Monday, March 21, 2022

Housing Market in Israel

From the IMF’s latest report on Israel:

“Furthermore, the reversal of several measures was needed to address emerging risks in the housing market. The rapid rise in housing prices—due to limited supply and rapid mortgage growth—rekindled concerns of price misalignment. With the house price-to-income and price-to-rent ratios at high levels, the BoI has appropriately reversed the increase in the LTV limit and the relaxation of an additional Tier 1 capital requirement for housing loans. Further tightening of macroprudential measures—e.g., lowering the debt-service-to-income cap from its current 50 percent ratio—could help stem banks’ exposures to the housing market and prevent potentially unsustainable borrowing.”

Addressing housing affordability should be high priority for the government. Given strong population growth and little growth in housing starts since 2019, investment in housing needs to accelerate significantly to curtail the existing housing shortage. In October, the government announced a plan for construction of 280,000 homes and approval of 500,000 homes in 2022–25. In December, to discourage investors in favor of first-time residence buyers, parliament increased the residential purchase tax on investors from 5 to 8 percent for the next 3 years. Further structural measures to ease housing supply—reforming property taxes, increasing land auctions, streamlining building regulations, allowing fast-track approvals of mixed-use development—should also be advanced.

(…)

Authorities’ views. The authorities agreed that banks’ strong balance sheets and macroprudential easing allowed the financial system to support the economy during the pandemic. The authorities insisted that supply-side bottlenecks in the housing market need to be addressed and were less concerned about banks’ exposures to housing market risks due to conservative LTV ratios and capital buffers. They noted that the committee reviewing the financial supervision structure was just commencing its work. Nonetheless, some committee members indicated a preference for retaining the current bank supervision architecture under the central bank given the experience of effective financial stability coordination during the pandemic.

(…)

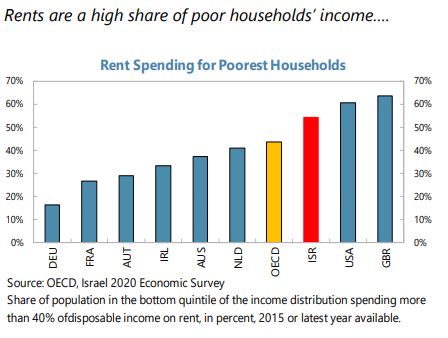

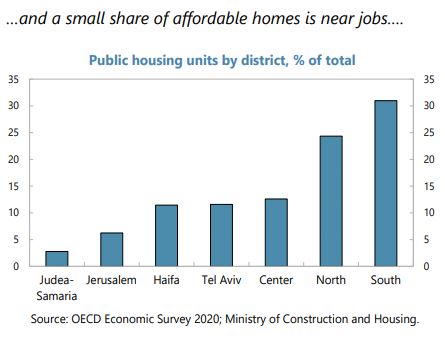

Improving the supply of affordable housing. Promoting public housing closer to economic centers, targeted to disadvantaged groups (e.g., using the mixed neighborhood models of the UK and US) would allow low-income workers better proximity to available jobs. This would require addressing the existing severe housing supply shortages. The government’s 2022–25 plan to increase the stock of available housing, which envisages additional 1.2 percent of GDP in spending, is a step in the right direction. It includes support for new schools, sewage, and other related infrastructure. However, strengthening municipal incentives to issue permits for residential housing also requires tax and land reforms, and potentially, a municipal reform. Less costly options to provide affordable housing farther away from economic centers carry trade-offs with the cost of better transport and digital infrastructure to ensure physical and digital accessibility to the available jobs.”

Posted by at 2:35 PM

Labels: Global Housing Watch

Subscribe to: Posts