Monday, January 31, 2022

Housing Market in Finland

From the IMF’s latest report on Finland:

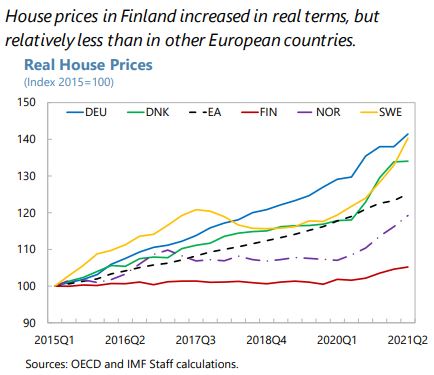

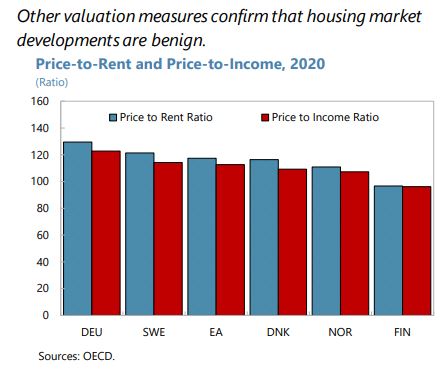

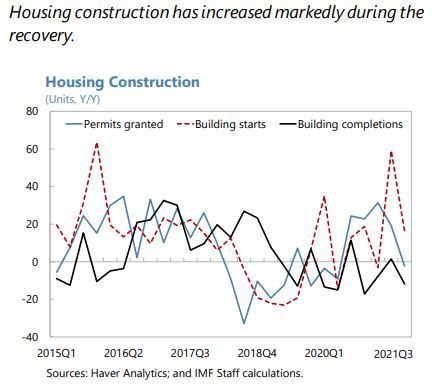

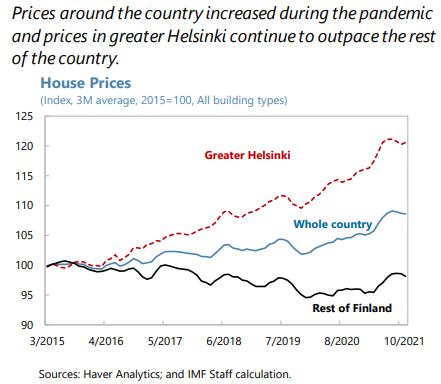

“The increase and changing composition of household debt continues to pose borrower-side vulnerabilities. Pre-pandemic, real estate prices were not overvalued, but household debt was increasing (although still low relative to Nordic peers). Much of this new debt was in the form of housing company loans—loans that finance buying shares of a housing company that may be connected to a specific apartment instead of purchasing it directly—which mask risk exposures for households. Unsecured consumer credit was also on the rise. As the pandemic struck, the authorities relaxed loan-to-collateral (LTC) requirements for housing loans. This was accompanied by an increase in highly leveraged borrowing, and housing valuations rose throughout Finland. Housing price growth has begun to moderate somewhat in the second half of 2021.

(…)

The authorities are taking steps to mitigate vulnerabilities in household finances. Following the recent increase in highly leveraged mortgage borrowing, the authorities tightened the LTC limit to pre-pandemic levels. Parliament will discuss in the spring of 2022 a draft bill on borrower-based macroprudential tools including maturity limits for housing and housing company loans, and loan-to-value (LTV) limits for housing company loans (a debt-to-income (DTI) cap was removed from the draft bill due to strong industry and political opposition). Additionally, an electronic registry of housing company shares should be operational by end-2022, making it easier to assess risks of investing in housing companies. But implementation of the planned comprehensive credit registry has been delayed to 2024 due to technical constraints.

Staff recommend that more steps be taken to enhance the macroprudential toolkit and strengthen macrofinancial resilience. The macroprudential toolkit could be enhanced further to include: (i) a DTI cap in line with recommendations from the government-appointed working group and reflecting growing household debt vulnerabilities; and (ii) supplementing the DTI cap with a debt-service-to-income cap once the new comprehensive credit registry is operational. Features of the tax code that create incentives for investors to favor housing company loans should be addressed so as to mitigate compositional changes in household debt (the recent MOF review concluded that separating the treatment of housing company shareholders’ loans’ amortization costs from interest and other expenses could help balance incentives). In this context, data relating to consumer credit and housing companies should be improved.”

Posted by at 12:16 PM

Labels: Global Housing Watch

Subscribe to: Posts