Friday, September 14, 2018

Housing View – September 14, 2018

On cross-country:

- Affordable Housing Governance and Finance: Innovations, partnerships and comparative perspectives – Taylor & Francis Group

- Housing & Migration – A Research Briefing – Housing Europe Observatory

- Affordable housing in Europe: how do the various member-states do it? – Housing Europe Observatory

- “Investing in affordable housing comes with a high return both socially and financially” – Barcelona City Council

- Housing Europe supports the Municipalist Declaration of Local Governments for the Right to Housing and the Right to the City – Housing Europe Observatory

- Can Housing Be Affordable Without Being Efficient? – World Resources Institute

- These May Be the World’s 10 Riskiest Housing Markets – Bloomberg

On the US:

- Ben Carson and HUD Get Ready to Take On the Nimbys – Bloomberg

- Mapping the boom in nonbank mortgage lending—and understanding the risks – Brookings

- Is the housing price-rent ratio a leading indicator? – Federal Reserve Bank of St. Louis

- Americans are now better off renting than buying. Above all, avoid buying in Dallas! – Global Property Guide

- Rental Glut Sends Chill Through the Hottest U.S. Housing Markets – Bloomberg

- Mortgage Fraud Fueled the Financial Crisis—and Could Again – Institute of New Economic Thinking

- Voters Can Keep Housing Affordable – New York Times

- Book Review: High-Risers: Cabrini-Green and the Fate of American Public Housing – The New York Review of Books

- The Financial Crisis Changed Home Buying Forever – Wall Street Journal

- Preserving Affordable Rental Housing – MacArthur Foundation

- The Housing Bubble Burst All Over Reality TV – New York Times

- Maryland’s Biggest County Responds to Full Schools by Halting New Housing – Slate

- City NIMBYS – Furman Center for Real Estate and Urban Policy

On other countries:

- [Australia] Chinese real estate investment in Australia drops by nearly 30% – Macro Business

- [China] How Much Would China’s GDP Respond to a Slowdown in Housing Activity? – Federal Reserve Bank of Kansas City

- [Iceland] Iceland’s house prices continue to rise, albeit at a slower pace – Global Property Guide

- [Ireland] House prices in Ireland continue to rise at breakneck speed – Global Property Guide

- [Portugal] Portugal’s housing market remains robust – Global Property Guide

- [Portugal] Qué son las “visas doradas” y por qué causan polémica en Portugal – BBC

- [Romania] Romania’s house price growth decelerating sharply – Global Property Guide

- [Spain] The financial transmission of housing bubbles: Evidence from Spain – VoxEU

- [Spain] Te presentamos a tu casero: se llama Blackstone y es dueño de medio Madrid – GQ

- [Sweden] Sweden’s house price boom is officially over – Global Property Guide

- [Switzerland] Holes in Swiss property market ring mortgage alarm bells – Reuters

- [Thailand] Thailand’s house prices rising strongly again – Global Property Guide

- [United Kingdom] Housing affordability: Is new local supply the key? – Sage Journals

Photo by Aliis Sinisalu

On cross-country:

- Affordable Housing Governance and Finance: Innovations, partnerships and comparative perspectives – Taylor & Francis Group

- Housing & Migration – A Research Briefing – Housing Europe Observatory

- Affordable housing in Europe: how do the various member-states do it? – Housing Europe Observatory

- “Investing in affordable housing comes with a high return both socially and financially” – Barcelona City Council

- Housing Europe supports the Municipalist Declaration of Local Governments for the Right to Housing and the Right to the City – Housing Europe Observatory

- Can Housing Be Affordable Without Being Efficient?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, September 13, 2018

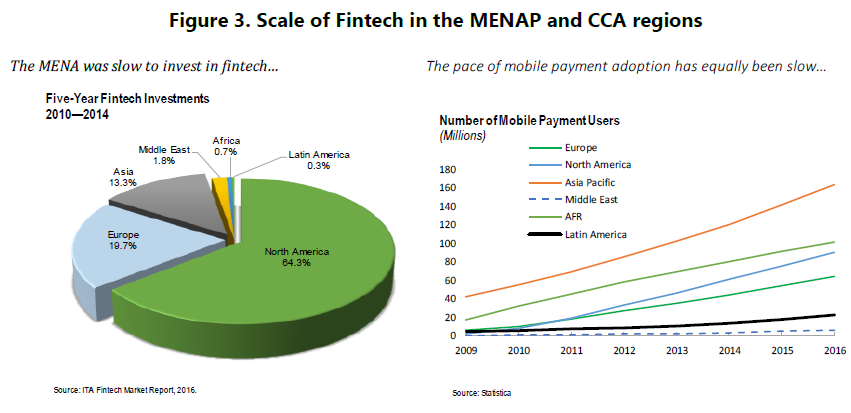

Fintech, Inclusive Growth and Cyber Risks in the MENAP and CCA Regions

From a new IMF working paper:

“Financial technology (fintech) is emerging as an innovative way to achieve financial inclusion and the broader objective of inclusive growth. In addition to improving the speed, convenience, and efficiency of financial services, fintech has potential to promote financial inclusion. More specifically, it can enhance access to affordable financial services for unbanked populations and underserved small and medium sized enterprises (SMEs); reduce delays and costs in cross-border remittances; foster efficiencies and transparency in government operations, which helps reduce corruption, and facilitate social and humanitarian transfers in a manner that preserves human dignity.”

“For the Middle East, North Africa, Afghanistan and Pakistan (MENAP) and Caucasus and Central Asia (CCA) regions, fintech has a particularly valuable role to play as these potential benefits are aligned with the regions’ policy priorities. Both regions have countries with large unbanked populations, SMEs whose growth is constrained by limited access to finance, high youth unemployment, large remittance markets and informal transfers (Hawala), undiversified economies, vulnerabilities to terrorism, large income disparities, large displaced populations, and endemic corruption. Fintech innovations and underlying technologies can contribute to the solutions for many of these challenges.”

“The scale and pace of fintech in MENAP and CCA countries, however, lags other regions, and fintech is yet to foster an inclusive digital economy. Although there is significant diversity in the pace with which countries in both regions are adopting fintech, overall investment into fintech and the uptake of fintech and mobile financial services have been low compared to other regions. There also continues to be a strong preference for cash payments in the Middle East, despite the growth of e-commerce transactions. Consequently, the potential gap remains large in key areas such as financial inclusion, access to SMEs, diversification, reducing informal sector and the broader objective of inclusive growth.”

From a new IMF working paper:

“Financial technology (fintech) is emerging as an innovative way to achieve financial inclusion and the broader objective of inclusive growth. In addition to improving the speed, convenience, and efficiency of financial services, fintech has potential to promote financial inclusion. More specifically, it can enhance access to affordable financial services for unbanked populations and underserved small and medium sized enterprises (SMEs); reduce delays and costs in cross-border remittances;

Posted by at 4:05 PM

Labels: Inclusive Growth

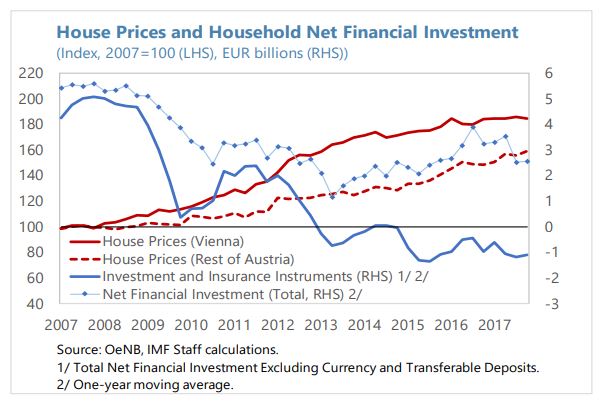

Housing Market Developments in Austria

The IMF’s latest report on Austria says:

“The Austrian housing market has shown a strong trend rise in valuations over the last decade, mainly driven by price increases in Vienna. Prices stagnated through the mid-2000s

but have since outpaced most of Austria’s EU peers. In September 2016, the ESRB issued Austria a warning on medium-term residential real estate vulnerabilities because of the robust price and credit growth and the risk of further loosening in credit standards. Recently, price growth moderated to 4.7 percent (y/y) at end-2017, due to a slowdown in Vienna, though prices accelerated in the rest of the country.”

While the robust price growth has largely reflected underlying market fundamentals, the nationwide market has recently started to show signs of modest overvaluation. Housing demand has been buoyed by demographic factors, including the spike in immigration in 2015–16, and low interest rates which also have increased the attractiveness of housing assets as a form of saving. Supply-side constraints, such as land availability, have also played a role, despite some recent pickup in construction activity. The OeNB’s fundamentals indicator for residential property prices suggests a modest overvaluation of around 10 percent for Austria in 2017 (and a larger overvaluation for Vienna of about 20 percent), broadly corresponding to a range of ECB indicators as of end-2017.

Real estate related financial stability risks are nonetheless contained. The rise in mortgage debt in Austria has been modest compared to other EU countries experiencing large property price increases, and its share relative to households’ incomes has remained stable and among the lowest in the Euro Area. Residential real estate exposures account for only about a fifth of Austrian banks’ total loan stock and about 150 percent of consolidated CET-1 capital. Furthermore, the prevalence of rental accommodation (about half and three-quarters of housing nationwide and in Vienna, respectively) shield a large share of the population from adverse price developments. Less than half of homeowners have outstanding mortgages, and they also typically have higher incomes and net wealth relative to the rest of the population.

Some pockets of vulnerability and early signs of increasing risks nonetheless warrant continued close monitoring. The share of foreign exchange denominated housing loans at around

15 percent remains high relative to Austria peers, although it has declined significantly in recent years. Furthermore, the recent prolonged period of low lending rates saw a significant increase in the share of variable interest rate mortgages, which despite a recent decline still amount to about three-quarters of the total stock. There are also signs of some easing in banks’ lending standards, with a rising—albeit still limited—share of relatively high loan-to-value, debt service-to-income, and debt-to-income ratios in new housing loans to households.Supply side measures could help ease the modest price imbalances over time, while the recently expanded macroprudential toolkit can help prevent a build-up of systemic risks.

Measures to address supply-side constraints could include reviewing zoning regulations and other restrictions on construction. Addressing outdated property tax valuations could help improve residential mobility and market efficiency. At the same time, the new real-estate specific macroprudential policy tools provide additional scope for tailored preventive measures to ensure systemic risks arising from the mortgage market remain contained. These are accompanied by new reporting requirements, expected to be introduced in 2019, to facilitate evaluation of risks and impact of potential policy changes. They also complement a 2016 call by the Financial Market Stability Board for the Austrian banks to maintain sustainable lending standards, although the guidance does not specify quantitative limits for the vulnerability ratios.”

The IMF’s latest report on Austria says:

“The Austrian housing market has shown a strong trend rise in valuations over the last decade, mainly driven by price increases in Vienna. Prices stagnated through the mid-2000s

but have since outpaced most of Austria’s EU peers. In September 2016, the ESRB issued Austria a warning on medium-term residential real estate vulnerabilities because of the robust price and credit growth and the risk of further loosening in credit standards.

Posted by at 10:57 AM

Labels: Global Housing Watch

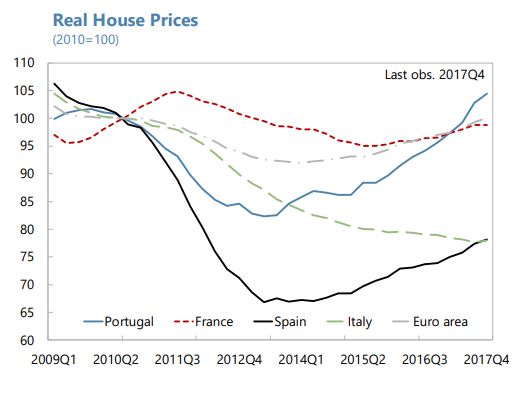

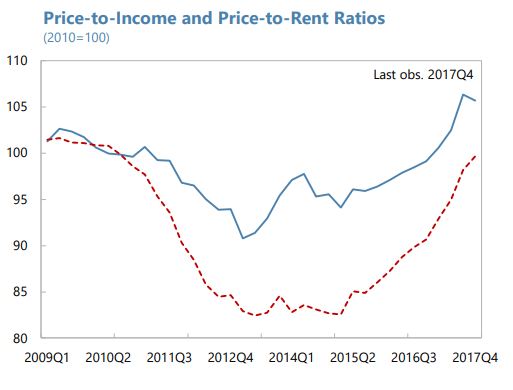

House Prices in Portugal

The IMF’s new report on Portugal says:

“Housing prices continue to increase, but there is no significant overvaluation yet. Following a decline of 18 percent in real terms over 2010–13, housing prices have since increased by

about 20 percent in real terms (7.9 percent in 2017), especially in Lisbon, Porto and the Algarve region. While the increases have been driven largely by transactions on existing dwellings by non-residents, the share of housing transactions financed by Portuguese mortgages has been growing since 2015 (reaching 41 percent in the last quarter of 2017). Estimates in the ECB’s May 2018 Financial Stability Review suggest that there are incipient signs of overvaluation in the residential real estate market. The authorities should continue to improve the quality of real estate data and related analytical tools, and to monitor mortgage markets and the evolution of risks to banks from developments in real estate markets.”

The IMF’s new report on Portugal says:

“Housing prices continue to increase, but there is no significant overvaluation yet. Following a decline of 18 percent in real terms over 2010–13, housing prices have since increased by

about 20 percent in real terms (7.9 percent in 2017), especially in Lisbon, Porto and the Algarve region. While the increases have been driven largely by transactions on existing dwellings by non-residents, the share of housing transactions financed by Portuguese mortgages has been growing since 2015 (reaching 41 percent in the last quarter of 2017).

Posted by at 10:44 AM

Labels: Global Housing Watch

Wednesday, September 12, 2018

Carbon Taxation for International Maritime Fuels: Assessing the Options

From a new IMF working paper by Ian Parry, Dirk Heine, Kelley Kizzier, and Tristan Smith:

“The International Maritime Organization (IMO) announced in April 2018 a target of cutting greenhouse gas (GHG) emissions from the sector by 50 percent below 2008 levels by 2050

and subsequent meetings of the IMO will develop a strategy for making headway on this commitment. This paper seeks to inform dialogue about the possibility of a carbon tax as a

key element of GHG mitigation policy for international maritime transport. The paper discusses the case for the tax over alternative mitigation instruments, options for the practical

design issues, and then presents estimates of the impacts of carbon taxation and other instruments from an analytical model of the maritime sector.”

From a new IMF working paper by Ian Parry, Dirk Heine, Kelley Kizzier, and Tristan Smith:

“The International Maritime Organization (IMO) announced in April 2018 a target of cutting greenhouse gas (GHG) emissions from the sector by 50 percent below 2008 levels by 2050

and subsequent meetings of the IMO will develop a strategy for making headway on this commitment. This paper seeks to inform dialogue about the possibility of a carbon tax as a

key element of GHG mitigation policy for international maritime transport.

Posted by at 9:59 AM

Labels: Energy & Climate Change

Subscribe to: Posts