Tuesday, July 12, 2022

Pandemic Policy: Support Jobs or Workers?

From Conversable Economist:

“The pandemic recession from March to April 2020 was a different creature from the previous post World-War II recessions: different in cause, length, depth, and the kinds of social and economic changes that happened. The appropriate economic policy response was also different. Instead of the standard anti-recession policy of stimulating the entire economy, it is more useful to think of pandemic recession policy as a form of social insurance. One key question is whether this social insurance should operated primarily by supporting the unemployed or by supporting jobs.

Lest this distinction sound like a word game, consider this real world difference. In the pandemic, most European countries responded with programs of “short-time work.” The idea the employer doesn’t need to fire or lay-off workers. Instead, it cuts their hours substantially, and the government makes up the difference. It’s a kind of partial unemployment, except that when the worst of short, sharp pandemic hit to the economy passed by, the workers were still employed at their previous jobs and employers could ramp up their hours again. In contrast, the US approach emphasized larger and longer unemployment payment aimed at those who were without jobs. US employers (with the exception of some small state-level programs) did not have option of switching to short-time work.

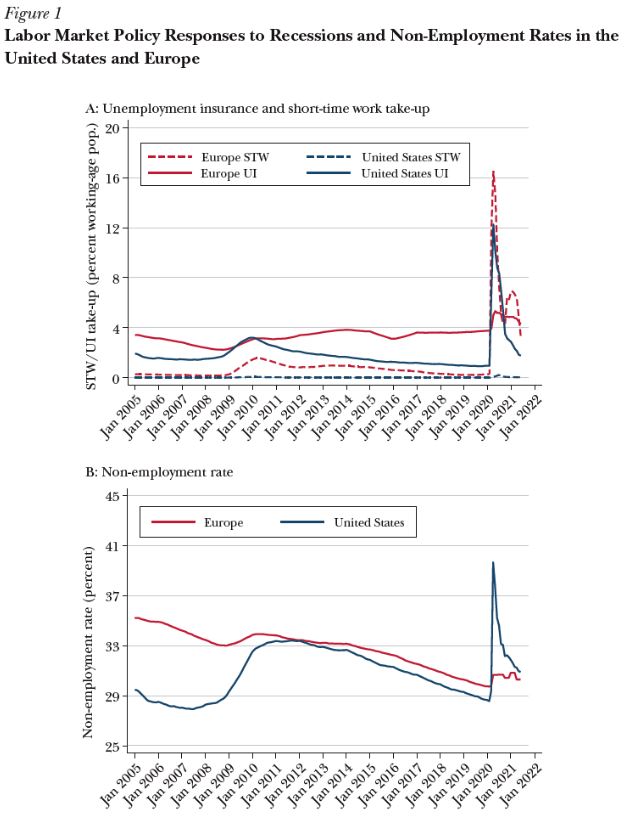

Giulia Giupponi, Camille Landais, and Alice Lapeyre discuss the tradeoffs between tehse two approaches in “Should We Insure Workers or Jobs during Recessions?” (Spring 2022, Journal of Economic Perspectives, 36:2, 29-54). Here’s one of their figures. The solid lines show the share of population receiving unemployment insurance, with the blue line showing the US and the red line showing a weighted average for Germany, France, Italy, and the United Kingdom. Notice that the share of workers getting unemployment insurance in the pandemic spikes up in the US (solid blue line) but barely budges in the European countries (solid red line). Conversely, the share of workers on short-time work spikes up in the European countries (dashed red line) but barely budgets in the US (dashed blue line).”

From Conversable Economist:

“The pandemic recession from March to April 2020 was a different creature from the previous post World-War II recessions: different in cause, length, depth, and the kinds of social and economic changes that happened. The appropriate economic policy response was also different. Instead of the standard anti-recession policy of stimulating the entire economy, it is more useful to think of pandemic recession policy as a form of social insurance.

Posted by at 7:39 AM

Labels: Inclusive Growth, Macro Demystified

Friday, July 8, 2022

Housing Market in Ireland

From the IMF’s latest report on Ireland:

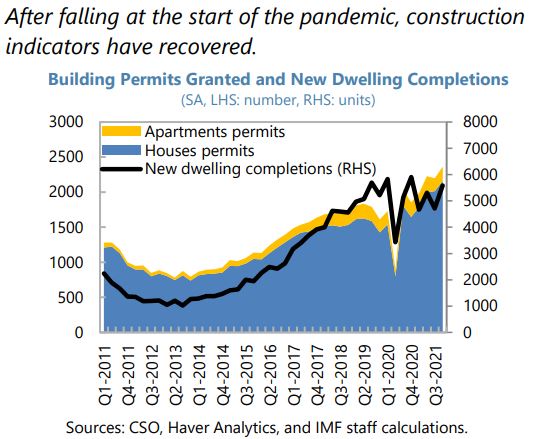

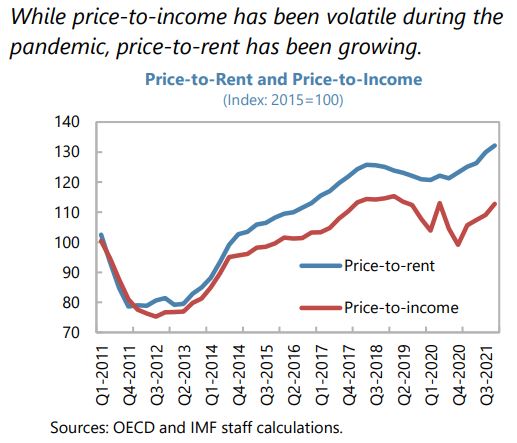

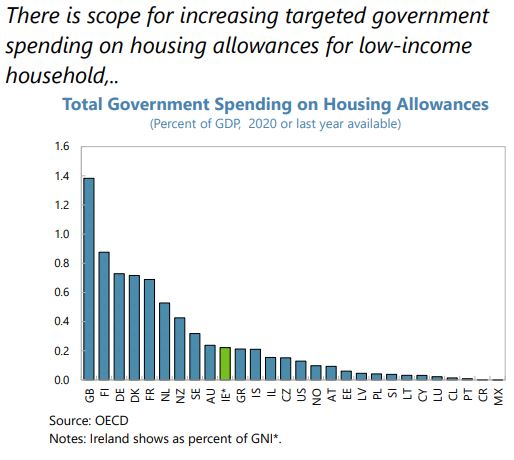

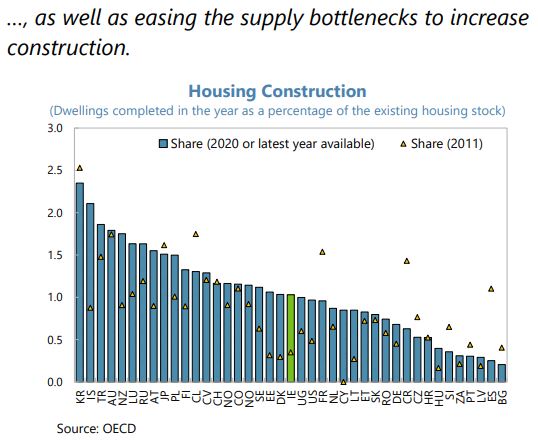

“The pandemic has exacerbated housing market’s imbalances, contributing to accelerating prices despite the recent acceleration in housing construction. Double-digit price growth has further pressured affordability as price-to-income and price-to-rent ratios increased sharply in recent quarters. House completions recovered in 2021 but were still below 2019 levels.

Housing commencements have accelerated to the highest number since the GFC, but the construction sector is facing combined headwinds of input cost inflation and labor shortages.

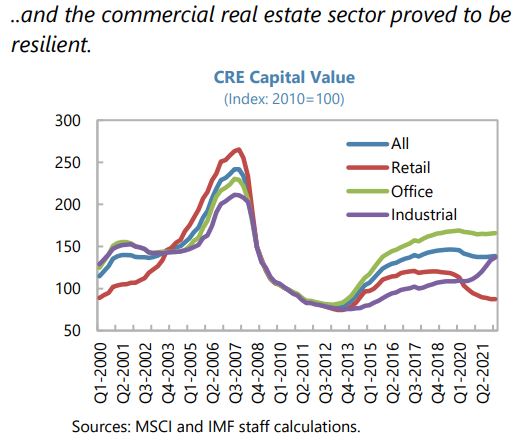

CRE activities performed better than expected during the pandemic. Investment in the sector was exceptionally strong in 2021 and this momentum is expected to continue in 2022. The polarization between different sectors that characterized the Irish property investment market stems from the higher return to investment in CRE than residential, partly due to the strong growth of MNEs, Brexit-related relocations to Ireland, and businesses’ general resilience despite the pandemic.

Supply-side policies should be further strengthened. The government has introduced a comprehensive fiscal and regulatory package (Housing for All18), costing close to 1 percent of GDP annually, to address the affordable housing shortage. The package includes measures to improve zoning, planning, land availability, and social housing. Timely implementation of these measures is needed and should be accompanied by additional policies aimed at raising productivity in the construction sector. The “First Home” affordable purchase shared-equity scheme (starting in 2022:Q3) aims to support first home buyers. However, it does not address the supply bottlenecks. While the scheme is partly targeted and limited in size, if expanded it can put further upward pressure on prices.

Improving construction productivity is needed to bolster housing supply. The construction sector is fragmented, lagging on digitalization, and faces high input costs and labor shortages. Complex and lengthy processes for obtaining occupational licenses, with excessively long apprenticeship requirements, raise barriers to entry and contribute to substantial bottlenecks and high costs of construction. In recent years, the government has taken some steps toward digitalization of the construction sector, upskilling and reskilling workers, including by increasing the number of apprenticeship centers. There is also a need to streamline the lengthy, cumbersome, and uncertain zoning and permit processes.

The government is implementing a set of comprehensive measures under “Housing for All – A New Housing Plan for Ireland” aimed at alleviating the housing shortage. Establishment of the Construction Sector Innovation and Digital Adoption Subgroup by the government and the industry is welcome to deliver on the seven priority actions detailed in the Building Innovation Report. The Construction Sector Group ensures regular and open dialogue between government and industry on how best to achieve and maintain a sustainable and innovative construction sector in order to successfully deliver on the commitments in Project Ireland 2040.”

From the IMF’s latest report on Ireland:

“The pandemic has exacerbated housing market’s imbalances, contributing to accelerating prices despite the recent acceleration in housing construction. Double-digit price growth has further pressured affordability as price-to-income and price-to-rent ratios increased sharply in recent quarters. House completions recovered in 2021 but were still below 2019 levels.

Housing commencements have accelerated to the highest number since the GFC, but the construction sector is facing combined headwinds of input cost inflation and labor shortages.

Posted by at 7:44 AM

Labels: Global Housing Watch

Housing Market in Vietnam

From the IMF’s latest report on Vietnam:

“Property and corporate bond markets risks are rising. Easy financial conditions contributed to record-high corporate bond issuances and equity and property market valuations. Price pressure points are largely seen in land sales, high-end housing in major cities, and mega-developments in coastal areas. Besides sizable direct exposure to the real estate sector in their loan portfolios, banks face indirect exposure through holding of corporate bonds issued by real estate companies. These companies have fairly robust debt servicing capacity but are more leveraged than the rest of the economy, and some were hit hard by the pandemic-induced drop in tourism. Recent policies to moderate systemic risks include measures to limit excessive leverage (e.g., higher risk weights for real estate) and recommendations urging prudent loan origination, particularly for property purchases.”

From the IMF’s latest report on Vietnam:

“Property and corporate bond markets risks are rising. Easy financial conditions contributed to record-high corporate bond issuances and equity and property market valuations. Price pressure points are largely seen in land sales, high-end housing in major cities, and mega-developments in coastal areas. Besides sizable direct exposure to the real estate sector in their loan portfolios, banks face indirect exposure through holding of corporate bonds issued by real estate companies.

Posted by at 7:24 AM

Labels: Global Housing Watch

Housing View – July 8, 2022

On cross-country:

- Prime residential rents in global cities rising at fastest rate since 2010 – Knight Frank

- The Impact of Home Sharing on Housing Affordability. Evidence from Airbnb in Urban Cities in Europe – Jonkoping University

On the US:

- Written testimony for hearing by Jenny Schuetz: Where Have All the Houses Gone: Private Equity, Single Family Rentals, and America’s Neighborhoods – Brookings

- Home Sellers Are Slashing Prices in Sudden Halt to Pandemic Boom. The rapid rise in mortgage rates is cooling demand, jolting markets from coast to coast – Bloomberg

- Biden Administration Weighs Move to Trim Mortgage Costs as Home Prices Rise. Mortgage industry officials say insurance cut for FHA-backed loans would help entry-level buyers; Republicans say it could increase prices – Wall Street Journal

- Redfin’s chief economist says the housing market correction has begun—and things are going to get worse before they get better – Fortune

- Inflation is making homelessness worse – Washington Post

- Volatility in Home Sales and Prices: Supply or Demand? – Federal Reserve Board

- Pandemic-Induced Remote Work and Rising House Prices – NBER

- Construction Job Openings Leveling Off – NAHB

- Lessons Learned from Mortgage Borrower Policies and Outcomes during the COVID-19 Pandemic – Boston Fed

- Mortgage Rates Fall to 5.30%, Reflecting Recession Fears. Rates fell for a second straight week, though they are still up significantly this year – Wall Street Journal

On China

- My garlic for a home: China struggles to revive property sector. The real estate market is struggling to recover as zero-Covid policies and developer debt sap buyer demand – FT

- China Property Debt Crisis Is Just Beginning, Charlene Chu Says. Charlene Chu sees further problems for China real estate. Ex-Fitch analyst says debt weighing on China economic growth – Bloomberg

On other countries:

- [Austria] How Vienna took the stigma out of social housing. In some European cities living in social housing is a misfortune. In Austria’s capital it’s an indicator of high-quality urban life. – Politico

- [Australia] Australian house prices fall for second month as interest rates rise. CoreLogic’s home value index drops for the second month in a row, after declining 0.6% in June – The Guardian

- [United Kingdom] The signs are Britain is not heading for a property crash. It would be naive to rule out the possibility, but the evidence points to house prices dampening rather than tumbling – The Guardian

On cross-country:

- Prime residential rents in global cities rising at fastest rate since 2010 – Knight Frank

- The Impact of Home Sharing on Housing Affordability. Evidence from Airbnb in Urban Cities in Europe – Jonkoping University

On the US:

- Written testimony for hearing by Jenny Schuetz: Where Have All the Houses Gone: Private Equity, Single Family Rentals, and America’s Neighborhoods – Brookings

- Home Sellers Are Slashing Prices in Sudden Halt to Pandemic Boom.

Posted by at 5:00 AM

Labels: Global Housing Watch

Sunday, July 3, 2022

How the World Became Rich: The Historical Origins of Economic Growth

From Economic History Association:

“Mark Koyama and Jared Rubin. How the World Became Rich: The Historical Origins of Economic Growth. Cambridge, UK: Polity Press. x + 259 pp. $24.95 (paperback), ISBN 978-1509540235.

Reviewed for EH.Net by Joel Mokyr, Departments of Economics and History, Northwestern University.

Any scholar teaching economic history and wishing for an up-to-date survey of a large and important literature will find it useful to read this book to bone up on the recent research listed in the long and encompassing list of references. Furthermore, they should seriously consider having their students read it for their class. The book is a wide-ranging yet remarkably complete and accessible survey of the Great Enrichment, the emergence of modern and prosperous economies that provide us with a material standard of living that our ancestors could not have dreamed of. How and why modern economic growth occurred when and where it did, and how economists have tried to understand this phenomenon, is the theme of this book. It is written by two of the finest young senior scholars in our field, both with important contributions to the subject matter of this book.

Many of the issues this book raises are highly contentious in our profession, and for good reason: these are hard questions on which learned scholars can disagree and interpret the evidence in different ways. How much did institutions really matter? What was the role of culture in economic growth? Was geography destiny? What was the role of craft guilds in the economic development of early modern Europe? How to think about the role of imperialism and slavery in the Industrial Revolution and the subsequent growth of industrial powers? Were high wages good or bad for technological progress? Was war a positive factor in economic growth? Was the European Marriage Pattern a positive factor in the economic development of the Continent?

The ecumenical and balanced approach the authors take to these questions is much like the Rabbi in a famous Jewish story. According to the legend, a rabbi is holding court in front of a large audience of his pupils. A husband and wife appear before the rabbi, to discuss their troubled domestic life. First the husband gets to lay out his case, and he lists all the sins and vices of his wife. The Rabbi listens carefully and pronounces his verdict: the husband is in the right. Then his pupils appeal to him: you should hear the wife’s case as well. The Rabbi consents and listens to the woman lays out her powerful case against her lazy and violent husband. He then announces his second verdict: the wife is in the right. His best pupil protests: but Rabbi, how can they both be in the right? The Rabbi listens and pronounces: the pupil is right too.

Rubin and Koyama present balanced and fair surveys of made in the literature, but they are reluctant to take strong positions. Such an ecumenical approach sets them apart from Clark’s Farewell to Alms and McCloskey’s Bourgeois Dignity, where the authors take up similar issues but in a much stronger opinionated mode. That thoughtful and measured approach of the survey, its elegant and crystal-clear style, and the authors’ impressive knowledge of a large and complex literature make this book nothing short of ideal for teaching advanced courses on global economic history to economics students.

It is especially refreshing to see a book such as this that pays explicit attention to institutions and culture, two themes that until not so long ago were taboo in our field but now seem to play increasingly central roles. The book contains full chapters on each, and while the discussion is naturally far from exhaustive, the authors do an excellent job summarizing some of the best work in these areas. What remains, of course, unsolved is why different nations develop different institutions and how and why such institutions change over time and how exactly cultural beliefs help determine the institutions that society ends up with.”

Continue reading here.

From Economic History Association:

“Mark Koyama and Jared Rubin. How the World Became Rich: The Historical Origins of Economic Growth. Cambridge, UK: Polity Press. x + 259 pp. $24.95 (paperback), ISBN 978-1509540235.

Reviewed for EH.Net by Joel Mokyr, Departments of Economics and History, Northwestern University.

Any scholar teaching economic history and wishing for an up-to-date survey of a large and important literature will find it useful to read this book to bone up on the recent research listed in the long and encompassing list of references.

Posted by at 9:32 AM

Labels: Book Reviews, Macro Demystified

Subscribe to: Posts