Thursday, April 11, 2019

Stability of the labour shares: evidence from OECD economies

A new paper “revisits the old standing issue of the stability of labour shares. […] Empirical results indicate diverse patterns in labour share movements, the most preponderant being a downward deterministic trend with break(s). Upward trends are observed in a limited set of economies (Belgium, Luxembourg and the Netherlands). Overall, the stability of the labour share hypothesis appears to find only weak support. Exploratory analysis demonstrates that most of the structural breaks are economically significant and relate to the recent economic and political history of individual economies. The nature of labour share dynamics, as a country-specific and (to a large extent) policy and political phenomenon, is emphasized.”

A new paper “revisits the old standing issue of the stability of labour shares. […] Empirical results indicate diverse patterns in labour share movements, the most preponderant being a downward deterministic trend with break(s). Upward trends are observed in a limited set of economies (Belgium, Luxembourg and the Netherlands). Overall, the stability of the labour share hypothesis appears to find only weak support. Exploratory analysis demonstrates that most of the structural breaks are economically significant and relate to the recent economic and political history of individual economies.

Posted by at 11:00 PM

Labels: Inclusive Growth

Wednesday, April 10, 2019

Mirror, mirror on the wall, who is the richest of them all?

From a VoxEU post by Ricardo Perez-Truglia:

“Tax records became easily accessible online in Norway in 2001, allowing everyone in the country to observe the incomes of everyone else. This column offers evidence that people primarily went online to snoop on the incomes of friends, relatives, and other contacts. This game of income comparisons negatively affected the wellbeing of poorer Norwegians while at the same time boosting the self-esteem of the rich.

Technological advances have made it possible for everyone to know potentially everything about everyone else. Sci-fi shows such as Netflix’s Black Mirror imagine dystopian scenarios that could result from these new technologies. In the real world, social media is already allowing individuals to disclose details about their personal lives with strangers. This technological change has sparked a policy debate too: should governments disclose data such as tax records?

Tax transparency in Norway

To understand how far reaching the societal consequences of transparency could be, it is useful to look at the experience of one of the pioneers of transparency, namely, Norway. Tax records have been public in Norway since the 19th century, but they have not always been easily accessible. Before 2001, an individual had to make a formal request in person at a tax agency to see someone else’s income. In the fall of 2001, the Norwegian media digitised tax records and created websites that allowed any individual with internet access to search the entire country’s tax records easily and effortlessly. Every Norwegian could find out the incomes of anyone else in the country in a matter of seconds.

In the following decade, Norwegians engaged in a heated debate about whether tax records should be easily accessible online. A similar debate took place in neighbouring Sweden, Iceland, and Finland. These other Scandinavian countries also had laws making tax records public, and thus had to decide whether to make them easily available online as in Norway.

There was no consensus among politicians or the general public on whether Norway’s transparency was good or bad. At its core, the disagreement was about what the effects of transparency actually are. Some supporters argued that public records could serve to deter corrupt politicians and tax evaders (Bø et al. 2015). Meanwhile, detractors claimed that the tax records would be used in objectionable ways, to snoop on the incomes of friends, for example. Thus far, only qualitative and anecdotal evidence has substantiated this contention. In a recent paper (Perez-Truglia 2019), I provide the first quantitative evidence on the matter.

Figure 1 shows a screenshot of one of the websites that allowed Norwegians to browse the tax records. These websites were easy to use and became incredibly popular in the country for the following decade. ”

Continue reading here.

From a VoxEU post by Ricardo Perez-Truglia:

“Tax records became easily accessible online in Norway in 2001, allowing everyone in the country to observe the incomes of everyone else. This column offers evidence that people primarily went online to snoop on the incomes of friends, relatives, and other contacts. This game of income comparisons negatively affected the wellbeing of poorer Norwegians while at the same time boosting the self-esteem of the rich.

Posted by at 8:56 AM

Labels: Inclusive Growth

Rethinking the Phillips Curve: Inflation May Rise Modestly Next Year

From an article by Christopher G. Collins (PIIE) and Joseph E. Gagnon (PIIE):

“The US economy is running hot, with a record high rate of job vacancies and the lowest unemployment rate in nearly fifty years. Yet most forecasters predict no increase at all in inflation. This combination appears to challenge the validity of the Phillips curve, a popular economic model dating from the 1950s that predicts rising inflation when unemployment is low and falling inflation when unemployment is high. In a new paper, however, we show that the relationship between inflation and unemployment has shifted twice—in the late 1960s and in the mid-1990s. The paper replicates the findings of some other researchers, who find a very flat Phillips curve since the 1990s, implying that unemployment has little effect on inflation. But we also propose an alternative hypothesis: The Phillips curve is bent when inflation is low so that high unemployment has little downward effect on inflation, but low unemployment still pushes inflation up. If we are right, inflation is likely to rise modestly over the next couple of years. We will explore what this means for monetary policy in a subsequent post.

THE EVOLVING US PHILLIPS CURVE

Alban Phillips (1958) developed the original curve bearing his name. It related the rate of wage inflation to the unemployment rate in the United Kingdom over the period 1861–1913. Olivier Blanchard (2017, chapter 8) showed that a similar downward-sloping curve in terms of price inflation and unemployment was apparent in the United States in 1900–1960. Our paper confirms Blanchard’s finding that the rising inflation of the late 1960s led to the unmooring of expectations of inflation from the stable low levels that had prevailed before then and a shift in the Phillips curve to a relationship between the change in the rate of inflation and the unemployment rate. The return of inflation to a very low and stable level led to a second shift in the Phillips curve in the mid-1990s, back to a relationship between the level of inflation and the unemployment rate.

In addition to this shift in the persistence of inflation, many researchers have found that the Phillips curve has been very flat since the 1990s, so that changes in unemployment have little effect on inflation. This was most dramatically demonstrated in the aftermath of the Great Recession of 2008–09, when unemployment remained very high for years and yet inflation barely dipped. We show, however, that another hypothesis fits the data equally well: The Phillips curve may become bent when inflation is low, with a flat portion for high unemployment and a steeper portion for low unemployment.”

Continue reading here.

From an article by Christopher G. Collins (PIIE) and Joseph E. Gagnon (PIIE):

“The US economy is running hot, with a record high rate of job vacancies and the lowest unemployment rate in nearly fifty years. Yet most forecasters predict no increase at all in inflation. This combination appears to challenge the validity of the Phillips curve, a popular economic model dating from the 1950s that predicts rising inflation when unemployment is low and falling inflation when unemployment is high.

Posted by at 8:55 AM

Labels: Macro Demystified

Tuesday, April 9, 2019

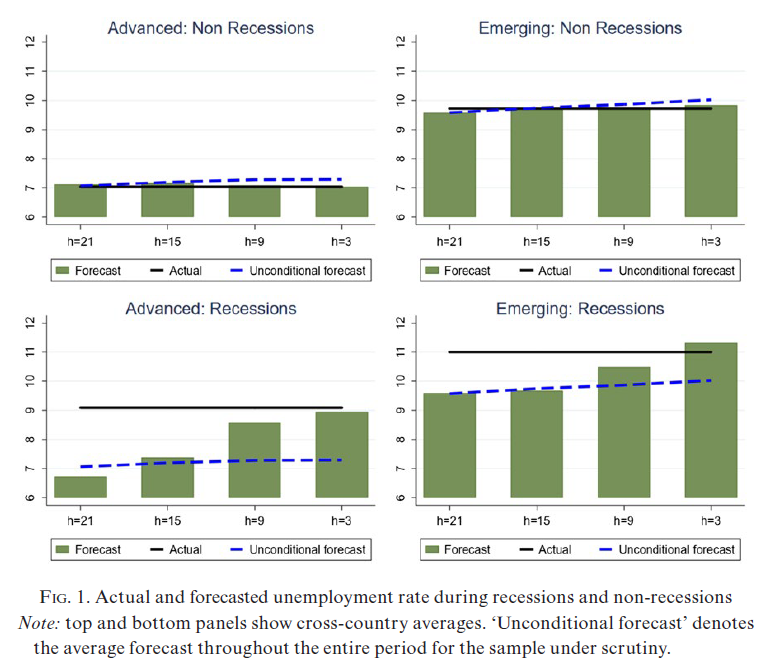

An Assessment of the IMF’s Unemployment Forecasts

My new paper with Zidong An and Joao Jalles was just published in Manchester School:

“This paper assesses the performance of the IMF’s unemployment forecasts for 84 countries, both advanced and emerging market economies, between 1990 and 2015. The forecasts are reported in the World Economic Outlook, a leading IMF publication. The forecasts display a small amount of bias—they tend to predict lower unemployment outcomes than occur—which arises because the forecasters fail to predict accurately the sharp increase in unemployment during downturns. Forecasts are characterized by inefficiency (errors of the past are repeated in the present) and rigidity (forecast revisions are serially correlated). There is little to choose between IMF and Consensus Forecasts, a source of private sector forecasts, for the small subset of 12 countries for which both sets of forecasts are available.”

My new paper with Zidong An and Joao Jalles was just published in Manchester School:

“This paper assesses the performance of the IMF’s unemployment forecasts for 84 countries, both advanced and emerging market economies, between 1990 and 2015. The forecasts are reported in the World Economic Outlook, a leading IMF publication. The forecasts display a small amount of bias—they tend to predict lower unemployment outcomes than occur—which arises because the forecasters fail to predict accurately the sharp increase in unemployment during downturns.

Posted by at 10:45 PM

Labels: Forecasting Forum

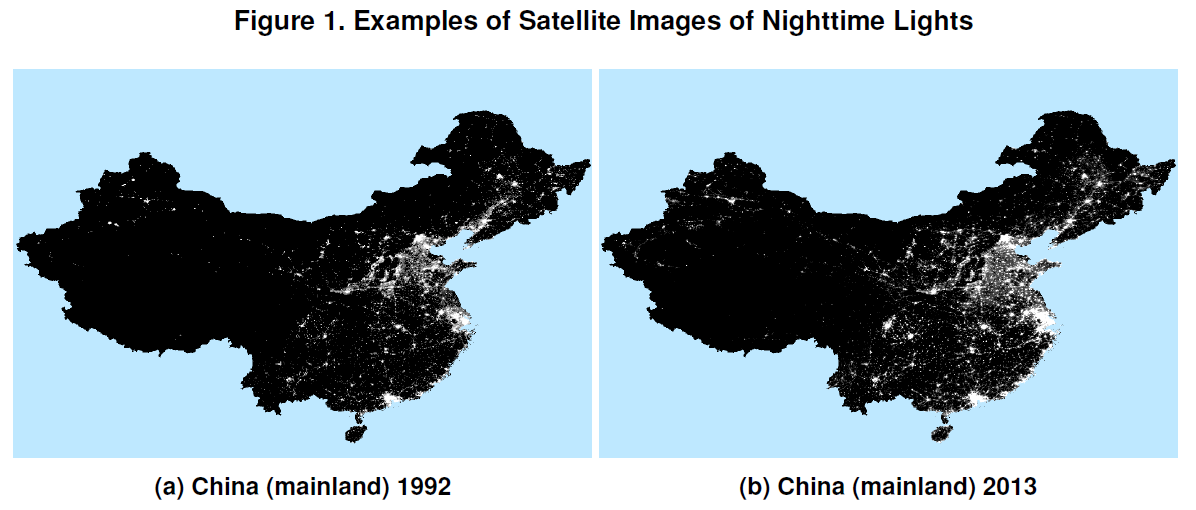

Illuminating Economic Growth

From a new IMF working paper:

“In this paper, we show that nighttime lights can be a useful source of information to improve official real GDP data. To begin with, they can be used to detect the uncertainty in official data and potential mismeasurement of real GDP. Systematic differences between the new and official measures may warrant further investigation as to what contributes to such differences. While nighttime lights can be computationally intensive to process, the method developed in this paper is not limited to nighttime lights. In fact, measures of real GDP that are conditionally independent of official data can be used in a similar fashion.”

“Figure 1 compares satellite images of nighttime lights for mainland China, […] Variation in nighttime lights may thus contain useful information on China’s real economic growth.”

Continue reading here.

From a new IMF working paper:

“In this paper, we show that nighttime lights can be a useful source of information to improve official real GDP data. To begin with, they can be used to detect the uncertainty in official data and potential mismeasurement of real GDP. Systematic differences between the new and official measures may warrant further investigation as to what contributes to such differences. While nighttime lights can be computationally intensive to process,

Posted by at 10:41 PM

Labels: Inclusive Growth

Subscribe to: Posts