Wednesday, April 27, 2022

Lessons Learned from Housing Policy during COVID-19

From a new work at Brookings by Kris Gerardi, Lauren Lambie-Hanson, Paul Willen, Laurie Goodman, and Susan Wachter:

“Evidence on housing policy

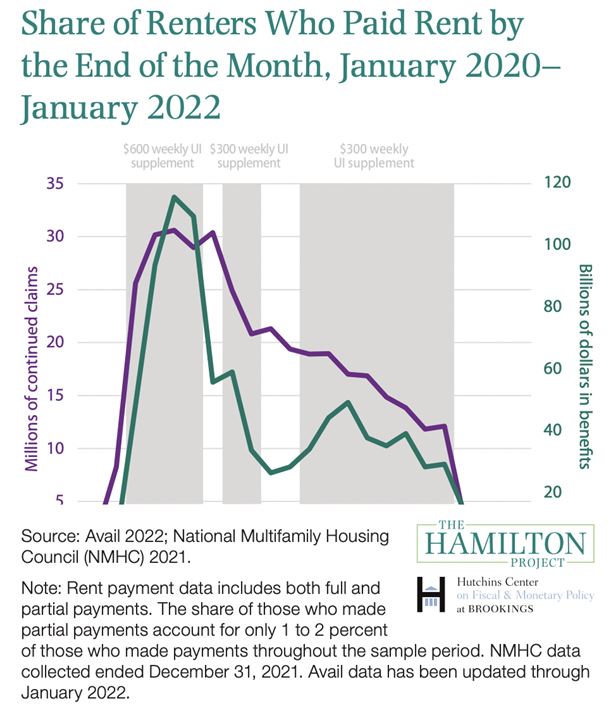

- The national forbearance mandate, foreclosure moratorium, enhanced Unemployment Insurance (UI), and Economic Impact Payments (EIPs) aided in reducing financial distress for both owners and renters at the outset of the pandemic and prevented longer-run problems in mortgage and housing markets.

- Over 80 percent of borrowers who missed a mortgage payment in the first three months of the pandemic enrolled in forbearance. Although minority mortgage borrowers were much more likely to experience distress and miss mortgage payments, conditional on missing payments, forbearance uptake was similar across racial and ethnic lines.

- Low interest rates led to a wave of refinancing, but fewer Black borrowers benefited from refinancing than white borrowers.

- The share of renters behind on rental payments has been above 2017 levels since 2020. Renter households who missed a rental payment were more likely to be lower-income households and were disproportionately minority households. Missed payments were most common among households who were struggling prior to the pandemic. The erratic rollout of the ERA, which was administered at the local level, prevented timely or easy access to these funds.

- Eviction moratoria resulted in a redirection of scarce household resources to immediate consumption needs and likely prevented homelessness. The decline in evictions during the pandemic is not solely the result of the eviction moratorium. The decline may also reflect the impact of ERA, greater access to legal aid, the impact of eviction diversion programs, and income replacement for households.”

Read the full chapter here.

From a new work at Brookings by Kris Gerardi, Lauren Lambie-Hanson, Paul Willen, Laurie Goodman, and Susan Wachter:

“Evidence on housing policy

- The national forbearance mandate, foreclosure moratorium, enhanced Unemployment Insurance (UI), and Economic Impact Payments (EIPs) aided in reducing financial distress for both owners and renters at the outset of the pandemic and prevented longer-run problems in mortgage and housing markets.

- Over 80 percent of borrowers who missed a mortgage payment in the first three months of the pandemic enrolled in forbearance.

Posted by at 10:16 AM

Labels: Global Housing Watch

Sunday, April 24, 2022

Health, income, and the Preston curve

From VoxEU post by Leandro Prados de la Escosura:

“GDP per capita is a commonly used, but imperfect, proxy for human wellbeing. This column analyses the relationship between life expectancy at birth and per capita income over the past 150 years. It shows that life expectancy and per capita income growth behaved differently in terms of trends and distribution over the period. The relationship was particularly weak during the period 1914 to 1950. Separately, medical improvements and the diffusion of medical knowledge have been crucial drivers of life expectancy improvements across the world.

Human wellbeing is increasingly viewed as a multidimensional phenomenon, of which income is only one facet (Stiglitz et al. 2009, OECD 2011, Proto and Rustichini 2014). However, economists continue to rely on GDP to gauge wellbeing (Oulton 2012). A way to assess GDP as a comprehensive measure of wellbeing is by looking beyond per capita income. In a recent paper, I focus on life expectancy at birth – a synthetic measure of health – and its relationship with per capita income over the past 150 years (Prados de la Escosura 2022).

An important caveat is that, when assessing life expectancy over time and across countries, we need to bear in mind that original values of life expectancy are bounded and that life quality improves with the quantity of years lived (Prados de la Escosura 2021). A solution is provided by Kakwani’s (1993) non-linear transformation in which an increase in life expectancy at birth at a higher level implies a greater achievement than would have been the case had it occurred at a lower level.

Trends in life expectancy and per capita income

Life expectancy (expressed as a Kakwani index) exhibits slightly faster long-run growth than per capita GDP. A closer look, however, reveals an apparent development puzzle: economic growth and life expectancy gains do not match each other (Table 1). During the globalisation backlash between 1914 and 1950, real per capita GDP growth slowed down as world commodity and factor markets disintegrated, while life expectancy experienced major gains across the board. But, from 1950 onwards, life expectancy achieved, on average, smaller gains to GDP per head. Thus, world average life expectancy exhibited a major advance across the board before 1950, earlier than usually presumed and at odds with the view that that global health only improved after WWII, when new drugs from the West reached the rest of the world (Acemoglu and Johnson 2007, Klasing and Milionis 2020).”

Continue reading here.

From VoxEU post by Leandro Prados de la Escosura:

“GDP per capita is a commonly used, but imperfect, proxy for human wellbeing. This column analyses the relationship between life expectancy at birth and per capita income over the past 150 years. It shows that life expectancy and per capita income growth behaved differently in terms of trends and distribution over the period. The relationship was particularly weak during the period 1914 to 1950.

Posted by at 7:58 AM

Labels: Macro Demystified

18 spectacularly wrong predictions were made around the time of the first Earth Day in 1970, expect more this year

From Mark Perry (AEI):

“Tomorrow is Earth Day 2022 and marks the 52nd anniversary of Earth Day, so it’s time for my annual CD post on the spectacularly wrong predictions that were made around the time of the first Earth Day in 1970…..

In the May 2000 issue of Reason Magazine, award-winning science correspondent Ronald Bailey wrote an excellent article titled “Earth Day, Then and Now: The planet’s future has never looked better. Here’s why” to provide some historical perspective on the 30th anniversary of Earth Day. In that article, Bailey noted that around the time of the first Earth Day in 1970, and in the years following, there was a “torrent of apocalyptic predictions” and many of those predictions were featured in his Reason article. Well, it’s now the 51st anniversary of Earth Day, and a good time to ask the question again that Bailey asked 21 years ago: How accurate were the predictions made around the time of the first Earth Day in 1970? The answer: “The prophets of doom were not simply wrong, but spectacularly wrong,” according to Bailey. Here are 18 examples of the spectacularly wrong predictions made around 1970 when the “green holy day” (aka Earth Day) started:

1. Harvard biologist George Wald estimated that “civilization will end within 15 or 30 years [by 1985 or 2000] unless immediate action is taken against problems facing mankind.”

2. “We are in an environmental crisis that threatens the survival of this nation, and of the world as a suitable place of human habitation,” wrote Washington University biologist Barry Commoner in the Earth Day issue of the scholarly journal Environment.

3. The day after the first Earth Day, the New York Times editorial page warned, “Man must stop pollution and conserve his resources, not merely to enhance existence but to save the race from intolerable deterioration and possible extinction.”

4. “Population will inevitably and completely outstrip whatever small increases in food supplies we make,” Paul Ehrlich confidently declared in the April 1970 issue of Mademoiselle. “The death rate will increase until at least 100-200 million people per year will be starving to death during the next ten years [by 1980].”

5. “Most of the people who are going to die in the greatest cataclysm in the history of man have already been born,” wrote Paul Ehrlich in a 1969 essay titled “Eco-Catastrophe! “By…[1975] some experts feel that food shortages will have escalated the present level of world hunger and starvation into famines of unbelievable proportions. Other experts, more optimistic, think the ultimate food-population collision will not occur until the decade of the 1980s.”

Continue reading here.

From Mark Perry (AEI):

“Tomorrow is Earth Day 2022 and marks the 52nd anniversary of Earth Day, so it’s time for my annual CD post on the spectacularly wrong predictions that were made around the time of the first Earth Day in 1970…..

In the May 2000 issue of Reason Magazine, award-winning science correspondent Ronald Bailey wrote an excellent article titled “Earth Day,

Posted by at 7:56 AM

Labels: Energy & Climate Change, Forecasting Forum

Friday, April 22, 2022

Housing View – April 22, 2022

On cross-country:

- These Are the World’s Most Affordable and Least Affordable Cities to Buy a Home – Bloomberg

- We Need Public Housing, Not Affordable Housing. Homeownership is out of reach for millions in Canada and the US. One well-meaning response to this crisis has been to call for more affordable housing. But we should be demanding more social housing instead. – Jacobin

On the US:

- Inflation, Interest and the Housing Paradox – New York Times

- Are We Approaching Bubble Territory in the U.S. Real Estate Market? – Realtor

- US homebuilders say materials are getting easier to find – Quartz

- The case for granny flats. Adding density would boost housing supply and lower emissions – The Economist

- Demographics, COVID-19 Leave Construction with Tight Labor Supply – St. Louis Fed

- Changing Minds on Restrictive Zoning: How to Unclog America’s Home Supply – Manhattan Institute

- Concentration in Homebuilding Driven by a Few Large Builders – Harvard Joint Center for Housing Studies

- High Building Materials Prices Erode Preference for New Construction – NAHB

- What’s Ahead for Cities & Real Estate – Wall Street Journal

- Are Some Homebuyers Strategically Transferring Climate Risks to Lenders? – Richmond Fed

- Property taxes lagged in 2021 — even as real estate prices soared – Axios

- The Sky-High Pandemic Housing Market Finds Gravity Does Exist. Mortgage costs have jumped as the Federal Reserve has raised rates. With higher rates come fewer offers – New York Times

- Decade-High Mortgage Rates Pose Threat to Spring Housing Market. Demand remains strong, but borrowing rates are climbing at fastest pace in years – Wall Street Journal

- Housing Market Fever Starts to Break in Boise – Bloomberg

- Homeowner Groups Seek to Stop Investors From Buying Houses to Rent. Suburban neighborhoods are rewriting rules as rental investors’ purchases surge – Wall Street Journal

- Home Costs and Rents Are Soaring. When Buying Makes Sense – Barron’s

- Higher Rates Start to Cool Canada’s Hot Housing Market. Transactions fall 5.4%, their biggest drop in nine months. Benchmark prices up 27% year-over-year on shortage of homes – Bloomberg

On other countries:

- [Australia] Australia’s COVID-19 pandemic housing policy responses – AHURI

- [Canada] Canada Wants to Double Home Construction But Needs to Find Workers – Canada

- [Germany] Constraints on bank lending unlikely to halt upward residential price spiral – REFIRE

- [Greece] Housing markets, the great crisis, and metropolitan gradients: Insights from Greece, 2000–2014 – IDEAS

- [United Kingdom] House prices to fall? Definitely, but not quite yet. While values are high, real interest rates are negative, making homes surprisingly affordable – FT

On cross-country:

- These Are the World’s Most Affordable and Least Affordable Cities to Buy a Home – Bloomberg

- We Need Public Housing, Not Affordable Housing. Homeownership is out of reach for millions in Canada and the US. One well-meaning response to this crisis has been to call for more affordable housing. But we should be demanding more social housing instead. – Jacobin

On the US:

- Inflation,

Posted by at 5:00 AM

Labels: Global Housing Watch

Wednesday, April 20, 2022

Figuring out efficient unemployment

From a VoxEU post by Pascal Michaillat and Emmanuel Saez:

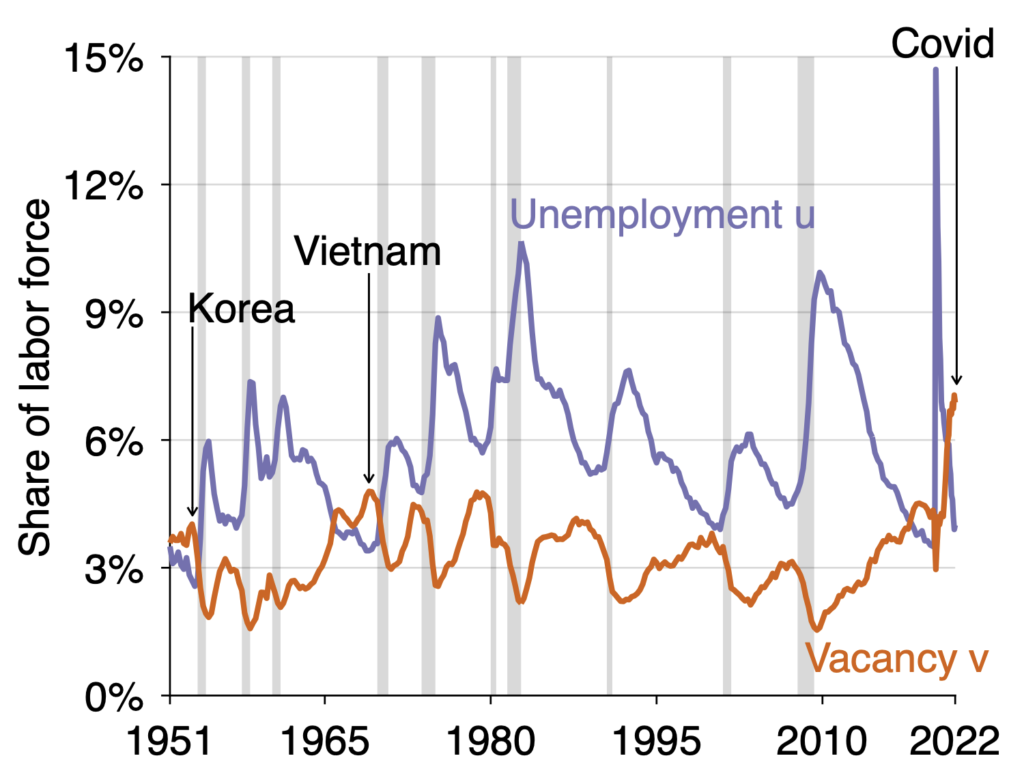

“Empirically, the unemployment rate is inversely related to the vacancy rate. Furthermore, servicing a job opening costs about as much as one job in terms of resources. This column shows that the labour market minimises waste when the unemployment rate equals the vacancy rate. It is too slack when the unemployment rate is higher and too tight when it is lower. Consequently, the efficient unemployment rate is simply given by the geometric average of the current unemployment and vacancy rates. At the beginning of 2022, the US labour market is excessively tight, and tighter than at any point since 1951.

Knowing whether an economy is too slack or at risk of overheating is crucial for macroeconomic policy. Economists generally look at price inflation, GDP level relative to potential, and the unemployment rate to assess, this but each measure has issues as can be seen when looking at the current US economy coming out of the Covid-19 crisis.1 An increase in inflation, as experienced in 2021, can be a marker of an overheating economy, but inflation can also increase due to temporary disruptions such as supply chain issues. Assessing whether GDP is below or above potential is challenging as a crisis like Covid-19 also affects the productive potential of the economy. The unemployment rate is 3.6% as of March 2022, not yet lower than just before Covid-19 when the economy did not show signs of overheating.

In this column, we propose a very simple rule to assess whether the economy, or more precisely the labour market, is too tight or too slack: are there more job openings than there are unemployed workers? This simple rule has intuitive appeal. If somehow job seekers were to be matched to job openings, would there be excess job openings, suggesting an economy with a shortage of willing workers (i.e. an overly tight labour market), or would there be excess job seekers left, suggesting an economy with too few jobs (i.e. an overly slack labour market)? It turns out that this simple intuitive rule can also be justified using the modern matching model that economists use.2 This reconciles economic theory with the widely scrutinised job-seeker-per-job-opening statistic.3

The Beveridge curve

William Beveridge first noted in 1944 that the number of job openings and the number of job seekers in the UK move in opposite directions: When the economy is depressed, there are lots of job seekers and few job openings. Conversely, when the economy is booming, there are few job seekers and many job openings. This relationship has therefore been dubbed the ‘Beveridge curve’ and holds remarkably well in the US as well.4 Figure 1 depicts the time series of the unemployment rate u (all job seekers divided by the labour force which includes all workers and job seekers) and the vacancy rate v (all job openings divided by the same labour force) since 1951. The figure shows clearly that u and v move in opposite directions.”

Figure 1 The US unemployment and vacancy rates since 1951

Continue reading here.

From a VoxEU post by Pascal Michaillat and Emmanuel Saez:

“Empirically, the unemployment rate is inversely related to the vacancy rate. Furthermore, servicing a job opening costs about as much as one job in terms of resources. This column shows that the labour market minimises waste when the unemployment rate equals the vacancy rate. It is too slack when the unemployment rate is higher and too tight when it is lower.

Posted by at 11:28 AM

Labels: Macro Demystified

Subscribe to: Posts