Sunday, June 19, 2022

The Economics of Cities: From Theory to Data

From a new paper by Stephen J. Redding:

“Economic activity is highly unevenly distributed within cities, as reflected in the concentration of economic functions in specific locations, such as finance in the Square Mile in London. The extent to which this concentration reflects natural advantages versus agglomeration forces is central to a range of public policy issues, including the impact of local taxation and transport infrastructure improvements. This paper reviews recent quantitative urban models, which incorporate both differences in natural advantages and agglomeration forces, and can be taken directly to observed data on cities. We show that these models can be used to estimate the strength of agglomeration forces and evaluate the impact of transportation infrastructure improvements on welfare and the spatial distribution of economic activity.”

From a new paper by Stephen J. Redding:

“Economic activity is highly unevenly distributed within cities, as reflected in the concentration of economic functions in specific locations, such as finance in the Square Mile in London. The extent to which this concentration reflects natural advantages versus agglomeration forces is central to a range of public policy issues, including the impact of local taxation and transport infrastructure improvements. This paper reviews recent quantitative urban models,

Posted by at 6:52 AM

Labels: Global Housing Watch

Friday, June 17, 2022

Housing View – June 17, 2022

On cross-country:

- Why is it so difficult to tackle the lack of affordable housing? – LSE

- There’s a desperate need for housing, so why isn’t more being built? – World Economic Forum

- What has caused the global housing crisis – and how can we fix it? – World Economic Forum

- The global house price boom may be weakening – Global Property Guide

On the US:

- The Economic Effects of Real Estate Investors – IE Business School

- Adapting to Flood Risk: Evidence from a Panel of Global Cities – NBER

- What economic policies prevented dire housing outcomes during COVID-19? – Brookings

- Waiting for Mortgage Rates to Fall? Don’t Hold Your Breath. The days of freakishly cheap loans are probably gone for good, and rates might even go up some more before they fall again. – Bloomberg

- Landlords Ready War Chests to Buy in Cooling US Housing Market. Rental companies see potential discounts ahead from homebuilders as higher mortgage rates sideline regular buyers. – Bloomberg

- Investors Bought Record Share of Homes as Mortgage Costs Climbed. Rising rates began to cool the housing market in the first quarter, but investors proved more resistant. – Bloomberg

- Rapidly Rising Building Materials and Freight Prices Push Construction Costs Higher – NAHB

- Real-Estate Firms Redfin and Compass Shed Jobs as Housing Market Slows. Companies say demand is slowing as mortgage rates rise – Wall Street Journal and New York Times

- Housing Market Cooldown Will Only Lead to More Dysfunction. The Fed had to hit the brakes on overheated home sales to control inflation, but it will be even harder now to meet future demand. – Bloomberg

- The U.S. needs more homes, but builders may be slowing construction – NPR

- U.S. Home Equity Hits Highest Level on Record—$27.8 Trillion. Soaring home prices have driven up home equity, but rising interest rates are making it more expensive to use – Wall Street Journal

- Twilight of the NIMBY. Suburban homeowners like Susan Kirsch are often blamed for worsening the nation’s housing crisis. That doesn’t mean she’s giving up her two-decade fight against 20 condos. – New York Times

- What Drove Home Price Growth and Can it Continue? – Freddie Mac

- EGC Affiliate Spotlight: Sun Kyong Lee. During a postdoctoral fellowship at EGC, the economist applied machine learning to digitize real estate transaction records and other archival data to shed light on the links between urban infrastructure investments, land use policy, and inequality. – Yale

- The Great Recession misled millennials: It made them think high home prices will eventually come down – Business Insider

- Rents climbed, a pain for tenants and policymakers alike. – New York Times

- Housing Perspectives: Short-Term Benefits of Emergency Rental Assistance Extend Beyond Housing – Harvard Joint Center for Housing Studies

- Warehousing Giants Are Consolidating in a Shifting Real-Estate Market. Industry observers say red-hot industrial property demand is cooling and some developers are reining in their rapid expansion plans – Wall Street Journal

- Does Affordable Housing Make the Surrounding Neighborhood Less Affordable? A Urban Institute research brief found that affordable housing developments in Alexandria, Virginia, were associated with a small increase in surrounding property values. – Reason

- Americans Are Building Vacation-Home Empires With Easy-Money Loans. Selling risky mortgages based on volatile per-night Airbnb income could end badly for communities, borrowers, and investors. – Bloomberg

On other countries:

- [Canada] Bank of Canada says inflation to dictate rate moves, not housing prices – Reuters

- [Canada] Home Prices in Canada Fall Again as Mortgage Pain Intensifies. Benchmark price dips to C$882,900; Ontario markets hit. Ratio of sales to new listings falls to three-year low – Bloomberg

- [Israel] Israel to boost building starts in bid to rein in soaring housing costs – Reuters

- [Korea] Young South Korean home buyers test Yoon’s vow to resolve affordability crisis – Reuters

- [New Zealand] New Zealand’s housing price boom cools as rate rises bite. Country is a test case for how property markets around the world will respond to higher interest rates – FT

- [New Zealand] New Zealand house prices fall as credit conditions hurt -REINZ – Reuters

- [Spain] Beset by uncertainties, Spanish borrowers lock in home loan rates – Reuters

- [United Kingdom] The Church of England wants to help solve the housing crisis. But building things in Britain is never straightforward – The Economist

- [United Kingdom] The ugly truth behind our rigged housing system – politicians live in fear of owners. The latest help-to-buy scheme will do little but fuel the rising prices that ministers bank on – The Guardian

- [United Kingdom] Daryl Fairweather On the Tax That Could Solve the Housing Crisis. Time to try a land value tax? – Bloomberg

On cross-country:

- Why is it so difficult to tackle the lack of affordable housing? – LSE

- There’s a desperate need for housing, so why isn’t more being built? – World Economic Forum

- What has caused the global housing crisis – and how can we fix it? – World Economic Forum

- The global house price boom may be weakening – Global Property Guide

On the US:

- The Economic Effects of Real Estate Investors – IE Business School

- Adapting to Flood Risk: Evidence from a Panel of Global Cities – NBER

- What economic policies prevented dire housing outcomes during COVID-19?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, June 16, 2022

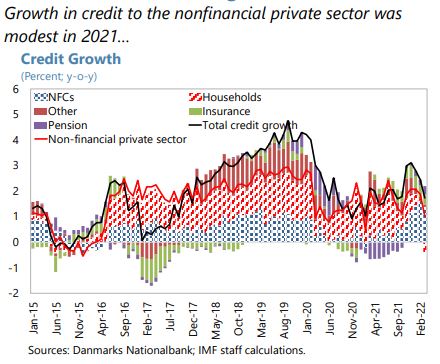

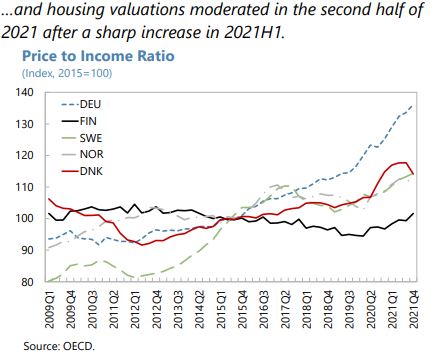

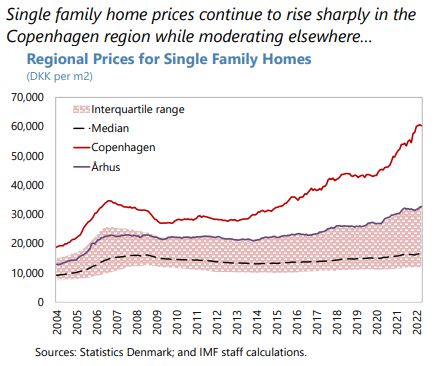

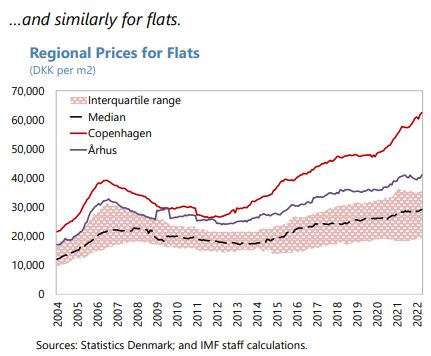

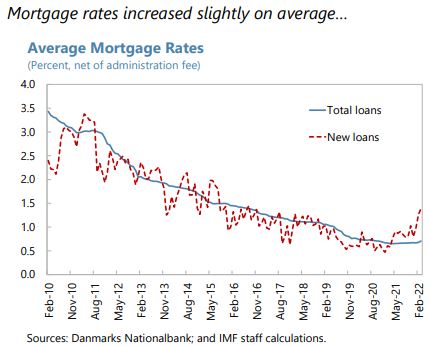

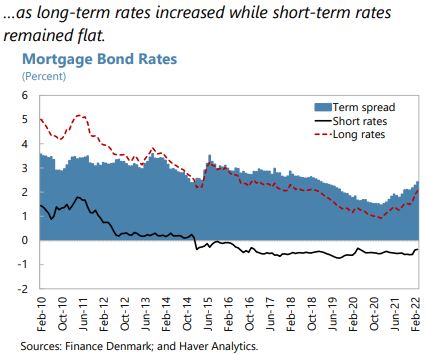

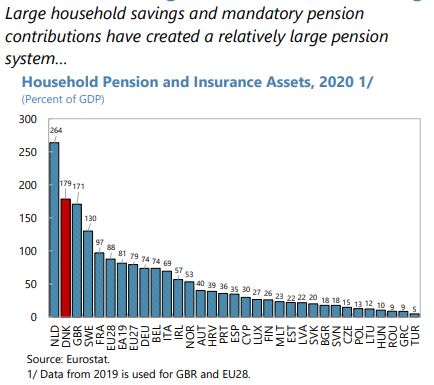

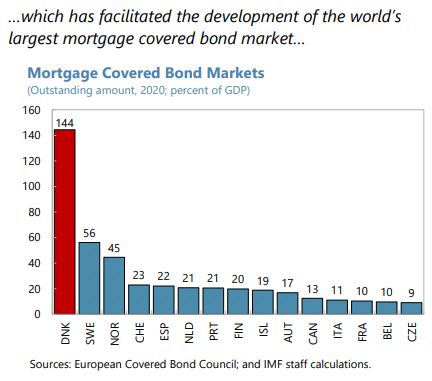

Housing Market in Denmark

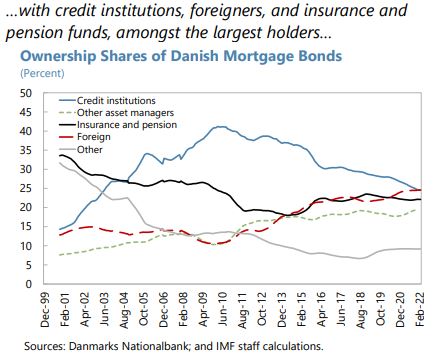

From the IMF’s latest report on Denmark:

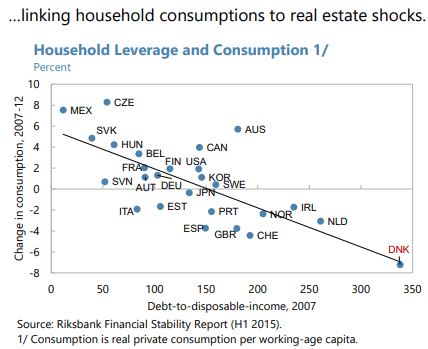

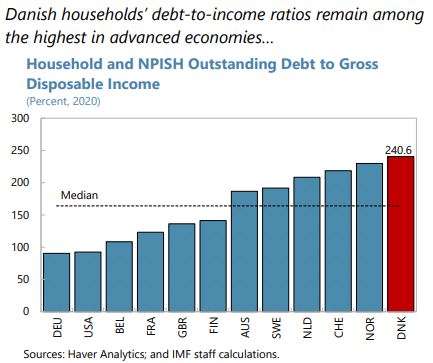

“Macrofinancial vulnerabilities remain elevated. Household leverage remains high by international standards and housing prices rose faster than incomes through the pandemic. Furthermore, a sizable share of newly-originated loans were interest-only loans, some with amortizing options that could be exercised by lenders if housing values fall. In addition, homeowners are increasingly taking out variable-rate mortgage loans and repaying fixed-rate loans which naturally increases the interest-rate sensitivity of homeowners. Thus, a domestic or regional house price correction, triggered possibly by a reassessment of fundamentals or a tightening of global financial conditions could reverberate in Denmark, weighing on the real estate market, private consumption, and investment. The impact could be amplified by the high interconnectedness of mortgage credit institutions (MCIs), pension funds, and insurance companies given their dependence on the housing sector. While the net impact is uncertain, high, and persistent inflation could weigh on bank profitability including through lower aggregate demand, or if highly-leveraged households cannot service their debt due to variable-rate mortgages resetting at higher rates.

(…)

They recognize that macrofinancial risks mainly stem from the housing market in combination with high household leverage and an increasing share of risky mortgages.

(…)

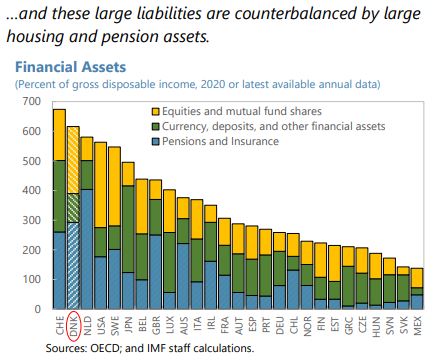

Macrofinancial vulnerabilities persist due to high leverage and an increasing share of risky mortgages. Following a prolonged period of low interest rates, high debt, combined with illiquid assets (concentrated in real estate via housing and pension assets), exposes households to price and interest rate shocks that can spill over to aggregate demand. Furthermore, many households have recently opted for interest-only mortgages with options for lenders to request amortization if housing prices fall, which could amplify adverse shocks. Many of these households would face markedly higher debt-servicing costs were they required to amortize their mortgages (DN 2021). A sharp revaluation could harm highly-leveraged households, particularly those who purchased in overvalued urban areas and low-income households. These vulnerabilities are compounded by the large and growing proportion of variable-rate mortgages, which are increasingly used to repay fixed-rate loans, exposing homeowners to higher interest rate risk. Moreover, MCIs and pension and insurance companies are highly interconnected and dependent on the health of the housing sector.

(…)

These developments warrant tightening prudential tools. Macroprudential tools aim to increase macrofinancial resilience and contain excessive risk taking. Staff recommend that new mortgages extended to highly-leveraged households be subject to minimum down-payment requirements or mandatory amortization until a minimum equity share is reached, regardless of maturity and type of interest rate fixation. As valuation-based measures can be less binding when housing prices appreciate rapidly (Chen et. al, 2020), the limits applying to ”highly-leveraged” borrowers should become binding if either DTI or loan-to-value (LTV) limit is breached, instead of the current joint requirement. Based on borrowers’ riskiness, differentiated limits on income-based measures and LTVs for interest-only and floating-rate mortgages should also be considered. In an environment of increasing mortgage rates, the “growth area guidelines” should be extended beyond Copenhagen and Aarhus and debt-service-to-income (DSTI) caps should be considered to protect against liquidity shocks. The proposed risk-based prudential framework should facilitate calibration of these measures, to account for risk differentiation across groups, e.g., first-time home buyers to improve affordability. National legislation should include borrower-based tools (limits on LTVs, DTIs, and DSTIs) in the policy toolkit (FSAP 2020).

To improve affordability, it is important to address features of the tax code and housing supply constraints that create price pressures. Incentives for the adequate supply of housing should be reviewed. Moreover, rent controls in Denmark are pervasive relative to peer countries. Once inflationary pressures abate, these should be relaxed to stimulate the rental market, while protecting the most vulnerable. Mortgage interest deductibility should be reduced as in other advanced economies, as this incentivizes larger housing purchases and higher indebtedness, pushing up prices (Gruber et. al, 2019). Linking property taxes to market valuations should be prioritized.”

From the IMF’s latest report on Denmark:

“Macrofinancial vulnerabilities remain elevated. Household leverage remains high by international standards and housing prices rose faster than incomes through the pandemic. Furthermore, a sizable share of newly-originated loans were interest-only loans, some with amortizing options that could be exercised by lenders if housing values fall. In addition, homeowners are increasingly taking out variable-rate mortgage loans and repaying fixed-rate loans which naturally increases the interest-rate sensitivity of homeowners.

Posted by at 12:07 PM

Labels: Global Housing Watch

Tuesday, June 14, 2022

Some Stock Market Benchmarks

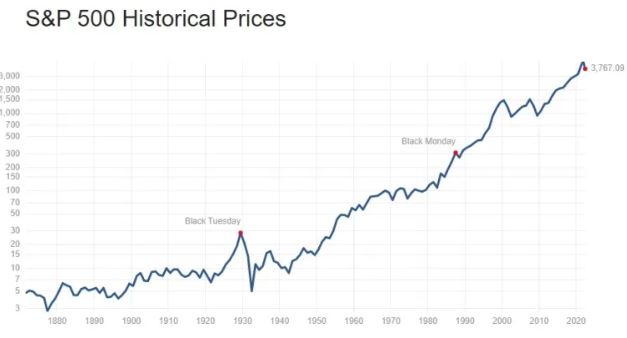

From Conversable Economist:

“When I get the quarterly announcements for what my retirement account is now worth, and a drop in the stock market has caused the total in the account to decline, I find myself looking at some of the long-run patterns in stock market prices.

To set the stage, here’s the historical pattern of the S&P stock index since back in the 19th century. In interpreting the figure, notice that the vertical axis is a logarithmic axis showing proportional changes; for example, the tripling from 10 to 30 is the same size as the tripling from 100 to 300 and the same as the tripling from 1000 to 3000. (Without using a log scale, all the smaller values–like the stock market crash of 1929, would just be a little squiggle what would look like a nearly flat line on the far left of the figure.) You can see some of the well-known changes in the stock market over time: the run-up of the 1920s, the crash of 1929, the run-up of the 1960s, the comparatively flat market of the 1970s, a big jump in the dot-com market of the 1990s, the run-up since 2009, and the recent decline. Of course, whenever you consider the possibility that the

For a slightly different view, here is the same set of data, this time adjusted for inflation. Again, the vertical axis shows proportional change. Again, the main well-known changes are pretty visible, but they don’t all look the same. For example, after adjusting for inflation, the Black Tuesday stock market decline in the 1920s looks even more striking, and during the high-inflation 1970s, the real value of the S&P 500 index is falling.

Of course, stock market values should be affected by expectations of corporate earnings. Thus, the standard price-earnings measure of the stock market looks at stock prices divided by corporate earnings over the previous 12 months. Notice that the logarithmic scales have now gone away. Corporate earnings will rise over the long run both because of inflation and along with overall growth in the economy. Thus, one might expect to see the P/E ratio be roughly the same over time, of course with some fluctuations as economic events and market trends interact. Indeed, when you try to find the 1929 stock market crash in this data, it’s barely apparent: after all, if both stock prices and corporate earnings collapse at about the same time, then the ratio of the two may not move in an especially dramatic way.”

From Conversable Economist:

“When I get the quarterly announcements for what my retirement account is now worth, and a drop in the stock market has caused the total in the account to decline, I find myself looking at some of the long-run patterns in stock market prices.

To set the stage, here’s the historical pattern of the S&P stock index since back in the 19th century.

Posted by at 8:10 AM

Labels: Macro Demystified

Saturday, June 11, 2022

Dale W. Jorgenson: An Intellectual Biography

Profile by John Fernald (INSEAD and Federal Reserve Bank of San Francisco):

“Dale W. Jorgenson has been a central contributor to a wide range of economic and policy issues over a long and productive career. His research is characterized by a tight integration of economic theory, appropriate data that matches the theory, and sound econometrics. His groundbreaking work on the theory and empirics of investment established the research path for the economics profession. He is a founder of modern growth accounting: Official statistics in many countries, including the United States, implement Jorgenson’s methods. Relatedly, without Jorgenson’s unflagging efforts, consistent industry KLEMS datasets for many countries—which have been widely used in recent decades for growth accounting, econometrics, and other applications—would not exist. Jorgenson is also a pioneer in econometric modeling of producer and consumer behavior and of econometrically estimated, intertemporal general equilibrium modeling for policy analysis.”

Also, see an article in the Wall Street Journal by James R. Hagerty: “Harvard Economist Dale Jorgenson Found Better Ways to Gauge Productivity. Professor, who has died at age 89, removed much of the mystery from studies of what drives economic growth”.

Profile by John Fernald (INSEAD and Federal Reserve Bank of San Francisco):

“Dale W. Jorgenson has been a central contributor to a wide range of economic and policy issues over a long and productive career. His research is characterized by a tight integration of economic theory, appropriate data that matches the theory, and sound econometrics. His groundbreaking work on the theory and empirics of investment established the research path for the economics profession.

Posted by at 11:48 AM

Labels: Profiles of Economists

Subscribe to: Posts