Wednesday, March 23, 2022

Will COVID-19 Have Long-Lasting Effects on Inequality? Evidence from Past Pandemics

From a new paper by Davide Furceri, Prakash Loungani, Jonathan D. Ostry, and Pietro Pizzuto:

“This paper provides evidence on the impact of major epidemics from the past two decades on income distribution. The pandemics in our sample, even though much smaller in scale than COVID-19, have led to increases in the Gini coefficient, raised the income share of higher income deciles, and lowered the employment-to-population ratio for those with basic education compared to those with higher education. We provide some evidence that the distributional consequences from the current pandemic may be larger than those flowing from the historical pandemics in our sample, and larger than those following typical recessions and financial crises.”

From a new paper by Davide Furceri, Prakash Loungani, Jonathan D. Ostry, and Pietro Pizzuto:

“This paper provides evidence on the impact of major epidemics from the past two decades on income distribution. The pandemics in our sample, even though much smaller in scale than COVID-19, have led to increases in the Gini coefficient, raised the income share of higher income deciles, and lowered the employment-to-population ratio for those with basic education compared to those with higher education.

Posted by at 12:24 PM

Labels: Inclusive Growth

Ukraine’s economic future

From Noahpinion:

“Some people are going to see this post as premature. Though the Ukrainians have turned the tide against the Russian invaders, the outcome is still in doubt, and much destruction still lies in the future. But at this point it seems likely that a country called Ukraine will survive this conflict, with most or all of the territory it possessed before Putin invaded. So it’s time to start thinking about reconstruction and growth after the war’s end.

Certainly after the shooting stops, the first order of business — and the task of several years — will be to rebuild the parts of the country torn down by Putin’s assault. Cities like Mariupol and Kharkiv are being reduced to rubble, much of the country’s infrastructure is being torn up, and about a quarter of the entire population has been displaced. It took Japan and Germany both slightly over a decade after the end of WW2 to reach the level of income they had enjoyed before the war. Ukraine hopefully won’t be in quite such bad shape after this conflict, but this isn’t going to be the kind of thing a country bounces back from in 1 or 2 years.

Ukrainians will work very hard to rebuild their country, but they’re going to need help. And given the U.S. and Europe’s copious military assistance, it seems likely that they’ll offer rebuilding assistance as well. In fact, the EU has just started setting up a postwar reconstruction fund, and the U.S. has already spent $13 billion helping the Ukrainians. Both the U.S. and EU leadership know that they can’t afford to have a weak, economically backward Ukraine as the first line of defense against a newly malevolent Russia, and the Ukrainians’ cause has resonated deeply with the U.S. and EU populations alike. So expect copious economic aid to flow for at least a decade.

But aid alone doesn’t build a country into an economic powerhouse. We Americans tend to think that the Marshall Plan was how Germany rebuilt its economy after WW2, but in fact this only provided a small initial kick — most of West Germany’s economic rise in the mid and late 20th century happened via its own investment and industrialization, helped by favorable trade treaties with allied countries. Ditto for Japan.

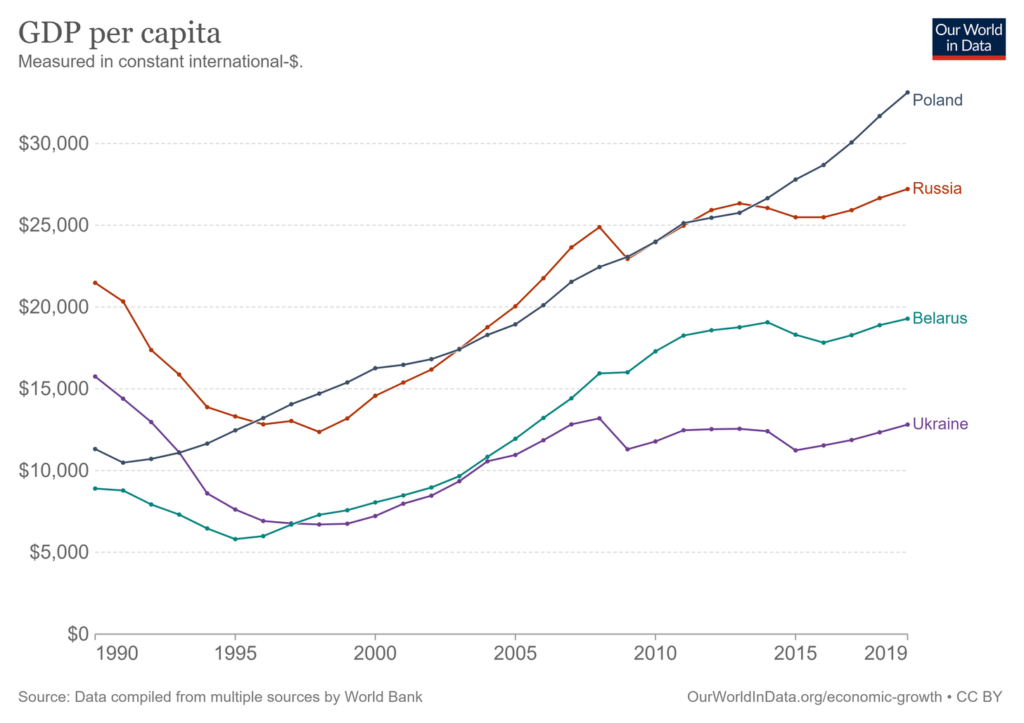

And Ukraine really needs to build itself into an economic powerhouse. Russia has four times Ukraine’s population; having a higher GDP than a sanctions-stricken postwar Russia would help Ukraine even up the balance of power a bit. Remember that before the war, Ukraine’s economy had languished for three decades, with living standards well below those of Poland, Russia, or even Belarus:”

Continue reading here.

From Noahpinion:

“Some people are going to see this post as premature. Though the Ukrainians have turned the tide against the Russian invaders, the outcome is still in doubt, and much destruction still lies in the future. But at this point it seems likely that a country called Ukraine will survive this conflict, with most or all of the territory it possessed before Putin invaded. So it’s time to start thinking about reconstruction and growth after the war’s end.

Posted by at 6:30 AM

Labels: Macro Demystified

Monday, March 21, 2022

Housing Market in Israel

From the IMF’s latest report on Israel:

“Furthermore, the reversal of several measures was needed to address emerging risks in the housing market. The rapid rise in housing prices—due to limited supply and rapid mortgage growth—rekindled concerns of price misalignment. With the house price-to-income and price-to-rent ratios at high levels, the BoI has appropriately reversed the increase in the LTV limit and the relaxation of an additional Tier 1 capital requirement for housing loans. Further tightening of macroprudential measures—e.g., lowering the debt-service-to-income cap from its current 50 percent ratio—could help stem banks’ exposures to the housing market and prevent potentially unsustainable borrowing.”

Addressing housing affordability should be high priority for the government. Given strong population growth and little growth in housing starts since 2019, investment in housing needs to accelerate significantly to curtail the existing housing shortage. In October, the government announced a plan for construction of 280,000 homes and approval of 500,000 homes in 2022–25. In December, to discourage investors in favor of first-time residence buyers, parliament increased the residential purchase tax on investors from 5 to 8 percent for the next 3 years. Further structural measures to ease housing supply—reforming property taxes, increasing land auctions, streamlining building regulations, allowing fast-track approvals of mixed-use development—should also be advanced.

(…)

Authorities’ views. The authorities agreed that banks’ strong balance sheets and macroprudential easing allowed the financial system to support the economy during the pandemic. The authorities insisted that supply-side bottlenecks in the housing market need to be addressed and were less concerned about banks’ exposures to housing market risks due to conservative LTV ratios and capital buffers. They noted that the committee reviewing the financial supervision structure was just commencing its work. Nonetheless, some committee members indicated a preference for retaining the current bank supervision architecture under the central bank given the experience of effective financial stability coordination during the pandemic.

(…)

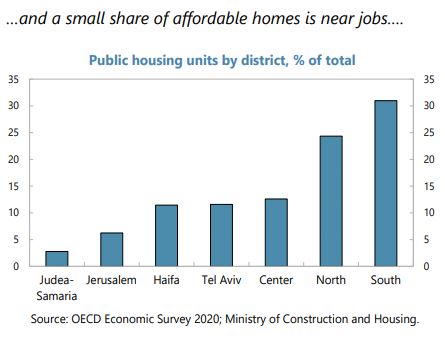

Improving the supply of affordable housing. Promoting public housing closer to economic centers, targeted to disadvantaged groups (e.g., using the mixed neighborhood models of the UK and US) would allow low-income workers better proximity to available jobs. This would require addressing the existing severe housing supply shortages. The government’s 2022–25 plan to increase the stock of available housing, which envisages additional 1.2 percent of GDP in spending, is a step in the right direction. It includes support for new schools, sewage, and other related infrastructure. However, strengthening municipal incentives to issue permits for residential housing also requires tax and land reforms, and potentially, a municipal reform. Less costly options to provide affordable housing farther away from economic centers carry trade-offs with the cost of better transport and digital infrastructure to ensure physical and digital accessibility to the available jobs.”

From the IMF’s latest report on Israel:

“Furthermore, the reversal of several measures was needed to address emerging risks in the housing market. The rapid rise in housing prices—due to limited supply and rapid mortgage growth—rekindled concerns of price misalignment. With the house price-to-income and price-to-rent ratios at high levels, the BoI has appropriately reversed the increase in the LTV limit and the relaxation of an additional Tier 1 capital requirement for housing loans.

Posted by at 2:35 PM

Labels: Global Housing Watch

Sunday, March 20, 2022

An assessment of US labor market rigidity

Source: VoxEU CEPR

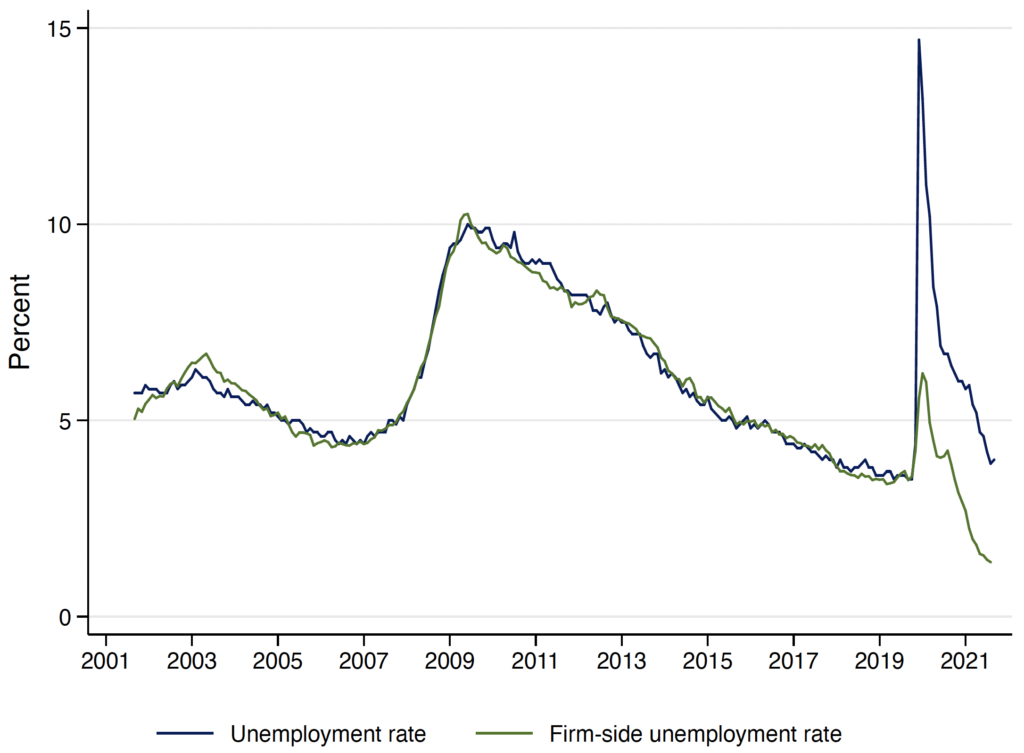

Abstract: Since the beginning of the pandemic, labour market indicators have been sending different signals about the degree of slack in the US labour market. This column uses time-series and cross-section data to show that firm-side unemployment (figure underneath) – a measure that ties together the unemployment rate with the vacancy and quits rate – predicts wage inflation better than the unemployment rate or the employment ratio, and that firm-side unemployment currently experienced in the US corresponds to a degree of tightness previously associated with sub 2% unemployment. The findings suggest that labour markets in the US are extremely tight and will likely contribute to inflationary pressures for some time to come.

Figure: Actual unemployment rate versus firm-side estimated unemployment rate

Source: VoxEU CEPR

Abstract: Since the beginning of the pandemic, labour market indicators have been sending different signals about the degree of slack in the US labour market. This column uses time-series and cross-section data to show that firm-side unemployment (figure underneath) – a measure that ties together the unemployment rate with the vacancy and quits rate – predicts wage inflation better than the unemployment rate or the employment ratio,

Posted by at 10:58 AM

Labels: Inclusive Growth

Subscribe to: Posts