Wednesday, February 12, 2020

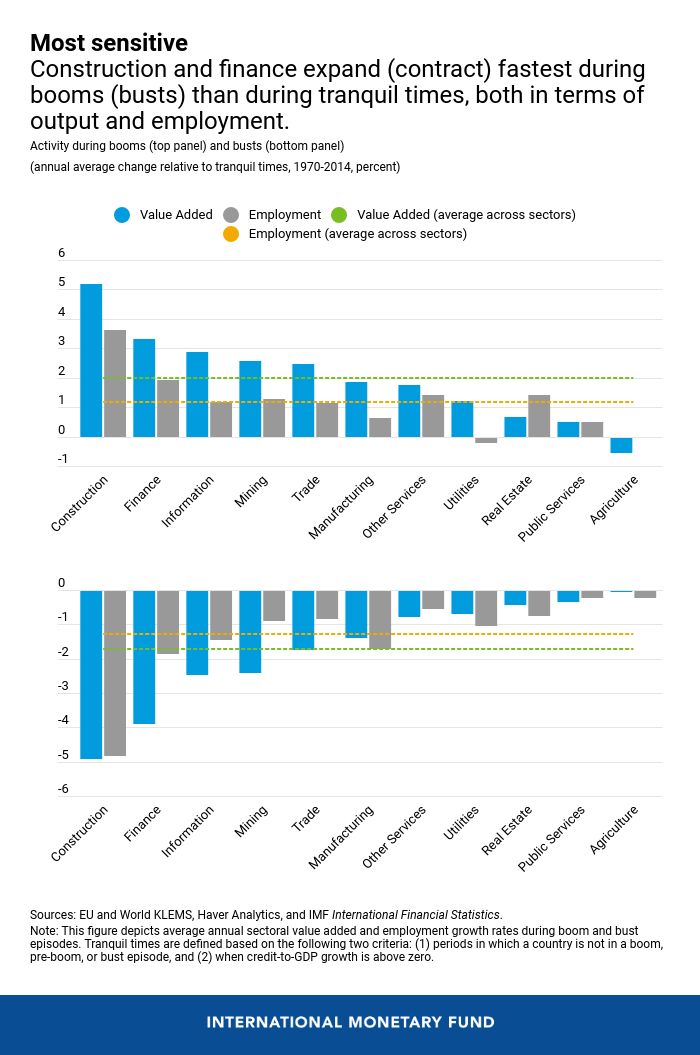

Construction Activity Can Signal When Credit Booms Go Wrong

From a new IMF research paper by Giovanni Dell’Ariccia, Ehsan Ebrahimy, Deniz O Igan, and Damien Puy:

“In Spain, private sector credit as a share of GDP almost doubled between 2000 and 2007. This increase was accompanied by a boom in housing prices—which doubled in real terms over the same period. The economy as a whole also grew at a record pace.

But then in 2008, Spain’s credit bubble burst, and with it came loan defaults, bank failures, and a prolonged economic slowdown.

A less-noticed development in Spain was in the construction sector, where employment grew by an astounding 47 percent, compared to the economy-wide increase of 27 percent.

New IMF staff research, based on a large sample of advanced and emerging market economies since the 1970s, shows that long-lasting credit booms that featured rapid construction growth never ended well.

New evidence on credit booms

Rapid credit growth—known as “credit booms”—presents a trade-off between immediate, buoyant economic performance and the danger of a future crisis. The risk of a “bad boom”—where a rapid credit growth episode is followed by a financial crisis or subpar economic growth—increases when there is also a boom in house prices.

Our research shows that the experience with the dangerous combination of credit booms and rapid expansion in the construction sector goes beyond the Spanish borders and extends to time periods not related to the global financial crisis.

We find that signals from construction activity may help to tell apart the dangerous booms, which need to be controlled, from the episodes of buoyant but healthy credit growth (“good booms”).

Credit booms do not lift all boats alike

During booms, output and employment expand faster. But not all sectors behave the same. Most of the extra growth is concentrated in a few industries—specifically, construction and, at a distant second, finance.

However, the same industries that benefit the most during booms experience the most severe downturns during busts. This implies that credit booms tend to leave few long-term footprints on a country’s industrial composition.”

Continue reading here.

From a new IMF research paper by Giovanni Dell’Ariccia, Ehsan Ebrahimy, Deniz O Igan, and Damien Puy:

“In Spain, private sector credit as a share of GDP almost doubled between 2000 and 2007. This increase was accompanied by a boom in housing prices—which doubled in real terms over the same period. The economy as a whole also grew at a record pace.

But then in 2008, Spain’s credit bubble burst,

Posted by at 10:49 AM

Labels: Global Housing Watch

Scottish Home Prices: Compatible with Euro Membership?

From a paper by William Miles (Wichita State University):

“Although the Scottish electorate voted down independence in 2014, Brexit has led to renewed calls from Scottish political leaders for a second referendum. Scottish independence would likely lead to joining the European Union, and this would obligate Scotland to eventually join the euro common currency. If Scottish home prices were not highly cohesive with those in euro zone countries, the ECB’s monetary policy could cause major disruptions for Scottish housing, and, by extension, the Scottish economy. As an example, if most euro-country home values were rising, but those in Scotland were falling, the ECB would likely run a tight monetary policy, which would be devastating to housing conditions in Scotland. We accordingly investigate the co-movement of house prices in Scotland with those in eight major euro zone countries, as well as co-movement between Scottish and UK home prices, using a variety of metrics. The use of methods that are primarily linear indicates that joining the euro may not result in a large loss of co-movement with other regional housing markets, compared to Scotland’s current correlation with UK national home prices. However, the use of a measure that takes into account differences in the magnitude, and not just the phase of cycles yields results indicating Scotland exhibits very little co-movement with other euro housing markets. Indeed Scotland has co-movement metrics within the euro countries at levels similar to those of Spain and Ireland, which both suffered devastating booms and busts. Thus leaving sterling for the euro could be highly problematic.”

From a paper by William Miles (Wichita State University):

“Although the Scottish electorate voted down independence in 2014, Brexit has led to renewed calls from Scottish political leaders for a second referendum. Scottish independence would likely lead to joining the European Union, and this would obligate Scotland to eventually join the euro common currency. If Scottish home prices were not highly cohesive with those in euro zone countries, the ECB’s monetary policy could cause major disruptions for Scottish housing,

Posted by at 10:45 AM

Labels: Global Housing Watch

Growth divergence and income inequality in OECD countries: the role of trade and financial openness

From a LSE paper by Enrico D’Elia and Roberta De Santis:

“This paper analyses trade and financial openness effects on growth and income inequality in 35 OECD countries. Our model takes into account both short run and long run effects of factors explaining income divergence between and within the countries. We estimate, for the period 1995-2016, an error correction model in which per capita GDP and inequality are driven by changes over time of selected factors and by the deviation from a long run relationship. Stylised facts suggest that trade and financial openness reduce the growth gaps across the countries but not income inequality, and the effects of finance are stronger in high income countries. Nevertheless, low and middle income countries benefit more from international trade. Our contribution to the existing literature is threefold: i) we study the short and long run effects of trade and financial openness on income level and distribution, ii) we focus on developed countries (OECD) rather than on developing and iii) we provide a sensitivity analysis including in our baseline equation an institutional indicator, a trade agreement proxy and a dummy of global financial crisis. Estimates results indicate that trade openness significantly improved the conditions of OECD low income countries both in short and long run mostly, consistently with the catching up theory. It also decreased inequality, but only in low and middle income countries. Differently financial openness had a positive and significant impact only in the short run on middle income countries and increased income disparities within countries in the short term in low income countries and in the long term in high income countries.”

From a LSE paper by Enrico D’Elia and Roberta De Santis:

“This paper analyses trade and financial openness effects on growth and income inequality in 35 OECD countries. Our model takes into account both short run and long run effects of factors explaining income divergence between and within the countries. We estimate, for the period 1995-2016, an error correction model in which per capita GDP and inequality are driven by changes over time of selected factors and by the deviation from a long run relationship.

Posted by at 10:44 AM

Labels: Inclusive Growth

A just transition must help those struggling to heat their homes

From Social Europe post by Monique Goyens:

“In the latest contribution to our series on ‘just transition’, Monique Goyens argues that it must address the people finding it hard to pay their energy bills.

The task of moving to a carbon-neutral society is herculean, but the benefits won’t just include saving the planet. There are also long-term economic gains, even for the most hard-up.

An estimated 50 million around the European Union struggle to keep their homes warm and pay their energy bills. Many suffer from the same problems: poorly insulated homes, ill-suited tariffs, insufficient advice on how to save energy or a combination of all three.

The lowest income earners in the EU spend an increasingly large share of their budget on energy—rising from 6 per cent in 2000 to 9 per cent in 2014. In the short term, for this group, it makes more sense to use energy more efficiently than to invest in solar panels, heat pumps or pellet stoves. It will also deliver faster savings.

The choice should not however be between having a warm home and having food on the table. In making their homes more efficient, people consume less energy to heat their living space and can more easily pay their bills.

But getting people to take action can be complex. Those at risk of energy poverty might feel overwhelmed and prioritise solving other problems, such as warmer clothing or food. Often, they might not know what solutions are out there.

For governments and energy advisers to upload advice about insulation to a website isn’t enough. That advice needs to get out to people. Human contact also helps.”

Continue reading here.

From Social Europe post by Monique Goyens:

“In the latest contribution to our series on ‘just transition’, Monique Goyens argues that it must address the people finding it hard to pay their energy bills.

The task of moving to a carbon-neutral society is herculean, but the benefits won’t just include saving the planet. There are also long-term economic gains, even for the most hard-up.

Posted by at 10:42 AM

Labels: Energy & Climate Change, Global Housing Watch, Inclusive Growth

Monday, February 10, 2020

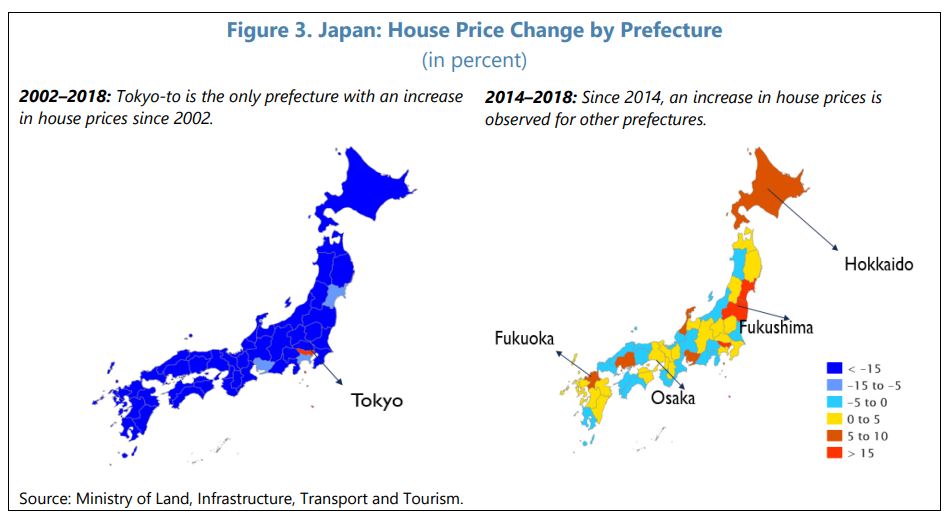

Disappearing Cities: Demographic Headwinds and their Impact on Japan’s Housing Market

From the IMF’s latest report on Japan:

“Japan’s population is rapidly aging and shrinking, and doing so unevenly across regions. Large cities, notably the Greater Tokyo area, are experiencing net migration inflows, while other regions are experiencing net migration outflows. In this chapter, we assess the regional differences in population dynamics and their implications for house price developments in Japan. Due to the durability of housing compared to other forms of investment, the magnitude of house price declines associated with population losses is larger than that of house price increases associated with population gains. These model-based predictions are likely to underestimate the actual fall in house prices associated with future population losses, as expectations of lower housing prices in the future could trigger more population outflows and disposal of houses, especially in rural areas. We suggest policy measures to help close regional disparities and avoid potential over-investment by taking account of demographic trends for housing supply.”

From the IMF’s latest report on Japan:

“Japan’s population is rapidly aging and shrinking, and doing so unevenly across regions. Large cities, notably the Greater Tokyo area, are experiencing net migration inflows, while other regions are experiencing net migration outflows. In this chapter, we assess the regional differences in population dynamics and their implications for house price developments in Japan. Due to the durability of housing compared to other forms of investment,

Posted by at 1:14 PM

Labels: Global Housing Watch

Subscribe to: Posts