Thursday, June 16, 2022

Housing Market in Denmark

From the IMF’s latest report on Denmark:

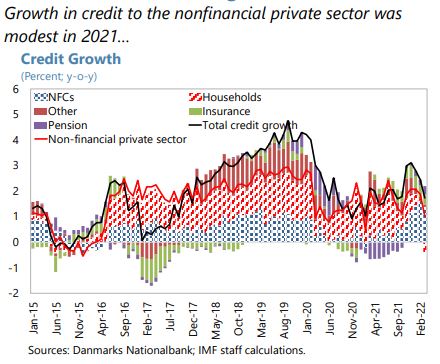

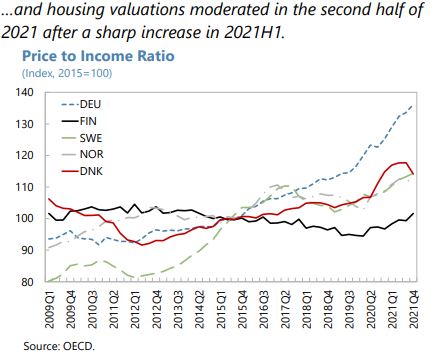

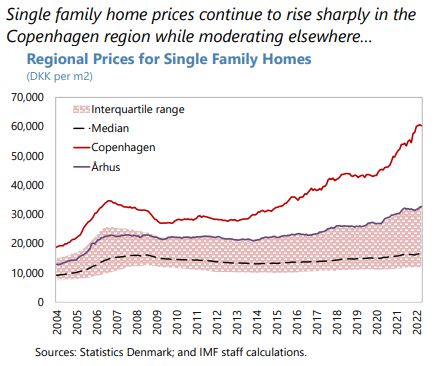

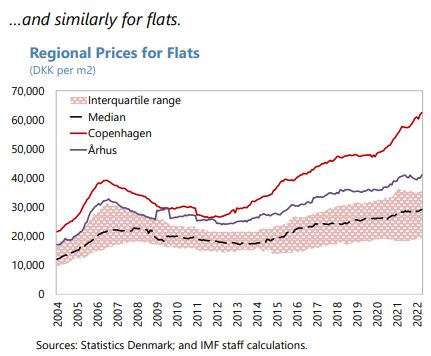

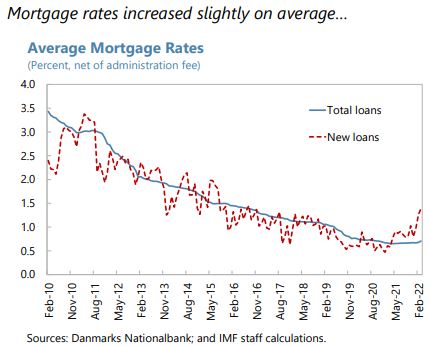

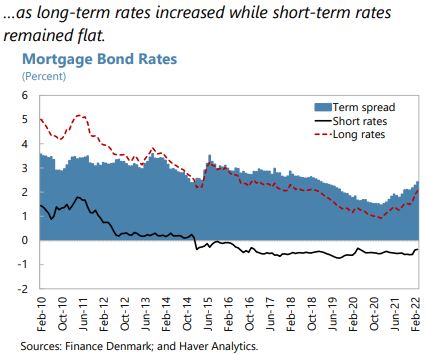

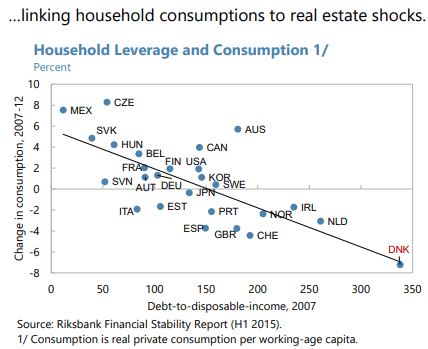

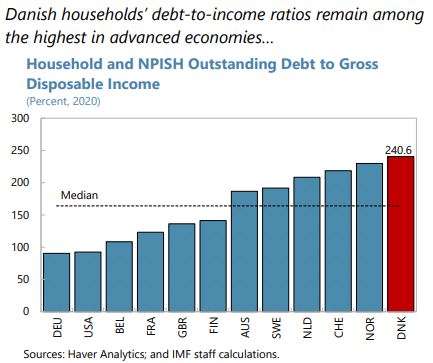

“Macrofinancial vulnerabilities remain elevated. Household leverage remains high by international standards and housing prices rose faster than incomes through the pandemic. Furthermore, a sizable share of newly-originated loans were interest-only loans, some with amortizing options that could be exercised by lenders if housing values fall. In addition, homeowners are increasingly taking out variable-rate mortgage loans and repaying fixed-rate loans which naturally increases the interest-rate sensitivity of homeowners. Thus, a domestic or regional house price correction, triggered possibly by a reassessment of fundamentals or a tightening of global financial conditions could reverberate in Denmark, weighing on the real estate market, private consumption, and investment. The impact could be amplified by the high interconnectedness of mortgage credit institutions (MCIs), pension funds, and insurance companies given their dependence on the housing sector. While the net impact is uncertain, high, and persistent inflation could weigh on bank profitability including through lower aggregate demand, or if highly-leveraged households cannot service their debt due to variable-rate mortgages resetting at higher rates.

(…)

They recognize that macrofinancial risks mainly stem from the housing market in combination with high household leverage and an increasing share of risky mortgages.

(…)

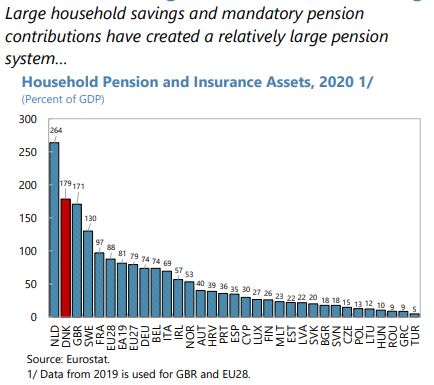

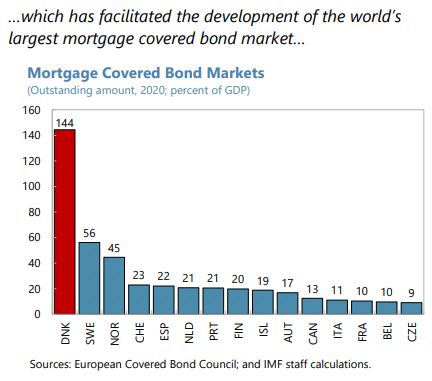

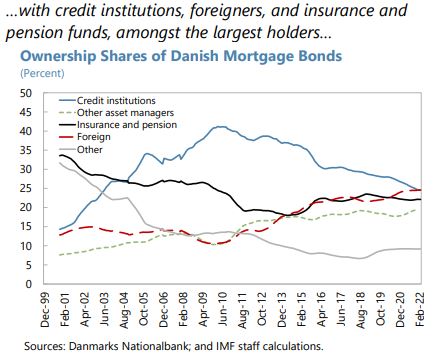

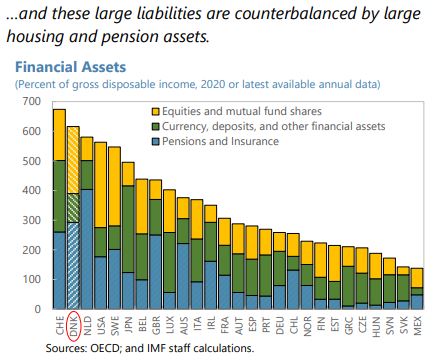

Macrofinancial vulnerabilities persist due to high leverage and an increasing share of risky mortgages. Following a prolonged period of low interest rates, high debt, combined with illiquid assets (concentrated in real estate via housing and pension assets), exposes households to price and interest rate shocks that can spill over to aggregate demand. Furthermore, many households have recently opted for interest-only mortgages with options for lenders to request amortization if housing prices fall, which could amplify adverse shocks. Many of these households would face markedly higher debt-servicing costs were they required to amortize their mortgages (DN 2021). A sharp revaluation could harm highly-leveraged households, particularly those who purchased in overvalued urban areas and low-income households. These vulnerabilities are compounded by the large and growing proportion of variable-rate mortgages, which are increasingly used to repay fixed-rate loans, exposing homeowners to higher interest rate risk. Moreover, MCIs and pension and insurance companies are highly interconnected and dependent on the health of the housing sector.

(…)

These developments warrant tightening prudential tools. Macroprudential tools aim to increase macrofinancial resilience and contain excessive risk taking. Staff recommend that new mortgages extended to highly-leveraged households be subject to minimum down-payment requirements or mandatory amortization until a minimum equity share is reached, regardless of maturity and type of interest rate fixation. As valuation-based measures can be less binding when housing prices appreciate rapidly (Chen et. al, 2020), the limits applying to ”highly-leveraged” borrowers should become binding if either DTI or loan-to-value (LTV) limit is breached, instead of the current joint requirement. Based on borrowers’ riskiness, differentiated limits on income-based measures and LTVs for interest-only and floating-rate mortgages should also be considered. In an environment of increasing mortgage rates, the “growth area guidelines” should be extended beyond Copenhagen and Aarhus and debt-service-to-income (DSTI) caps should be considered to protect against liquidity shocks. The proposed risk-based prudential framework should facilitate calibration of these measures, to account for risk differentiation across groups, e.g., first-time home buyers to improve affordability. National legislation should include borrower-based tools (limits on LTVs, DTIs, and DSTIs) in the policy toolkit (FSAP 2020).

To improve affordability, it is important to address features of the tax code and housing supply constraints that create price pressures. Incentives for the adequate supply of housing should be reviewed. Moreover, rent controls in Denmark are pervasive relative to peer countries. Once inflationary pressures abate, these should be relaxed to stimulate the rental market, while protecting the most vulnerable. Mortgage interest deductibility should be reduced as in other advanced economies, as this incentivizes larger housing purchases and higher indebtedness, pushing up prices (Gruber et. al, 2019). Linking property taxes to market valuations should be prioritized.”

Posted by at 12:07 PM

Labels: Global Housing Watch

Subscribe to: Posts