Wednesday, July 20, 2022

Housing Market in Germany

From the IMF’s latest report on Germany:

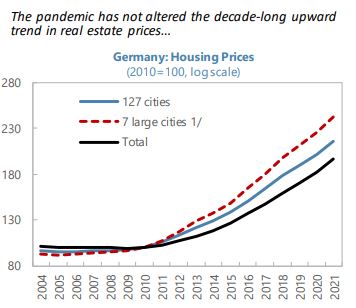

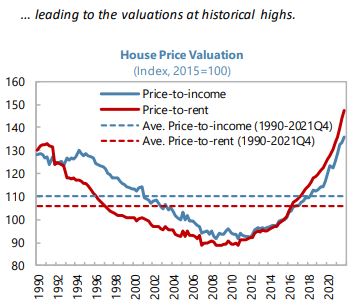

“The authorities have appropriately tightened macroprudential policy in the face of house price risks, but further actions are needed. Rapid rises in housing prices (12.4 percent between 2021Q4 and 2020Q4) have led to residential real estate valuations above fundamental levels for Germany overall, and even greater misalignment in larger cities. Nationwide, price-to-rent and price-to-income indicators suggested deviations from the long-run average of about 37 and 21 percent, respectively at end-2021, while estimates of an econometric model suggest overvaluations of 10–15 percent at 2021Q3. Meanwhile, a city-level panel model suggests greater overvaluation in the largest cities. Mortgage origination has also been strong and lending standards appear somewhat loose in certain segments. For example, according to different private sector data sources, between 7 and 20 percent of mortgage loans exceed the underlying property value (e.g., Text Figure 11). With these vulnerabilities in mind, the authorities appropriately raised the counter-cyclical capital buffer to 0.75 percent, from zero previously, and introduced a sectoral systemic risk buffer of two percent on loans secured by domestic residential real estate to apply from February 1, 2023. The authorities have also cautioned banks against taking excessive risks in mortgage lending. However, legal concerns and a lack of comprehensive data on lending standards remain obstacles to the activation of borrower-based measures, like the imposition of limits on loan-to-value ratios on new lending. As noted in the FSAP, precautionary use of borrower-based measures is warranted, and the authorities should remove obstacles to their activation by modifying the law on borrower-based measures, while in the interim strengthening guidance on lending standards (for example, encouraging banks to adhere to loan-to-value ratio limits through issuing a Guidance Note to banks). The authorities are also urged to accelerate the closure of data gaps and add income-based measures into the macroprudential toolkit.

Authorities’ Views

While generally sharing staff’s assessment of financial sector health and recommendations, the authorities assessed that risks in the housing market do not warrant the activation of borrower-based measures at this juncture. The authorities appreciated the FSAP’s stress tests of bank solvency and liquidity and found the results to be in line with their expectations. They are aware of U.S. dollar liquidity risks at some LSIs but judge that these are already sufficiently managed in the supervisory process. They emphasized the risk-sharing that takes place between savings and cooperative banks and their regional wholesale bank partners. The authorities highlighted the appropriateness of the macroprudential policy package announced by BaFin in January 2022. They noted that important data gaps on lending standards will be closed in 2023 and legislative proposals are being drafted to add income-based instruments to the toolkit. Furthermore, the Bundesbank has set up a project dedicated to monitoring the effects of the macroprudential policy package—inter alia its effects on lending standards. Existing private sector data on LTV and DSTI ratios currently provide mixed signals. On financial safety nets, the authorities considered that maintaining the existing multiple deposit guarantee schemes appropriately reflects the three-pillar structure of the German banking system.

Posted by at 1:16 PM

Labels: Global Housing Watch

Subscribe to: Posts