Friday, April 15, 2022

Housing View – April 15, 2022

On the US:

- The American property market is once again looking bubbly. Soaring mortgage rates have yet to cool exuberant demand – The Economist

- The housing market is running hot. Can the Fed cool it before it crashes? S&P Global considers 88% of U.S housing regions overvalued – Market Watch

- Early signs of cooling housing market seen in some U.S. cities, Redfin says – Reuters

- The new risk to the housing market – Politico

- What Higher Mortgage Rates Mean for the Housing Market. Wharton’s Benjamin Keys explains why higher mortgage interest rates are discouraging home buyers, but not for long. – Wharton

- Homebuyers Get Desperate in Overheated U.S. Spring Sales Season. Soaring mortgage rates and prices are fueling a rush to seal a deal in market where competition for houses is intense. – Bloomberg

- Fed’s Quantitative Tightening Throws a Wrench Into Mortgage-Bond Market. Investors have been cautious with mortgage bonds, and the Fed’s latest policy signals are unlikely to resolve all their concerns – Wall Street Journal

- Senators Romney, Lee Introduce Bill to Increase Utah Housing Supply – Mitt Romney

- The Landscape of Middle-Income Housing Affordability in California – Terner Center

- Raise Residential Taxes? Bring in Casinos? Cities Look at Ways to Bolster Budgets. Leaders in urban areas struggling with pandemic hits to business and travel revenues are brainstorming longer-term strategies – Wall Street Journal

- How Homeownership Changes You. It’s not just a financial commitment. It can alter people’s relationships to a community, a place, and even time. – The Atlantic

- House-flipping algorithms are coming to your neighborhood. Despite millions of dollars in losses, iBuying’s failure doesn’t signal the end of tech-led disruption, just a fumbled beginning. – Bloomberg

- Pandemic-fueled suburban growth doesn’t mean we should abandon climate resiliency – Brookings

- Understanding the U.S. Housing Crisis in an Era of Inflation. Economist Jenny Schuetz offers a practical guide to one of the biggest challenges facing renters and homebuyers: the skyrocketing cost of housing. – Bloomberg

On China

- China Banks Allow Mortgage Payment Holiday in Covid-Hit Shanghai. Shanghai reports record new infections as lockdown extended. Megabanks’ profit growth at risk amid Covid, property weakness – Bloomberg

On other countries:

- [Australia] Melbourne and Sydney suburbs lead housing value declines – CoreLogic

- [Canada] Canada targets housing, banks in modest-spending budget – Reuters

- [Canada] Canada plans to double homebuilding in decade, but where are the workers? – Reuters

- [Canada] ‘The Top Is Off’: Home Prices Show Signs of Cracking in Canada’s Hot Market. Industry experts are predicting Canada’s home prices could finally start to decline after a 50% surge over the past two years. – Bloomberg

- [Canada] Bank of Canada rate hike could cool Canada’s hot housing markets, economists say – The Globe and Mail

- [Hong Kong] The coming end of ‘property hegemony’. Rising inequality and the deterioration of living conditions and standards among ordinary people – the alleged underlying sources of the 2019 unrest – have been blamed on the dominance of the real estate sector. Beijing may want the next chief executive to crack down – South China Morning Post

- [New Zealand] New Zealand house prices fall as interest rates and inflation weigh – Reuters

- [New Zealand] New Zealand house prices are starting to fall – but many buyers remain locked out. Some economists are predicting a 10% decrease over the year, but even that won’t return prices to those of two years ago – The Guardian

- [United Kingdom] Home Ownership and the UK Mortgage Market: An International Review – Institute for Global Change

- [United Kingdom] Stamp duty holiday tempted buyers into ‘marathon’ loans. Many homebuyers opted for mortgages of 35 years or more – The Guardian

- [United Kingdom] Breathing rooms: pollution and the property market. Air quality could become as important to homebuyers as price per square foot, proximity to schools and transport links – FT

On the US:

- The American property market is once again looking bubbly. Soaring mortgage rates have yet to cool exuberant demand – The Economist

- The housing market is running hot. Can the Fed cool it before it crashes? S&P Global considers 88% of U.S housing regions overvalued – Market Watch

- Early signs of cooling housing market seen in some U.S. cities, Redfin says – Reuters

- The new risk to the housing market – Politico

- What Higher Mortgage Rates Mean for the Housing Market.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, April 14, 2022

World Wealth: Human, Physical, and Natural

From the Conversable Economist:

“The wealth of a society is so much more than the value of houses, or the stock market, or retirement accounts. Wealth broadly understood should also include endowments of nature, ranging from wilderness to oil wells, as well as the human capital embodied in the education and skills of its people. Every few years, the World Bank takes on the task of measuring the world’s wealth in these broader ways. The most recent set of estimates appear in The Changing Wealth of Nations 2021 : Managing Assets for the Future.

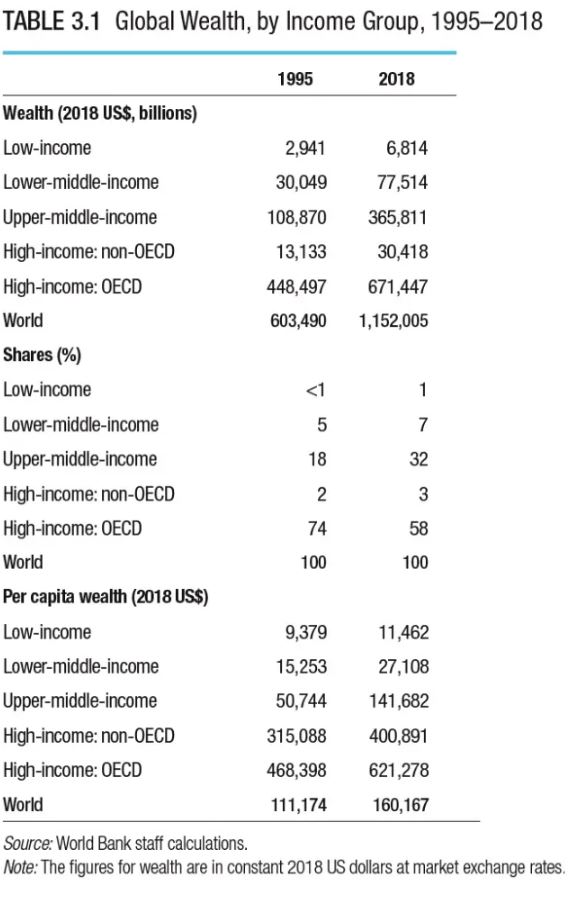

Just to be clear, wealth represents an accumulation over time. This is different from GDP, which is the amount produced in a given year. Thus, world GDP in 2018 was about $86 trillion, but world wealth as estimated in this report was 13 times bigger at $1,152 trillion. Here are some estimates from “Chapter 3: Global and Regional Trends in

Wealth, 1995–2018,” by Glenn-Marie Lange, Diego Herrera, and Esther Naikal.

Here is how wealth was distributed around the world between countries of different income levels (I have left out some intermediate years in the table):”

From the Conversable Economist:

“The wealth of a society is so much more than the value of houses, or the stock market, or retirement accounts. Wealth broadly understood should also include endowments of nature, ranging from wilderness to oil wells, as well as the human capital embodied in the education and skills of its people. Every few years, the World Bank takes on the task of measuring the world’s wealth in these broader ways.

Posted by at 1:17 PM

Labels: Macro Demystified

Wednesday, April 13, 2022

GDP vs. GNP

From Marginal Revolution:

“As a metric of how well economes are doing, gdp is underrated, as I argue in my latest Bloomberg column. Here is one bit:

If a nation has a lot of foreign direct investment, as does Ireland, GDP will exceed GNP by a considerable amount. According to the Irish government, the country’s GDP is about 370 billion euros. Its GNP is less than 300 billion euros. The difference in GDP and GNP is largely accounted for by the outflow of profits to foreign-owned multinationals.

This isn’t just a story about Ireland. Many other nations have had significant differences between their GDP and GNP, including many developing nations and, at times, Singapore.

The conventional wisdom is that GNP is the proper measure of living standards, because domestic citizens do not have claims on the profits of foreign multinationals. That isn’t wrong, but it is also an incomplete answer. When it comes to the future prospects of a country, GDP is a better indicator. Countries that have a high ratio of GDP to GNP are especially promising, though there are some caveats.

A relatively high GDP is a sign that a large number of foreign companies view the future of the domestic economy as bright. They are “putting their money where their mouth is.”

In the case of Ireland, the country is now the only member of the European Union in which English is the main language not only for business but also for schools and public life. Foreign investors are drawn by that fact. They also see that Ireland is relatively underpopulated, and appears to be receptive to absorbing talented foreign immigrants. Furthermore, Ireland is ruled by mainstream parties and seems largely unaffected by the populism and nativism that are creating problems elsewhere in Europe.

All these realities are reason to be bullish. It is also reasonable to expect that the Irish government will be relatively friendly to business looking forward.”

From Marginal Revolution:

“As a metric of how well economes are doing, gdp is underrated, as I argue in my latest Bloomberg column. Here is one bit:

If a nation has a lot of foreign direct investment, as does Ireland, GDP will exceed GNP by a considerable amount. According to the Irish government, the country’s GDP is about 370 billion euros. Its GNP is less than 300 billion euros.

Posted by at 2:25 PM

Labels: Macro Demystified

Housing Market in Macao

From the IMF’s latest report on Macao:

“Staff reiterates its call to phase out the residency-based LTV capital flow management measure and macroprudential measure (IMF Country Report No. 19/123, Appendix IV). The authorities have introduced this measure in response to a potential risk from soaring property prices fueled by demand from non-residents. However, since 2019 this risk has abated as residential prices have plateaued and residential property transactions by non-residents have fallen. Linking the differentiation in LTV limits directly to banks’ risk assessment of loans and borrowers could attain the same objective without residency-based differentiation.”

From the IMF’s latest report on Macao:

“Staff reiterates its call to phase out the residency-based LTV capital flow management measure and macroprudential measure (IMF Country Report No. 19/123, Appendix IV). The authorities have introduced this measure in response to a potential risk from soaring property prices fueled by demand from non-residents. However, since 2019 this risk has abated as residential prices have plateaued and residential property transactions by non-residents have fallen.

Posted by at 4:56 AM

Labels: Global Housing Watch

Sunday, April 10, 2022

Five reasons China’s productivity slowed down

From Noahpinion:

“It’s always an interesting experience to read books about China’s economy from before 2018 or so. So many world-shaking events have changed the story since then — Trump’s trade war, Covid, Xi’s industrial crackdowns, the real estate bust, lockdowns, Russia’s invasion of Ukraine. Reading predictions of China’s evolution from before these events occurred is a little like reading sci-fi from 1962.

When I started China’s Economy: What Everyone Needs to Know®, by the veteran economic consultant Arthur Kroeber, I was prepared for this surreal effect. After all, it was published in April 2016 — not the most opportune timing. So I was pleasantly surprised by how relevant the book still felt. Most of the book’s explanations of aspects of the Chinese economy — fiscal federalism, urbanization and real estate construction, corruption, Chinese firms’ position within the supply chain, etc. — are either still highly relevant, or provide important explanations of what Xi’s policies were reacting against. Dan Wang was not wrong to recommend that I read it.

But China’s Economy is still a book from 2016, and through it all runs a strain of stubborn optimism that seems a lot less justifiable six years later. Most crucially, while Kroeber acknowledged many of China’s economic challenges — an unsustainable pace of real estate construction, low efficiency of capital, an imbalance between investment and consumption, and so on — he argued that China would eventually overcome these challenges by shifting from an extensive growth model based on resource mobilization to one based on greater efficiency and productivity improvements. This was despite his acknowledgement of the fact that productivity growth had already slowed well before 2016, and that Xi’s policies so far didn’t seem up to the challenge of reviving it.

In many ways, productivity growth is the thread that ties together the entire story of the Chinese economy since 2008. Basic economic theory says that eventually the growth benefits of capital accumulation hit a wall, and you have to improve technology and/or efficiency to keep growth going. Some countries, like Japan, South Korea, Singapore, and Taiwan, have done this successfully, and are now rich; other, like Thailand, failed to do it and are now languishing at the middle income level. For several decades, Chinese productivity growth looked like Japan’s or Korea’s did. But slightly before Xi came to power, it downshifted to look a bit more like Thailand. Here’s a graph from the Lowy Institute’s recent report:”

From Noahpinion:

“It’s always an interesting experience to read books about China’s economy from before 2018 or so. So many world-shaking events have changed the story since then — Trump’s trade war, Covid, Xi’s industrial crackdowns, the real estate bust, lockdowns, Russia’s invasion of Ukraine. Reading predictions of China’s evolution from before these events occurred is a little like reading sci-fi from 1962.

When I started China’s Economy: What Everyone Needs to Know®,

Posted by at 7:58 AM

Labels: Macro Demystified

Subscribe to: Posts