The Issue:

Reducing poverty in developing countries has been a longstanding and central concern of development economics. Over the past two decades, there has been a noticeable shift in the approach taken by development economists to address this question. Researchers have increasingly focused their efforts on randomized controlled trials — an experimental approach commonly used in medical research — to determine the effectiveness of anti-poverty programs and interventions. This shift was highlighted by the 2019 Nobel Prize in Economics awarded to Abhijit Banerjee, Esther Duflo and Michael Kremer, which recognized their work for breaking down the issue of fighting global poverty into “smaller, more manageable, questions – for example, the most effective interventions for improving educational outcomes or child health.” One question that remains, though, is how much overall reduction in the poverty rate one can expect from projects, programs or policy interventions that raise the well-being of those in absolute poverty at a given level of income, versus how much poverty reduction comes from broad-based economic growth.

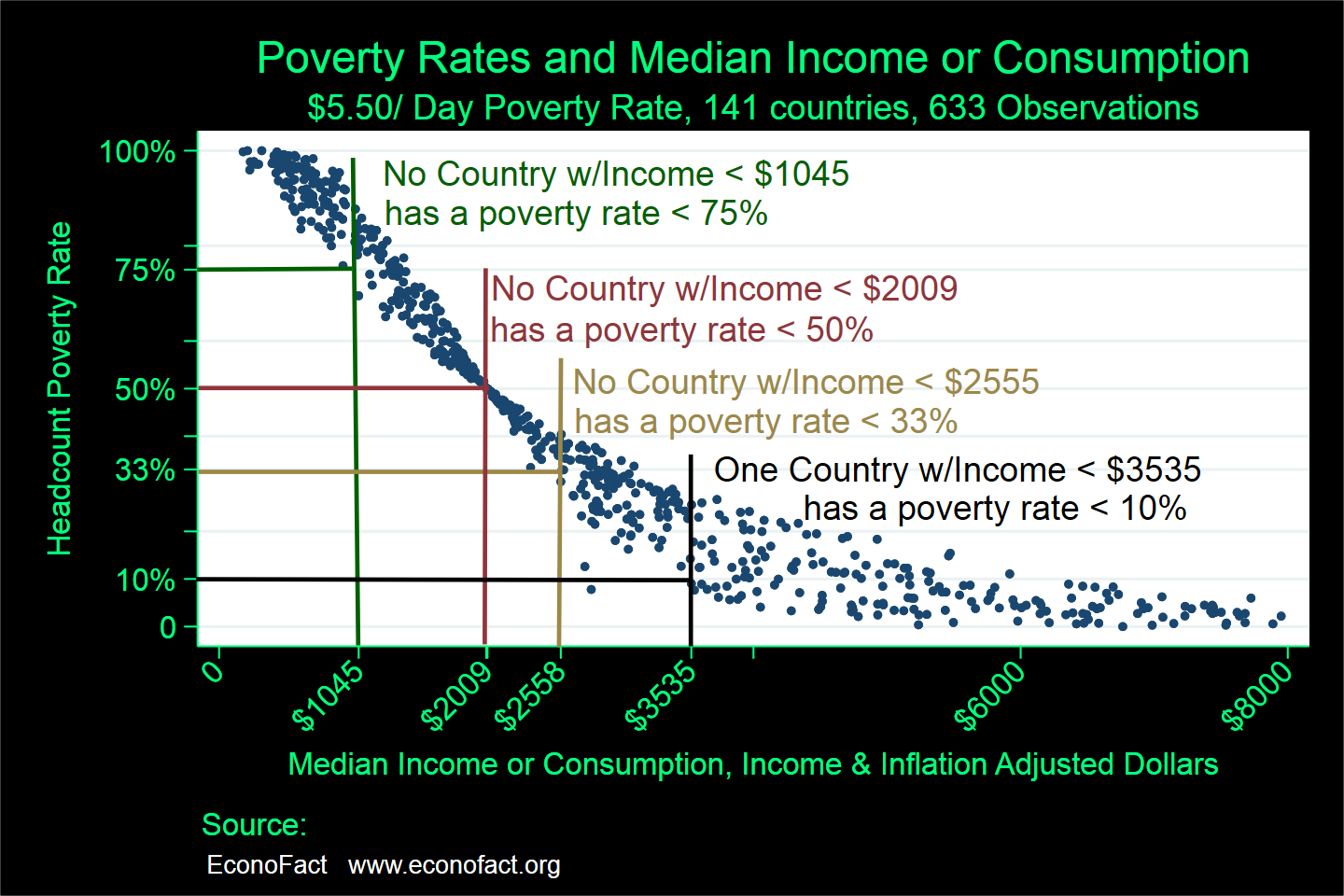

The Facts:

- In the last quarter century 1.1 billion people, about one-seventh of the world’s population, have been lifted out of extreme poverty. Yet progress has been uneven across different regions and significant challenges remain. A dramatic reduction of extreme poverty in East Asia, particularly in China, accounts for an important share of the advances in combating global poverty, with poverty reductions in South Asia also contributing their share. In contrast, progress has been much slower in Sub-Saharan Africa (see here). The World Bank counts all persons in a household as “poor” if the household per capita daily consumption or income is below a “poverty line.” It uses three different thresholds, $1.90, $3.20, and $5.50 per person per day, where local currency values are translated into 2011 dollar values, and taking into account the fact that goods and services are cheaper in poorer countries (so-called “purchasing power parity” currency conversion rates). The World Bank notes a marked reduction in extreme poverty (less than $1.90 per day) over the past quarter century, with a decrease from 36 percent in 1990 to 10 percent in 2015. Still, over 700 million people around the world continued to live in extreme poverty in 2015.

- One way to consider the relationship between economic growth and poverty is to look across countries and compare median incomes and the share of the population living in poverty. The median income is the income level at which half the population has an income higher than this amount and half the population has an income below this amount. Statisticians focus on median income rather than average income because a small number of people with very high levels of income alter the average much more than the median and can give rise to a distorted picture of the income profile of a country.