Thursday, April 4, 2019

Assessing the Risk of the Next Housing Bust

From the IMF’s latest Global Financial Stability report:

“There’s good news for people living in Las Vegas, Miami and Phoenix: the risk of a housing bust like the one they endured during the global financial crisis is fairly small. For folks in Toronto and Vancouver, however, the picture hasn’t improved since 2008, and the risk of a large decline in house prices remains elevated.

Those are among the insights generated by the IMF’s new tool for assessing the danger of a severe downturn in home prices. Homeowners, of course, are keenly interested in the value of what is probably their biggest asset. But there is also a strong link between home prices, the financial system, and the economy. The link is especially powerful when prices go down – as we explain in Chapter Two of the IMF’s twice-yearly Global Financial Stability Report.

Why do home prices matter for the broader economy? Housing construction and related spending on things like home improvements account for one-sixth of the US and euro-area economies, making them among the largest components of GDP. What’s more, mortgages and other housing-related lending are a big part of banks’ assets in many countries, so changes in house prices affect the health of the banking system.

Boom-bust cycle

It’s no surprise, then, that more than two-thirds of financial crises in recent decades were preceded by a boom-bust cycle in home prices, and that central banks in the United States, China, Australia, and elsewhere have recently expressed concern about large increases in home prices.

Fortunately, the IMF’s new tool can help policy makers gauge the likelihood of a future housing downturn and take early steps to help limit the damage. The tool, dubbed House Prices at Risk, feeds into the Fund’s growth-at-risk model, which links financial conditions to the danger of an economic downturn (see the October 2017 GFSR .)

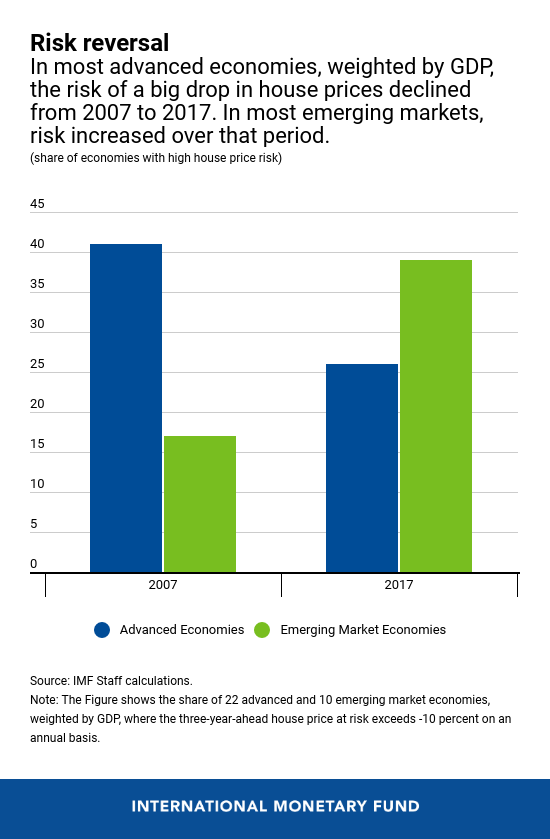

Our study encompasses data from 22 advanced economies, 10 emerging-market economies, and the major cities in those countries. We found that in most advanced economies in our sample, weighted by GDP, the odds of a big drop in inflation-adjusted house prices were lower at the end of 2017 than 10 years earlier but remained above the historical average. In emerging markets, by contrast, riskiness was higher in 2017 than on the eve of the global financial crisis. Nonetheless, downside risks to house prices remain elevated in more than 25 percent of these advanced economies and reached nearly 40 percent in emerging markets in our study. Among them, China stands out, especially its Eastern provinces.”

Continue reading here.

Posted by at 10:06 AM

Labels: Global Housing Watch

Subscribe to: Posts