Friday, February 7, 2020

Philippines: Is Real Estate Credit a Concern?

From the IMF’s latest report on the Philippines:

“The near-boom credit episodes detected between 2014 and early 2018 coincided with strong lending growth in the real estate sector. The latter contributed importantly to the strong overall lending growth of close to 20 percent during this period. Notwithstanding some moderation recently, credit to real estate has continued to outpace that in manufacturing and other sectors. It now accounts for the largest share in total loans outstanding (18 percent).

Strong property demand from a few key players drove the real estate credit growth. The recent rise of Chinese online gaming companies operating in the Philippines (Philippines Offshore Gaming Operators—POGO) has led to a large inflow of Chinese workers and increased demand for residential and office properties. The dynamic business process outsourcing (BPO) industry has been another important driver of property demand, while demand for residential housing has also remained strong. Property prices have risen in this environment, translating into higher credit needs for many buyers.

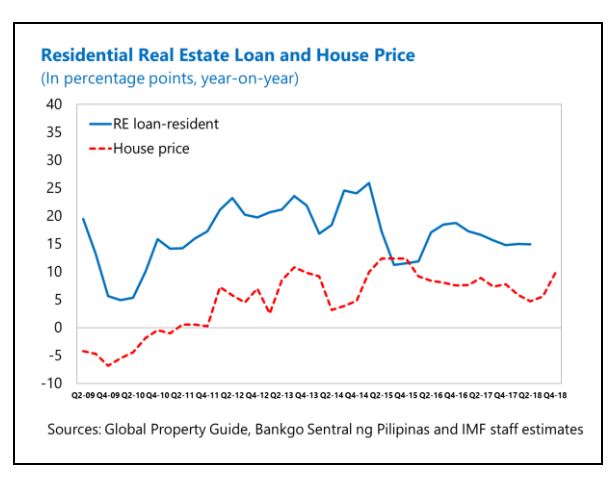

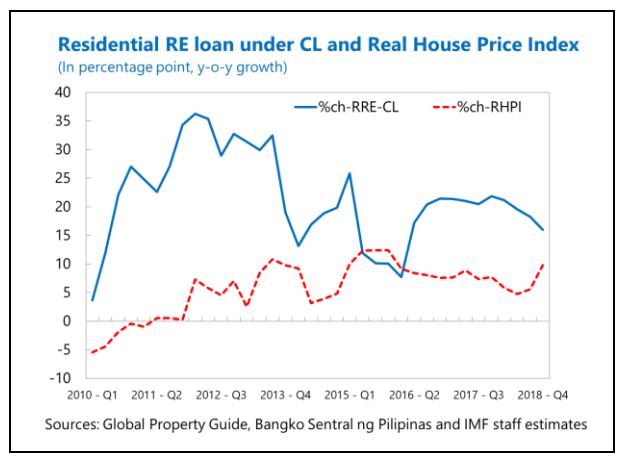

The quality of real estate loans remains sound, despite a recent uptick in NPLs. As of end-2018:Q2, NPL ratios for real estate loans were at record low levels after a steady decline. The relatively stable NPL ratio for residential loans has not followed the continuous decrease in the NPL ratio of commercial real estate loans. This could partly reflect the fact that the 20 percent limit on the share of total bank loans to commercial real estate is binding, which could be keeping bank lending focused on high-quality projects.

Continued strong real house price increases amid the cooling in residential real estate lending suggests a need for close monitoring of related market risks. House price increases in 2018 were broadly similar to those in 2017 despite the slowdown in real estate credit growth. The latter could have partly reflected the tighter lending requirements to the real estate sector in effect since mid-2018.3 Meanwhile, the increase in real house prices could be associated with high real estate demand from POGO companies and workers, which typically does not involve credit from the domestic banking system, or, possibly, increased shadow-banking activities by real estate developers, with increased indirect exposure by domestic banks.

BSP has introduced several macroprudential measures to identify and prevent the buildup of financial stability risks. These include Basel III Liquidity and Net Stable Funding Ratios, and a countercyclical capital buffer (CCyB), which has not yet been activated, as well as the Real Estate Stress Test (REST), real estate sectoral exposure limits, and mortgage collateral value limits. The Philippines’ Macroprudential Policy Measures (Box 2) discusses in greater detail the prudential measures introduced by the BSP since 2007, including newly-introduced measures on the real estate sector credit.”

Posted by at 12:50 PM

Labels: Global Housing Watch

Subscribe to: Posts