Wednesday, July 20, 2022

Housing Market in Germany

From the IMF’s latest report on Germany:

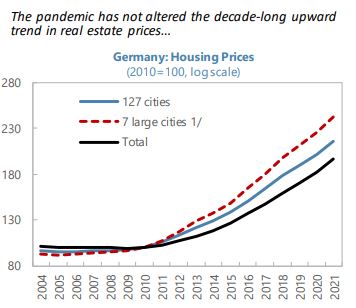

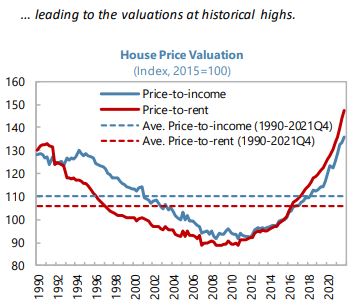

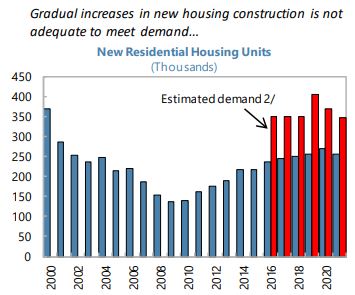

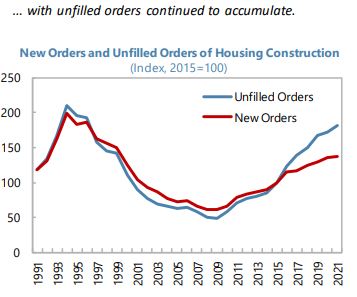

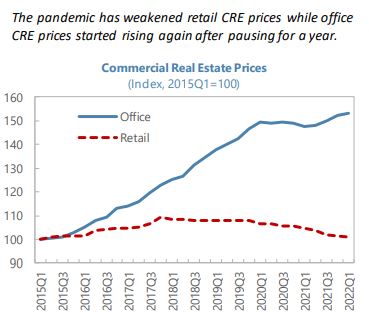

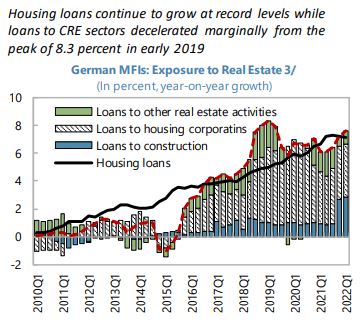

“The authorities have appropriately tightened macroprudential policy in the face of house price risks, but further actions are needed. Rapid rises in housing prices (12.4 percent between 2021Q4 and 2020Q4) have led to residential real estate valuations above fundamental levels for Germany overall, and even greater misalignment in larger cities. Nationwide, price-to-rent and price-to-income indicators suggested deviations from the long-run average of about 37 and 21 percent, respectively at end-2021, while estimates of an econometric model suggest overvaluations of 10–15 percent at 2021Q3. Meanwhile, a city-level panel model suggests greater overvaluation in the largest cities. Mortgage origination has also been strong and lending standards appear somewhat loose in certain segments. For example, according to different private sector data sources, between 7 and 20 percent of mortgage loans exceed the underlying property value (e.g., Text Figure 11). With these vulnerabilities in mind, the authorities appropriately raised the counter-cyclical capital buffer to 0.75 percent, from zero previously, and introduced a sectoral systemic risk buffer of two percent on loans secured by domestic residential real estate to apply from February 1, 2023. The authorities have also cautioned banks against taking excessive risks in mortgage lending. However, legal concerns and a lack of comprehensive data on lending standards remain obstacles to the activation of borrower-based measures, like the imposition of limits on loan-to-value ratios on new lending. As noted in the FSAP, precautionary use of borrower-based measures is warranted, and the authorities should remove obstacles to their activation by modifying the law on borrower-based measures, while in the interim strengthening guidance on lending standards (for example, encouraging banks to adhere to loan-to-value ratio limits through issuing a Guidance Note to banks). The authorities are also urged to accelerate the closure of data gaps and add income-based measures into the macroprudential toolkit.

Authorities’ Views

While generally sharing staff’s assessment of financial sector health and recommendations, the authorities assessed that risks in the housing market do not warrant the activation of borrower-based measures at this juncture. The authorities appreciated the FSAP’s stress tests of bank solvency and liquidity and found the results to be in line with their expectations. They are aware of U.S. dollar liquidity risks at some LSIs but judge that these are already sufficiently managed in the supervisory process. They emphasized the risk-sharing that takes place between savings and cooperative banks and their regional wholesale bank partners. The authorities highlighted the appropriateness of the macroprudential policy package announced by BaFin in January 2022. They noted that important data gaps on lending standards will be closed in 2023 and legislative proposals are being drafted to add income-based instruments to the toolkit. Furthermore, the Bundesbank has set up a project dedicated to monitoring the effects of the macroprudential policy package—inter alia its effects on lending standards. Existing private sector data on LTV and DSTI ratios currently provide mixed signals. On financial safety nets, the authorities considered that maintaining the existing multiple deposit guarantee schemes appropriately reflects the three-pillar structure of the German banking system.

From the IMF’s latest report on Germany:

“The authorities have appropriately tightened macroprudential policy in the face of house price risks, but further actions are needed. Rapid rises in housing prices (12.4 percent between 2021Q4 and 2020Q4) have led to residential real estate valuations above fundamental levels for Germany overall, and even greater misalignment in larger cities. Nationwide, price-to-rent and price-to-income indicators suggested deviations from the long-run average of about 37 and 21 percent,

Posted by at 1:16 PM

Labels: Global Housing Watch

The end of privilege: A re-examination of the net foreign asset position of the US

A VoxEU article by Andy Atkeson, Jonathan Heathcote, Fabrizio Perri:

“The US net foreign asset position – measuring the difference between its foreign assets and liabilities – was negative, yet small, until 2007. This column shows that since then, it has deteriorated sharply to negative 40% of GDP, mostly as a result of changes in the market value of US-owned assets abroad and foreign-owned assets in the US. These valuation effects are explained by rising US equity values disproportionately benefitting foreign owners of US firms. Whether this is beneficial for depends on whether the profit rises are due to higher productivity or lower competition.

A country’s net foreign asset position measures the value of all the assets residents own abroad minus the value of assets foreigners own in the country. It is an important statistic, because all else equal, a higher net foreign asset position means a country can expect higher future net income from abroad, and can thus plan on running larger future trade deficits. One common way to decompose changes in the net foreign asset position is to recognise that the position can improve because a country, on net, acquires additional foreign assets – i.e. it runs a current account surplus – or because the market value of existing assets owned abroad increases relative to the value of foreign-owned assets in the country.

The US has long had a negative net foreign asset position. But until 2007 it was relatively small, never exceeding 20% of US GDP. In fact, the position was surprisingly small given the US history of large and persistent current account deficits. In influential papers, Gourinchas and Rey (2007, 2014) emphasised the importance of valuation effects in shaping the dynamics of the US net foreign asset position. At the time they were writing, these revaluations seemed to move consistently in favour of the US, especially during the mid-2000s. The net effect was that the US appeared to enjoy the special privilege of being consistently able to borrow without running up much debt. Gourinchas and Rey and others argued that this privilege reflected an asymmetry in cross-country portfolios, with Americans owning lots of direct investment and portfolio equity assets abroad – whose value tended to rise over time – while US liabilities consisted disproportionately of low return US government bonds.

Our paper (Atkeson et al. 2022) updates the history of the US net foreign asset position, using data assembled by the US Bureau of Economic Analysis and the US Treasury in the Financial Accounts of the United States. We find that a lot has changed in the last 15 years. First and most notably, the US net foreign asset position has deteriorated very sharply, from negative 5% of US GDP in 2007, to negative 65% of US GDP by the third quarter of 2021. Such a large negative net position is unprecedented. What has driven this decline? What are the welfare implications for Americans?”

Continue reading here.

A VoxEU article by Andy Atkeson, Jonathan Heathcote, Fabrizio Perri:

“The US net foreign asset position – measuring the difference between its foreign assets and liabilities – was negative, yet small, until 2007. This column shows that since then, it has deteriorated sharply to negative 40% of GDP, mostly as a result of changes in the market value of US-owned assets abroad and foreign-owned assets in the US. These valuation effects are explained by rising US equity values disproportionately benefitting foreign owners of US firms.

Posted by at 7:36 AM

Labels: Macro Demystified

Sunday, July 17, 2022

Interview: Leah Boustan, economist

From Noah Smith:

“Immigration is obviously one of the most important and most contentious issues of our time. The sheer amount of confusion, misconception, and misinformation is just staggering. So when I want to know the hard facts on the immigration issue, I go to Princeton economist Leah Boustan.

Boustan’s research covers far more than immigration — she’s incredibly versatile, covering labor economics, urban economics, economic history, and more. But recently, her research on immigration has garnered a lot of (well-deserved) attention. In a series of recent papers, she and her various co-authors showed that 1920s immigration restrictions hurt native-born American workers, that immigrant groups give their kids less foreign-sounding names over time, that immigrants do better economically when they move out of ethnic enclaves, and that the children of poor immigrants tend to be extremely upwardly mobile.

In her new book with Ran Abramitzky, Streets of Gold: America’s Untold Story of Immigrant Success, Boustan draws from her own research and others’ to weave a nuanced yet compelling story of how immigrants fare in the United States — and how little this has changed between the early 20th century and the early 21st. It’s a great book, and I highly recommend it to everyone.

In this interview, I ask Leah about her book, and about the immigration issue in general. Enjoy!

N.S.: I’ve been following your work for years, and you’re my favorite economist of immigration. How did you first become interested in that topic?

L.B.: First, thank you! That is so kind to say and I have appreciated all of your engagement with our work through the years. I will always associate the “before times” (immediately pre-Covid) with being able to meet in person at the ASSA conference in Jan 2020.

So, how did I become interested in immigration? Well, my first book was on the black migration from the rural South to industrial cities in the North and West (the Great Black Migration). I got interested in this topic when reading William Julius Wilson’s The Truly Disadvantaged and encountering a paragraph with what seemed like an aside, but it really is a gem of an idea. Wilson said something like “ironically, European immigrants benefited from the closing of the US border in the 1920s, but black migrants faced a lot of competition because you can’t close the Mason-Dixon line.” (This is a paraphrase!). I thought to myself – wow – I always knew about white ethnic communities in US cities, but I never really thought of the black community as a *migrant* community. So what if we – as economists – really study African-American history as migrant history? My first book was called Competition in the Promised Land, which picks up on this idea.

It was pretty natural after that to turn my attention to studying European immigrants in the late 19th and early 20th centuries. Sociologists like Wilson and like Stanley Lieberson explicitly or implicitly compare white ethnic progress with African American progress. So, after working for some time on black migrants, I wanted to learn more about European immigrants as well.”

Continue reading here.

From Noah Smith:

“Immigration is obviously one of the most important and most contentious issues of our time. The sheer amount of confusion, misconception, and misinformation is just staggering. So when I want to know the hard facts on the immigration issue, I go to Princeton economist Leah Boustan.

Boustan’s research covers far more than immigration — she’s incredibly versatile, covering labor economics,

Posted by at 7:34 AM

Labels: Book Reviews, Profiles of Economists

Friday, July 15, 2022

Housing View – July 15, 2022

On cross-country:

- Are foreigners inflating property prices? – BFM

On the US:

- New Fed Paper Finds Surging Home Prices Driven by Demand — Not Supply – Bloomberg

- Volatility in Home Sales and Prices: Supply or Demand? – Federal Reserve Board

- What’s behind the rising rents and what can be done? – Washington Post

- Relief Eludes Many Renters as Fed Raises Interest Rates. As the central bank sharply increases borrowing costs, it could lock would-be home buyers into rentals and keep a hot market under pressure. – New York Times

- Remodeling Market Declines Year-over-Year – NAHB

- The Great Appreciation Of Home Prices Is Now Over – Forbes

- Housing Shortage Spreads Across US, Becoming Coast-to-Coast Crisis. New analysis shows deficits surging just before the pandemic, even in areas that had few supply challenges a decade ago. – Bloomberg

- What’s Up With the Crazy Housing Market? Rising mortgage rates. Faltering home sales. Skyrocketing rents. Here’s how to make sense of a baffling real estate market. – New York Times

- Housing inventories may note save prices after all – Washington Post

- The United States Must Deliver on Equitable Housing Outcomes for All. Federal investments kept millions of Americans in their homes during the pandemic; in the long term, commitment to bold federal housing policy can eliminate housing insecurity for millions while uplifting historically disadvantaged communities. – American Center for Progress

- Who’s To Blame for Gentrification? Most likely, no one in particular—but policy changes can alleviate the housing shortage and prevent displacement. – Planetizen

- Why this tightening cycle is so brutal for the US housing market – Quartz

- Housing-Affordability Index Drops to Lowest Level Since 2006. Mortgage rates and home prices are up sharply, pressuring buyers and driving sellers to cut prices – Wall Street Journal

- The Coming Housing Risks – American Action Forum

- The cities where house prices are most likely to fall – Axios

- The great house U.S. price boom continues – Global Property Guide

- Inflation Expectations Increase at Short Term, But Decline at Medium and Longer Terms; Home Price Growth Expectations Decline Sharply – New York Fed

- How to limit the risks to financial stability posed by the Federal Home Loan Bank System – Brookings

- Housing Could Provide More Fuel for Inflation. Other consumer prices might need to post big drops for the Fed to see overall inflation fall – Wall Street Journal

On China

- Is China Stumbling Into Its Own Mortgage Crisis? A rapidly spreading protest — borrowers refusing to make payments on unfinished homes — threatens to rattle the financial system. – Bloomberg

- China Convenes Banks on Mortgage Boycott Roiling Markets. Officials asked for information on impact of housing loan snub. More buyers refuse to pay loans on unfinished home projects – Bloomberg

- Chinese Homebuyers Across 22 Cities Refuse to Pay Mortgages. Home loan payment halts may cause $83 billion of bad debt. China Construction Bank, Postal Bank, ICBC may be more exposed – Bloomberg

- China developers face $13bn wall of dollar bond payments in second half. Foreign investors fear Beijing will favour onshore creditors as Shimao Group becomes latest to default – FT

On other countries:

- [Cambodia] Cambodia’s house prices plunging – Global Property Guide

- [Ireland] Taxes Can Ease House Price Volatility, Irish Central Bank Says – Bloomberg

- [Sweden] Swedish Home Price Expectations Drop to Lowest Level Since 2008. SEB survey points to worsening price outlook for houses. The Riksbank sees home prices falling 16% through end of 2023 – Bloomberg

- [Thailand] Thailand’s housing market continues to slow – Global Property Guide

- [United Kingdom] UK house prices rise at fastest rate in 18 years. Typical home goes for record £294,845 as property shortage drives up costs for buyers – FT

- [United Kingdom] Covid-19 and the curious case of the rental bust-up that never came. An arbitration scheme to handle pandemic rental arrears is currently virtually unused – FT

On cross-country:

- Are foreigners inflating property prices? – BFM

On the US:

- New Fed Paper Finds Surging Home Prices Driven by Demand — Not Supply – Bloomberg

- Volatility in Home Sales and Prices: Supply or Demand? – Federal Reserve Board

- What’s behind the rising rents and what can be done? – Washington Post

- Relief Eludes Many Renters as Fed Raises Interest Rates.

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, July 12, 2022

Housing Market in the US

From the IMF’s latest report on the US;

“The housing market has been on a steep upward trajectory. Nationwide, average prices are 38 percent above where they were at end-2019 and prices are relatively high as a share of both rents and household income. Leverage, though, has been contained by relatively low loan-to-value ratios and conservative underwriting standards (a legacy of the post-financial crisis reforms). In addition, refinancing activity over the past few years has reduced average mortgage payments to all-time lows as a share of disposable income. As such, financial stability risks emanating from the housing market appear to be contained. However, there are important social concerns linked to the worsening in housing affordability, particularly for lower income households.”

From the IMF’s latest report on the US;

“The housing market has been on a steep upward trajectory. Nationwide, average prices are 38 percent above where they were at end-2019 and prices are relatively high as a share of both rents and household income. Leverage, though, has been contained by relatively low loan-to-value ratios and conservative underwriting standards (a legacy of the post-financial crisis reforms). In addition, refinancing activity over the past few years has reduced average mortgage payments to all-time lows as a share of disposable income.

Posted by at 5:50 PM

Labels: Global Housing Watch

Subscribe to: Posts