Monday, June 20, 2022

Housing Market in Switzerland

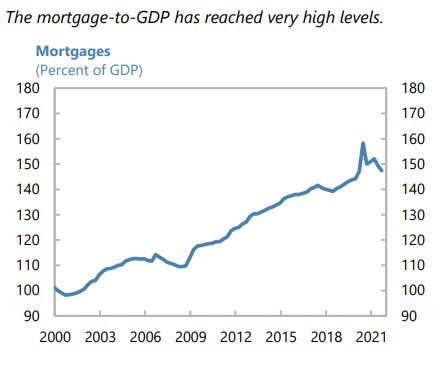

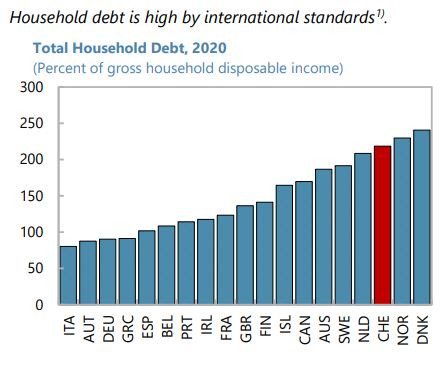

From the IMF’s latest report on Switzerland:

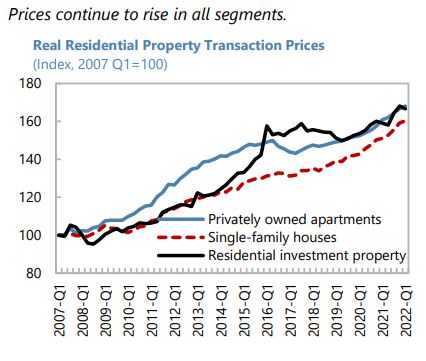

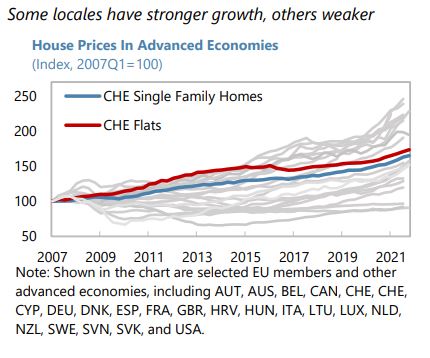

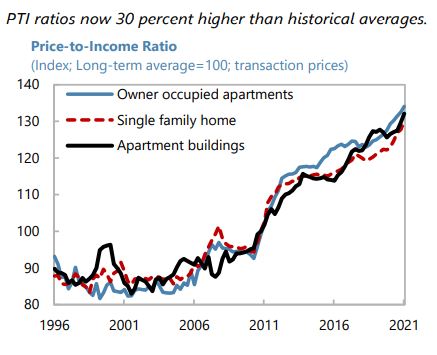

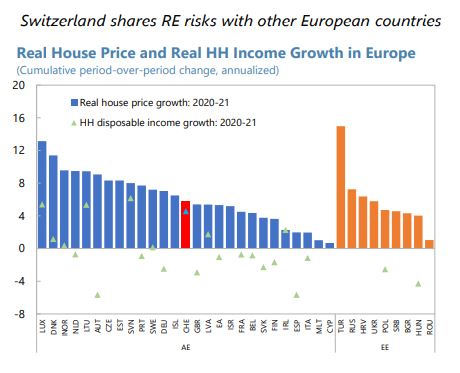

“With further housing price increases, the sectoral CCyB was reactivated at the maximum 2.5 percent, effective September 2022. (…) This has alleviated downward inflation pressures, but brought side-effects (balance-sheet expansion, profitability pressures, higher housing prices). (…) Housing prices have risen relative to fundamentals (overvaluation estimates are 5–30 percent for apartments), with search-for-yield and robust mortgage lending. A sharp tightening of conditions could trigger sell-offs in the investment-led segment and increase affordability concerns in general. Price corrections could lead to defaults and pressures on capital buffers. Domestically-focused banks are vulnerable to interest-rate shocks, given duration gaps; the largest banks are exposed to international clients via leveraged and Lombard loans, to counterparty credit risk in derivative and trading activities, to market and basis risk (under volatile conditions), and to business risk from lower asset management flows, including linked to the war in Ukraine. Risks related to crypto assets and cyberattacks have increased with the war, although incidents have remained contained; sanctions have increased compliance and financial-integrity risks.”

Posted by at 9:33 AM

Labels: Global Housing Watch

Subscribe to: Posts