Tuesday, June 21, 2022

Housing Market in Greece

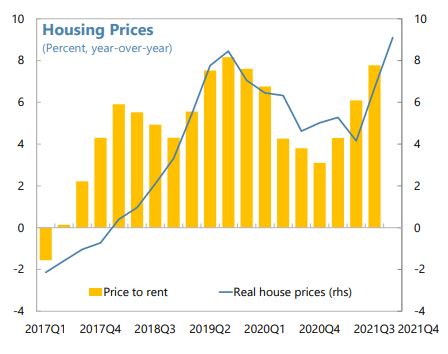

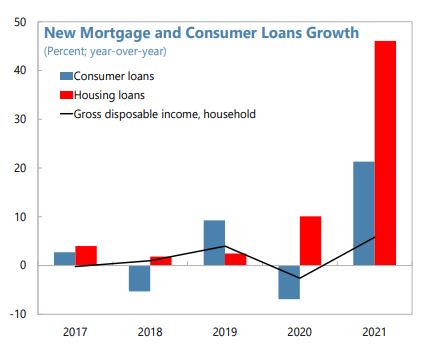

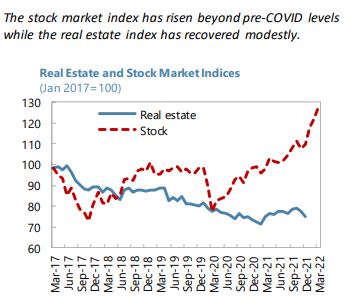

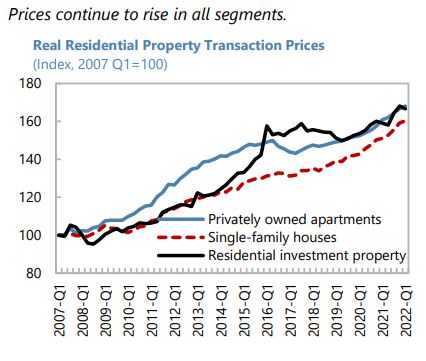

From IMF’s latest report on Greece:

“There are nascent signs of emerging systemic vulnerabilities. Residential real estate prices have rebounded by almost 25 percent since 2018, accompanied by a significant increase in price-to-rent and income ratios. Commercial real estate prices have also rebounded, albeit to a weaker extent. Household credit expansion has surpassed disposable income growth, with demand for mortgage and corporate loans expected to mirror the recent rise in new lending to households and corporates, although after a period of pronounced private sector deleveraging (…). Model-based analyses suggest positive private sector credit gaps for Greece. A further acceleration of credit growth is anticipated from NGEU loans being channeled through the banking system.”

From IMF’s latest report on Greece:

“There are nascent signs of emerging systemic vulnerabilities. Residential real estate prices have rebounded by almost 25 percent since 2018, accompanied by a significant increase in price-to-rent and income ratios. Commercial real estate prices have also rebounded, albeit to a weaker extent. Household credit expansion has surpassed disposable income growth, with demand for mortgage and corporate loans expected to mirror the recent rise in new lending to households and corporates,

Posted by at 8:53 PM

Labels: Global Housing Watch

Housing Market in Qatar

Posted by at 8:48 PM

Labels: Global Housing Watch

Monday, June 20, 2022

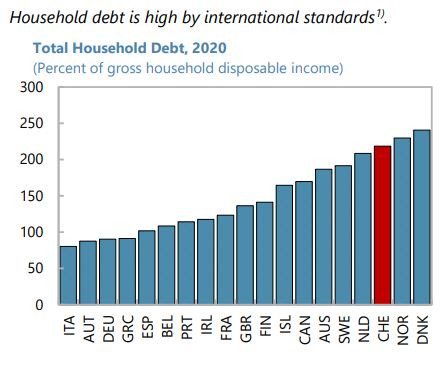

Housing Market in Switzerland

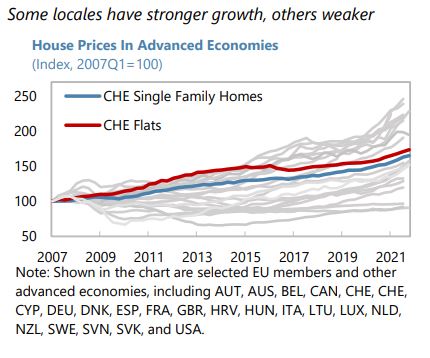

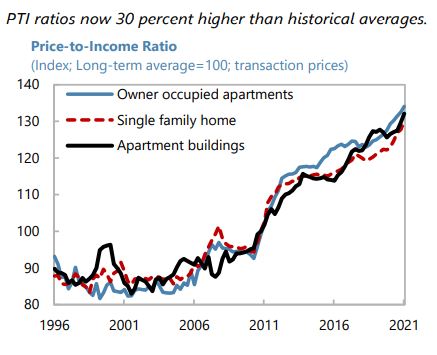

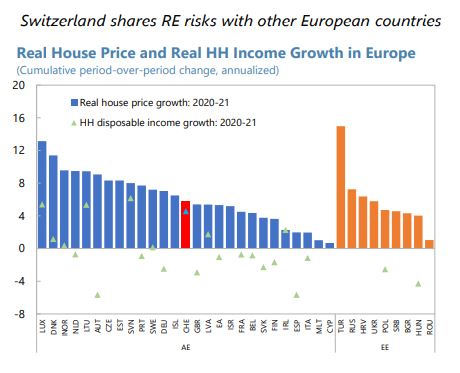

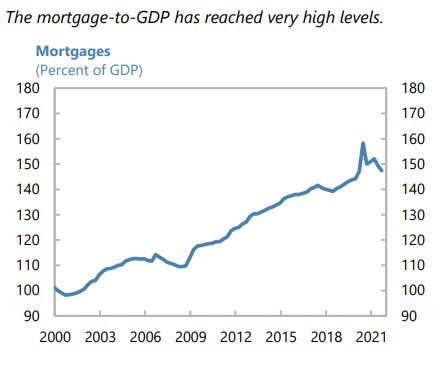

From the IMF’s latest report on Switzerland:

“With further housing price increases, the sectoral CCyB was reactivated at the maximum 2.5 percent, effective September 2022. (…) This has alleviated downward inflation pressures, but brought side-effects (balance-sheet expansion, profitability pressures, higher housing prices). (…) Housing prices have risen relative to fundamentals (overvaluation estimates are 5–30 percent for apartments), with search-for-yield and robust mortgage lending. A sharp tightening of conditions could trigger sell-offs in the investment-led segment and increase affordability concerns in general. Price corrections could lead to defaults and pressures on capital buffers. Domestically-focused banks are vulnerable to interest-rate shocks, given duration gaps; the largest banks are exposed to international clients via leveraged and Lombard loans, to counterparty credit risk in derivative and trading activities, to market and basis risk (under volatile conditions), and to business risk from lower asset management flows, including linked to the war in Ukraine. Risks related to crypto assets and cyberattacks have increased with the war, although incidents have remained contained; sanctions have increased compliance and financial-integrity risks.”

From the IMF’s latest report on Switzerland:

“With further housing price increases, the sectoral CCyB was reactivated at the maximum 2.5 percent, effective September 2022. (…) This has alleviated downward inflation pressures, but brought side-effects (balance-sheet expansion, profitability pressures, higher housing prices). (…) Housing prices have risen relative to fundamentals (overvaluation estimates are 5–30 percent for apartments), with search-for-yield and robust mortgage lending. A sharp tightening of conditions could trigger sell-offs in the investment-led segment and increase affordability concerns in general.

Posted by at 9:33 AM

Labels: Global Housing Watch

A Forward Looking Approach to Calibrate Macroprudential Tools in Switzerland

From the IMF’s latest report on Switzerland:

“Housing matters for economic activity and financial stability in Switzerland. The mortgage market is large relative to the size of the economy and banks are heavily exposed. House prices have significantly outpaced income growth, and this trend has accentuated during the pandemic. The Swiss authorities have taken decisive action to address unsustainable developments, but vulnerabilities have increased. This paper shows that a fuller set of macroprudential tools can be more effective to reduce systemic risk. Adequate calibration and a forward-looking approach are key given lags between policy announcements and policy effects. The paper quantifies a suite of LTV/DSTI caps, amortization requirements, and ‘speed limits’ calibrated at the vintage level to guard against the build-up of vulnerabilities and strengthen resilience.”

From the IMF’s latest report on Switzerland:

“Housing matters for economic activity and financial stability in Switzerland. The mortgage market is large relative to the size of the economy and banks are heavily exposed. House prices have significantly outpaced income growth, and this trend has accentuated during the pandemic. The Swiss authorities have taken decisive action to address unsustainable developments, but vulnerabilities have increased. This paper shows that a fuller set of macroprudential tools can be more effective to reduce systemic risk.

Posted by at 9:24 AM

Labels: Global Housing Watch

Sunday, June 19, 2022

Work From Home and the Office Real Estate Apocalypse

From a new working paper by Arpit Gupta, Vrinda Mittal and Stijn Van Nieuwerburgh:

“We study the impact of remote work on the commercial office sector. We document large shifts in lease revenues, office occupancy, lease renewal rates, lease durations, and market rents as firms shifted to remote work in the wake of the Covid-19 pandemic. We show that the pandemic has had large effects on both current and expected future cash flows for office buildings. Remote work also changes the risk premium on office real estate. We revalue the stock of New York City commercial office buildings taking into account pandemic-induced cash flow and discount rate effects. We find a 32% decline in office values in 2020 and 28% in the longer-run, the latter representing a $500 billion value destruction. Higher quality office buildings were somewhat buffered against these trends due to a flight to quality, while lower quality office buildings see much more dramatic swings. These valuation changes have repercussions for local public finances and financial sector stability.”

From a new working paper by Arpit Gupta, Vrinda Mittal and Stijn Van Nieuwerburgh:

“We study the impact of remote work on the commercial office sector. We document large shifts in lease revenues, office occupancy, lease renewal rates, lease durations, and market rents as firms shifted to remote work in the wake of the Covid-19 pandemic. We show that the pandemic has had large effects on both current and expected future cash flows for office buildings.

Posted by at 9:29 AM

Labels: Global Housing Watch

Subscribe to: Posts