Thursday, April 4, 2019

Assessing the Risk of the Next Housing Bust

From the IMF’s latest Global Financial Stability report:

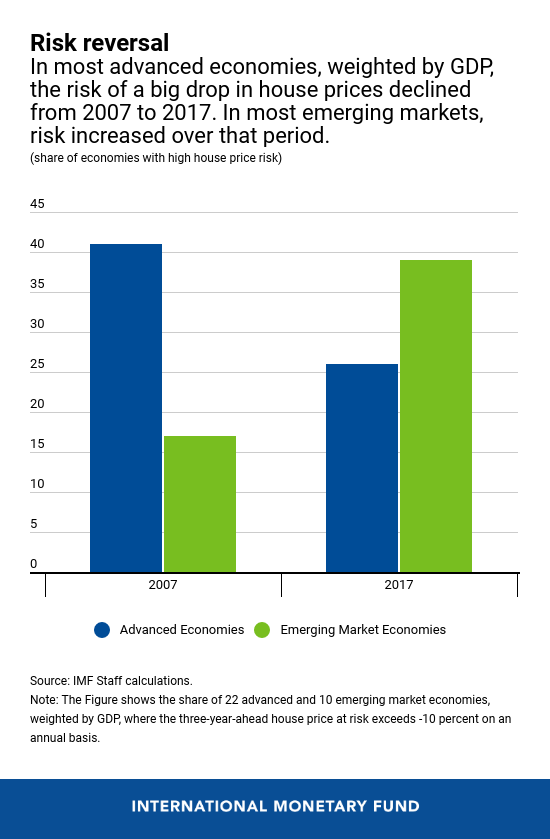

“There’s good news for people living in Las Vegas, Miami and Phoenix: the risk of a housing bust like the one they endured during the global financial crisis is fairly small. For folks in Toronto and Vancouver, however, the picture hasn’t improved since 2008, and the risk of a large decline in house prices remains elevated.

Those are among the insights generated by the IMF’s new tool for assessing the danger of a severe downturn in home prices. Homeowners, of course, are keenly interested in the value of what is probably their biggest asset. But there is also a strong link between home prices, the financial system, and the economy. The link is especially powerful when prices go down – as we explain in Chapter Two of the IMF’s twice-yearly Global Financial Stability Report.

Why do home prices matter for the broader economy? Housing construction and related spending on things like home improvements account for one-sixth of the US and euro-area economies, making them among the largest components of GDP. What’s more, mortgages and other housing-related lending are a big part of banks’ assets in many countries, so changes in house prices affect the health of the banking system.

Boom-bust cycle

It’s no surprise, then, that more than two-thirds of financial crises in recent decades were preceded by a boom-bust cycle in home prices, and that central banks in the United States, China, Australia, and elsewhere have recently expressed concern about large increases in home prices.

Fortunately, the IMF’s new tool can help policy makers gauge the likelihood of a future housing downturn and take early steps to help limit the damage. The tool, dubbed House Prices at Risk, feeds into the Fund’s growth-at-risk model, which links financial conditions to the danger of an economic downturn (see the October 2017 GFSR .)

Our study encompasses data from 22 advanced economies, 10 emerging-market economies, and the major cities in those countries. We found that in most advanced economies in our sample, weighted by GDP, the odds of a big drop in inflation-adjusted house prices were lower at the end of 2017 than 10 years earlier but remained above the historical average. In emerging markets, by contrast, riskiness was higher in 2017 than on the eve of the global financial crisis. Nonetheless, downside risks to house prices remain elevated in more than 25 percent of these advanced economies and reached nearly 40 percent in emerging markets in our study. Among them, China stands out, especially its Eastern provinces.”

Continue reading here.

From the IMF’s latest Global Financial Stability report:

“There’s good news for people living in Las Vegas, Miami and Phoenix: the risk of a housing bust like the one they endured during the global financial crisis is fairly small. For folks in Toronto and Vancouver, however, the picture hasn’t improved since 2008, and the risk of a large decline in house prices remains elevated.

Those are among the insights generated by the IMF’s new tool for assessing the danger of a severe downturn in home prices.

Posted by at 10:06 AM

Labels: Global Housing Watch

Wednesday, April 3, 2019

The missing link between income inequality and economic growth: Inequality of opportunity

From a VoxEU post by Shekhar Aiyar and Christian Ebeke:

“There are contrasting theories on the relationship between income inequality and growth, and the empirical evidence is similarly mixed. This column highlights the neglected role of equality of opportunity in mediating this relationship. Using the World Bank’s new Global Database on Intergenerational Mobility, it shows that in societies where opportunities are unequally distributed, income inequality exerts a greater drag on growth.

Despite the firm consensus that income inequality is intrinsically undesirable, its impact on economic growth is much disputed. Simon Kuznets famously argued that inequality is beneficial for economic growth at an early stage of development, since a moneyed capitalist class can undertake more investment, but is harmful at a later stage. Others have pointed to inequality as a necessary, even desirable outcome of rewards to innovation and risk-taking. But there are also numerous theories about how income inequality can reduce investment and hinder the full realisation of human potential. As a canonical example, Galor and Zeira (1993) show that if poor families are constrained to under-invest in education, aggregate growth falls.

The empirical evidence is similarly mixed. Barro (2000) finds that for developed economies income inequality raises growth. On the other hand, Berg et al. (2012, 2018) find that income inequality tends to reduce the duration of growth spells. Forbes (2000) and Panizza (2002) find no systematic effect.

The missing link: Inequality of opportunity

In recent work (Aiyar and Ebeke 2018), we point to the neglected role of equality of opportunity in mediating this relationship. Our hypothesis is simple. In societies where opportunities are unequally distributed – where the material circumstances of parents act as binding constraints on the opportunities available to their children – income inequality exerts a greater drag on growth. Any increase in income inequality tends to become entrenched, limiting the investment opportunities – broadly defined to include investment in children – available to low-income earners, thereby retarding long-term aggregate growth. On the other hand, in societies with a more equal distribution of opportunities, an increase in income inequality can be more easily reversed and need not constrain investment opportunities and growth. To the extent that inequality of opportunity matters in this way, its omission from standard regressions of growth on income inequality leads to misspecification, which can help explain the inconclusive nature of the empirical literature to date.

We measure a society’s distribution of opportunity by the economic mobility of its people across generations. The World Bank’s new Global Database on Intergenerational Mobility (GDIM) compiles cross-country estimates of the elasticity of a son’s income (or education level) with respect to the income (or education level) of their father (Narayan et al. 2018). The higher this elasticity, the lower the degree of intergenerational mobility, which we take to signal a less equal distribution of opportunity. Because each observation requires a comparison of life-cycle income over two generations, this is a slow-moving variable whose latest value says something about societal conditions over a period of several decades. For the purpose of our study and due to data availability constraints, we take this variable to be time-invariant.”

Continue reading here.

From a VoxEU post by Shekhar Aiyar and Christian Ebeke:

“There are contrasting theories on the relationship between income inequality and growth, and the empirical evidence is similarly mixed. This column highlights the neglected role of equality of opportunity in mediating this relationship. Using the World Bank’s new Global Database on Intergenerational Mobility, it shows that in societies where opportunities are unequally distributed, income inequality exerts a greater drag on growth.

Posted by at 8:43 AM

Labels: Inclusive Growth

Housing Market in Kuwait

From the IMF’s latest report on Kuwait:

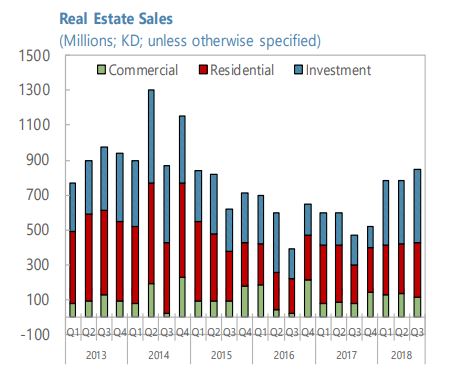

“Real estate is recovering, and equity markets have outperformed regional peers. The sales of investment and residential properties rebounded since mid-2018. Kuwaiti stocks outperformed other Gulf Cooperation Council (GCC) markets, and market capitalization rose, especially following the March 2018 announcement of Kuwait’s inclusion in the FTSE Russell Emerging Market Index.”

From the IMF’s latest report on Kuwait:

“Real estate is recovering, and equity markets have outperformed regional peers. The sales of investment and residential properties rebounded since mid-2018. Kuwaiti stocks outperformed other Gulf Cooperation Council (GCC) markets, and market capitalization rose, especially following the March 2018 announcement of Kuwait’s inclusion in the FTSE Russell Emerging Market Index.”

Posted by at 8:40 AM

Labels: Global Housing Watch

Tuesday, April 2, 2019

Monetary Policy, Growth and Employment in Developing Areas: A Review of the Literature

From a paper by P.N. (Raja) Junankar at University of Technology Sydney;

“In this paper we review the literature on the impact that monetary policy has on growth and employment in developing countries. Much of the literature focusses on the impact of monetary policy on inflation levels and inflation volatility, and sometimes on output (GDP) levels and volatility of output. This survey of the literature on Monetary policy and growth shows that money plays a small role in developing countries and that monetary policy is not a very important influence on growth but may have some impact on inflation. Although there is much discussion about the merits of keeping inflation levels and volatility low, there is very little literature on studying the impact of low rates of steady inflation on the levels of private investment and technological change and hence on economic growth and on employment. There is very little research about the direct links between monetary policy and employment. The impact of growth on employment depends on what are the main drivers of economic growth and the initial state of the economy. Although growth may lead to increasing employment (formal and informal) there is little evidence showing that growth leads to an increase in “decent employment”.”

From a paper by P.N. (Raja) Junankar at University of Technology Sydney;

“In this paper we review the literature on the impact that monetary policy has on growth and employment in developing countries. Much of the literature focusses on the impact of monetary policy on inflation levels and inflation volatility, and sometimes on output (GDP) levels and volatility of output. This survey of the literature on Monetary policy and growth shows that money plays a small role in developing countries and that monetary policy is not a very important influence on growth but may have some impact on inflation.

Posted by at 11:07 AM

Labels: Inclusive Growth

Monday, April 1, 2019

Some US Social Indicators Since 1960

From a new post by Timothy Taylor

“Economic

- Real GDP per person has more than tripled since 1960, rising from $18,036 in 1960 to $55,373 in 2017 (as measured in constant 2012 dollars).

- Inflation has reduced the buying power of the dollar over time such that $1 in 2016 had about the same buying power as 12.3 cents back in 1960, according to the Consumer Price Index.

- The employment/population ratio rose from 56.1% in 1960 to 64.4% by 2000, then dropped to 58.5% in 2012, before rebounding a bit to 62.9% in 2018.

- The share of the population receiving Social Security disabled worker benefits was 0.9% in 1960 and 5.5% in 2018.

- The net national savings rate was 10.9% of GDP in 1960, 7.1% in 1980, and 6.0% in 2000. It actually was slightly negative at -0.5 in 2010, but was back to 2.9% in 2017.

- Research and development spending has barely budged over time: it was 2.52% of GDP in 1960 and 2.78% of GDP in 2017, and hasn’t varied much in between.

Demographic

- The foreign-born population of the US was 9.6 million out of a total of 204 million in 1970, and was 44.5 million out of at total of 325.7 million in 2017.

- In 1960, 78% of the over-15 population had ever been married; in 2018, it was 67.7%.

- Average family size was 3.7 people in 1960, and 3.1 people in 2018.

- Single parent households were 4.4% of households in 1960, and 9.1% of all households in 2010, but slightly down to 8.3% of all households in 2018.

Socioeconomic

- The share of 25-34 year-olds who are high school graduates was 58.1% in 1960, 84.2% in 1980, and 90.9% in 2018.

- The share of 25-34 year-olds who are college graduates was 11% in 1960, 27.5% in 2000, and 35.6% in 2017.

- The average math achievement score for a 17 year-old on the National Assessment of Educational Progress was 304 in 1970, and 306 in 2010.

- The average reading achievement score for a 17 year-old was 285 in 1970 and 286 in 2010.

Health

- Life expectancy at birth was 69.7 years in 1960, and 78.7 years in 2010, and 78.6 years in 2017.

- Infant mortality was 26 per 1,000 births in 1960, and 5.8 per 1,000 births in 2017.

- In 1960, 13.4% of the population age 20-74 was obese (as measured by having a Body Mass Index above 30). In 2016, 40% of the population was obese.

- In 1970, 37.1% of those age 18 and older were cigarette smokers. By 2017, this has fallen to 14.1%.

- Total national health expenditures were 5.0% of GDP in 1960, and 17.9% of GDP in 2017.

Security and Safety

- The murder rate was 5.1 per 100,000 people in 1960, rose to 10.2 per 100,000 by 1980, but had fallen back to 4.9 per 100,000 in 2015, before nudging up to 5.3 per 100,000 in 2017..

- The prison incarceration rate in federal and state institutions was 118 per 100,000 in 1960, 144 per 100,000 in 1980, 519 per 100,000 by 2010, and then down to 464 per 100,000 in 2016.

- Highway fatalities rose from 37,000 in 1960 to 51,000 in 1980, and then fell to 33,000 in 2010, before nudging up to 37,000 in 2017.

Energy

- Energy consumption per capita was 250 million BTUs in 1960, rose to 350 million BTUs per person in 2000, but since then has fallen to 300 BTUs per person in 2017.

- Energy consumption per dollar of real GDP (measured in constant 2009 dollars) was 14,500 BTUs in 1960 vs. 5,700 in 2017.

- Electricity net generation on a per person basis was 4.202 kWh in 1960, had more than tripled to 13,475 kWh by 2000, but since then has declined to 12,326 kWh in 2017.

- The share of electricity generation from renewable sources was 19.7% of the total in 1960, fell to 8.8% by 2005, and since then rose to 17.1% of the total in 2017.

Numbers and comparisons like these are a substantial part of how a head-in-the-clouds academic like me perceives economic and social reality. If you like this kind of stuff, you would probably also enjoy my post from a few years back, “The Life of US Workers 100 Years Ago” (February, 5, 2016).”

From a new post by Timothy Taylor

“Economic

- Real GDP per person has more than tripled since 1960, rising from $18,036 in 1960 to $55,373 in 2017 (as measured in constant 2012 dollars).

- Inflation has reduced the buying power of the dollar over time such that $1 in 2016 had about the same buying power as 12.3 cents back in 1960, according to the Consumer Price Index.

Posted by at 2:41 PM

Labels: Inclusive Growth

Subscribe to: Posts