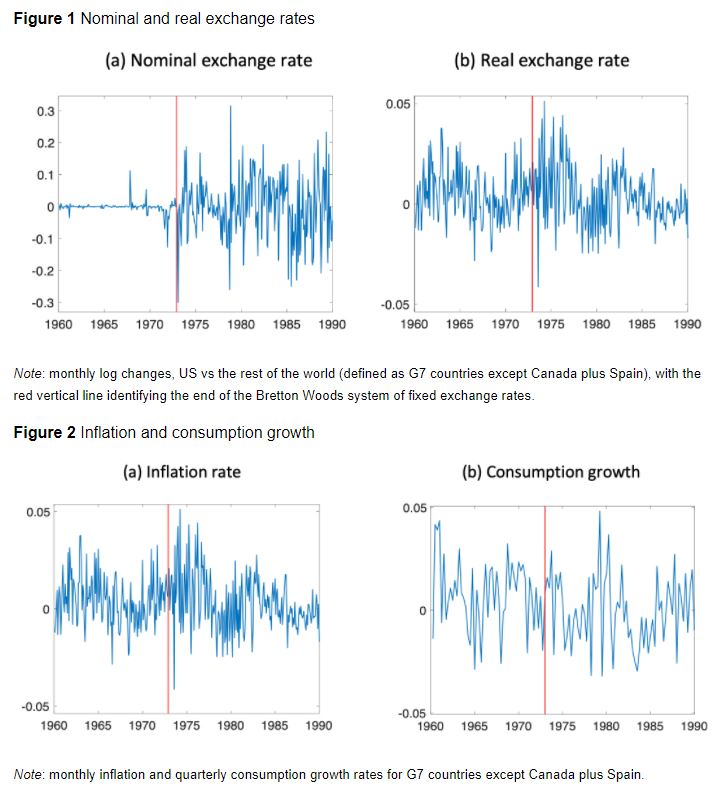

What is the most convincing evidence that monetary shocks affect real outcomes? When Nakamura and Steinsson (2018) surveyed prominent macroeconomists, “the three most common answers were: the evidence presented in Friedman and Schwartz (1963) regarding the role of monetary policy in the severity of the Great Depression; the Volcker disinflation of the early 1980s and accompanying twin recession; and the sharp break in the volatility of the US real exchange rate accompanying the breakdown of the Bretton Woods System of fixed exchange rates in 1973”. This third fact, famously documented by Mussa (1986), is especially appealing as it relies on a simple and clear identification of the causal real effect from a shift in monetary policy: a large and discontinuous change in the nominal exchange rate process makes it hard to attribute the increased volatility of the real exchange rate to any other factors (see Figure 1)

What is missing from this narrative, however, is that there was no simultaneous change in the properties of other macro variables – neither nominal like inflation, nor real like consumption and output (Baxter and Stockman 1989, Flood and Rose 1995, and Figure 2). One could interpret this as an extreme form of neutrality, where a major shift in the monetary regime, which increases the volatility of the nominal exchange rate by an order of magnitude, does not affect the equilibrium properties of any macro variables, apart from the real exchange rate. In fact, this is a considerably more puzzling part of the larger set of ‘Mussa facts’ summarised in Figures 1 and 2. In a recent paper, we argue that this evidence points to a particular unconventional transmission mechanism of monetary policy and has important normative implications for both open and closed economies (Itskhoki and Mukhin 2021b).”

Continue reading here.

Posted by at 9:51 AM

Labels: Macro Demystified

Subscribe to: Posts