Tuesday, April 9, 2019

Subjective Models of the Macroeconomy: Evidence From Experts and a Representative Sample

From a new working paper:

“We propose a method to measure people’s subjective models of the macroeconomy. Using a representative sample of the US population and a sample of experts we study how expectations about the unemployment rate and the inflation rate change in response to four different hypothetical exogenous shocks: a monetary policy shock, a government spending shock, a tax shock, and an oil price shock. While expert predictions are mostly quantitatively aligned with standard dynamic stochastic general equilibrium models and vector auto-regression evidence, there is strong heterogeneity in the predictions in the representative panel. While households predict changes in unemployment that are qualitatively in line with the experts for all four shocks, their predictions of changes in inflation are at odds with those of experts both for the tax shock and the interest rate shock. People’s beliefs about the micro mechanisms through which the different macroeconomic shocks are propagated in the economy strongly affect how aligned their predictions are with those of the experts. More educated and older respondents form their expectations more in line with experts, consistent with roles for cognitive limitations and learning over the life-cycle. Our findings inform the validity of central assumptions about the expectation formation process and have important implications for the optimal design of fiscal and monetary policy.”

From a new working paper:

“We propose a method to measure people’s subjective models of the macroeconomy. Using a representative sample of the US population and a sample of experts we study how expectations about the unemployment rate and the inflation rate change in response to four different hypothetical exogenous shocks: a monetary policy shock, a government spending shock, a tax shock, and an oil price shock. While expert predictions are mostly quantitatively aligned with standard dynamic stochastic general equilibrium models and vector auto-regression evidence,

Posted by at 10:33 PM

Labels: Forecasting Forum

Measuring unemployment and labor-force participation

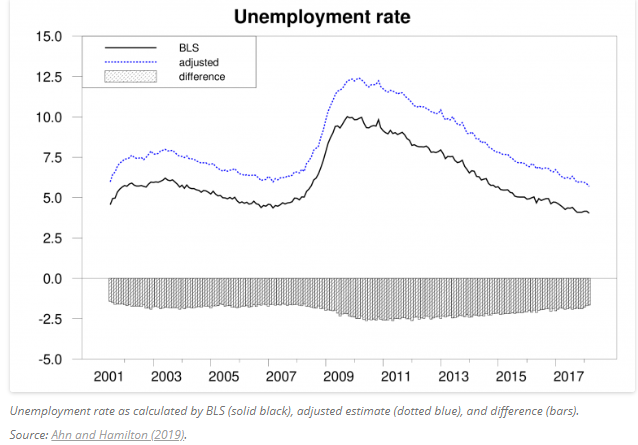

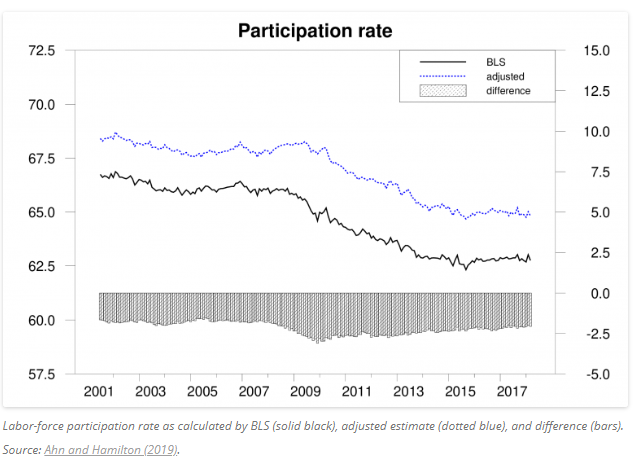

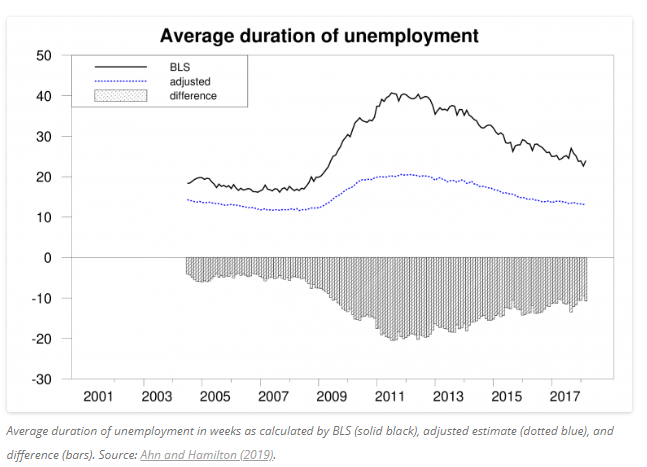

From a new Econbrowser by Hie Joo Ahn and James D. Hamilton:

“We conclude that the true unemployment rate in the U.S. is 1.9% higher on average than the published estimates.”

“We also conclude that the Bureau of Labor Statistics has underestimated the labor-force participation rate by 2.2% on average and that the fall in participation has been slower than suggested by the BLS estimates.”

“On the other hand, we find that reported average unemployment durations significantly overstate the average length of an uninterrupted spell of unemployment. A big factor in this appears to be the fact noticed by Kudlyak and Lange (2018) that some individuals include periods when they were briefly employed but nonetheless looking for a better job when they give an answer to how many weeks they have been actively looking for a job.”

“Here is our paper’s conclusion:

The data underlying the CPS contain multiple internal inconsistencies. These include the facts that people’s answers change the more times they are asked the same question, stock estimates are inconsistent with flow estimates, missing observations are not random, reported unemployment durations are inconsistent with reported labor-force histories, and people prefer to report some numbers over others. Ours is the first paper to attempt a unified reconciliation of these issues. We conclude that the U.S. unemployment rate and labor-force continuation rates are higher than conventionally reported while the average duration of unemployment is considerably lower.”

From a new Econbrowser by Hie Joo Ahn and James D. Hamilton:

“We conclude that the true unemployment rate in the U.S. is 1.9% higher on average than the published estimates.”

“We also conclude that the Bureau of Labor Statistics has underestimated the labor-force participation rate by 2.2% on average and that the fall in participation has been slower than suggested by the BLS estimates.”

Posted by at 10:28 PM

Labels: Inclusive Growth

Universal Basic Income: The Promise vs the Practicalities

From Intereconomics:

“The idea of a universal basic income (UBI) is nothing new: the concept of a guaranteed endowment paid by the government to each of its citizens dates back centuries. The UBI has gained momentum in recent years as the relative economic stability of the second half of the 20th century gave way to a more turbulent start to the new millennium. The limits of the free market and globalisation in providing a decent standard of living for every citizen were laid bare for all to see, and inequality widened in even the richest global economies. Added to this was the increasing complexity of social security systems in modern welfare states. Policymakers and civil servants had the unenviable task of deciding who was deserving of assistance, as well as policing those in the system to make sure advantage was not being taken. Proponents argue that a UBI, by simply trusting everyone with a basic income each month, could solve both of these issues. Moreover, it could also be the solution to the purportedly imminent destruction of traditional jobs due to the rise of robotics and artificial intelligence. While the idea of a UBI is intriguing, real-world implementation is anything but basic. No serious answers have been found to the question of how to finance such a system, and until a workable solution is found, a UBI is simply not feasible. Other issues that economists continue to research include the negative effects of a UBI on a person’s willingness to work and the proper size of a UBI in order to fulfil its intended purpose. The following five articles in this Forum deal with these issues in order to analyse the strengths and weaknesses of what will surely be a major topic of debate over the next decade and beyond.”

Continue reading here.

From Intereconomics:

“The idea of a universal basic income (UBI) is nothing new: the concept of a guaranteed endowment paid by the government to each of its citizens dates back centuries. The UBI has gained momentum in recent years as the relative economic stability of the second half of the 20th century gave way to a more turbulent start to the new millennium. The limits of the free market and globalisation in providing a decent standard of living for every citizen were laid bare for all to see,

Posted by at 4:06 PM

Labels: Inclusive Growth

The Power of Two: Inclusive Growth and the IMF

From Intereconomics:

“For decades, mainstream economics has focused on increasing economic growth and accelerating cross-country convergence, while ignoring distributional concerns. However, the consensus has begun to shift, and recent IMF research has paid increased attention to inclusive growth and the detrimental macroeconomic effects of inequality. The IMF also recognises the threat posed by climate change and has begun to dedicate research to exploring ways to decouple carbon emissions from economic growth.

It is common in macroeconomic models to assume the existence of a “representative agent”, one person who represents the preferences of the entire economy. By construction, such models focus on growth rather than on distribution. However, the use of models with “heterogeneous agents” is increasing, which permit a joint analysis of growth and distribution. This trend has been mirrored in the IMF’s research and operations in recent years. While growth remains critical, the institution increasingly recognises that:

- jobs are the basis for people to feel included in society and have a sense of dignity – hence the IMF’s increased focus on unemployment and the functioning of labour markets;

- major segments of the population should have the opportunity to share in the prosperity of a country – hence the research into inequality;

- growth should be shared not just among this generation but with future generations – hence the scaling up of work on addressing climate change.

A common thread through many of the IMF’s recent initiatives is that they seek to promote inclusion. Over time, these issues have become important to the institution’s mission, as they directly affect economic performance and stability in many countries. This article describes the key findings of some of the IMF’s work in these three areas.”

Continue reading here.

From Intereconomics:

“For decades, mainstream economics has focused on increasing economic growth and accelerating cross-country convergence, while ignoring distributional concerns. However, the consensus has begun to shift, and recent IMF research has paid increased attention to inclusive growth and the detrimental macroeconomic effects of inequality. The IMF also recognises the threat posed by climate change and has begun to dedicate research to exploring ways to decouple carbon emissions from economic growth.

Posted by at 4:05 PM

Labels: Inclusive Growth

Friday, April 5, 2019

Housing View – April 5, 2019

On cross-country:

- Affordable Housing Crisis Spreads Throughout World – Wall Street Journal

- Film Director: Don’t Just Blame Gentrification for Housing Crisis – Wall Street Journal

- Mind the data gap: commercial property prices for policy – Bank for International Settlements

On the US:

- Bank Balance Sheets and Liquidation Values: Evidence from Real Estate Collateral – SSRN

- Expectations During the U.S. Housing Boom: Inferring Beliefs from Actions – NBER

- Banks’ Real Estate Exposure and Resilience – Federal Reserve Bank of San Francisco

- American Families Can’t Afford the Rent – Harvard Joint Center for Housing Studies

- San Francisco Fed Says Banks Could Weather a Big Hit to Housing – Bloomberg

- The Link Between Local Zoning Policy and Housing Affordability in America’s Cities – George Mason University

- Wall Street Puts the Squeeze on the Housing Market – Bloomberg

- California Home Prices Are So High, Even High-Income Households Can’t Keep Up – Zillow

- What’s Keeping Lower-Income Families from Homeownership? – Freddie Mac

- Are Planners Partly to Blame for Gentrification? – Citylab

- Mapping America’s Next Tech Hubs: A Look at Housing Market and Migration Trends in Atlanta, Austin, D.C. and Other Hot Destinations for Tech Companies – Redfin

- These Low-Income Communities Should Prepare for an Influx of Cash – Zillow

- Homebuying Startups Keep Raising Money in Softer Housing Market – Bloomberg

- Housing Prices, Supply, and Innovation – Cato Institute

- Upzoning Under SB 50: The Influence of Local Conditions on the Potential for New Supply – University of California, Berkeley

- The Neighborhoods Where Housing Costs Devour Budgets – Citylab

- Available Affordable Housing Is Down Across The State, Report Finds – wbur

- The Growing Shortage of Affordable Housing for the Extremely Low Income in Massachusetts – Federal Reserve Bank of Boston

On other countries:

- [Australia] What do house prices do to jobs? – Macro Business

- [Canada] Toronto Housing Market Steadies as Sellers Bide Their Time – Bloomberg

- [Canada] Canada’s house price boom takes off – Global Property Guide

- [Czech Republic] Czech mortgage market continues to fall in February – ING

- [Indonesia] The housing market in Indonesia rarely makes big moves – Global Property Guide

- [Ireland] Ireland Property Rush Risks Repeat of Crisis – Bloomberg

- [Japan] What Housing Crisis? In Japan, Home Prices Stay Flat – Wall Street Journal

- [Japan] NIMBYs Argue New Housing Supply Doesn’t Make Cities Affordable. They’re Wrong. – Reason

- [Latvia] Latvia’s house price rises decelerating – Global Property Guide

- [New Zealand] Household Leverage and Asymmetric Housing Wealth Effects- Evidence from New Zealand – Reserve Bank of New Zealand

- [Singapore] Singapore’s house price rises accelerating – Global Property Guide

- [Switzerland] Slowdown inevitable for house prices in Switzerland – Global Property Guide

- [Switzerland] Swiss Regulator Calls for Measures to Avert Property Bubble – Bloomberg

- [United Kingdom] Should tenants fear the rise of the corporate landlord? – Financial Times

On cross-country:

- Affordable Housing Crisis Spreads Throughout World – Wall Street Journal

- Film Director: Don’t Just Blame Gentrification for Housing Crisis – Wall Street Journal

- Mind the data gap: commercial property prices for policy – Bank for International Settlements

On the US:

- Bank Balance Sheets and Liquidation Values: Evidence from Real Estate Collateral – SSRN

- Expectations During the U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts