Tuesday, April 10, 2018

Global Investors, House Price Dispersion, and Synchronicity

From IMF’s Global Financial Stability Report – April 2018:

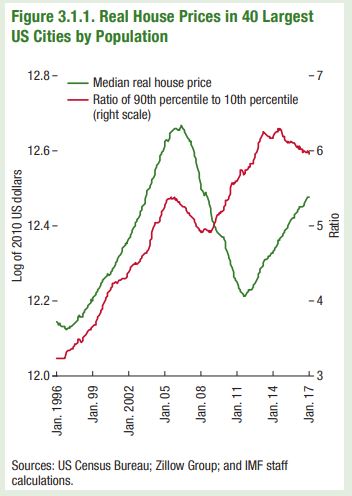

“House price dispersion can be used as a proxy for demand from high-net-worth foreign investors with a preference for luxury housing. Using granular data from the US housing market, this box finds that house price dispersion in the United States has increased sharply over recent decades, and it increases when house prices in alternative investment destinations outside the United States rise. Both findings point to global investors contributing to house price synchronicity across cities and countries.”

Continue reading here.

From IMF’s Global Financial Stability Report – April 2018:

“House price dispersion can be used as a proxy for demand from high-net-worth foreign investors with a preference for luxury housing. Using granular data from the US housing market, this box finds that house price dispersion in the United States has increased sharply over recent decades, and it increases when house prices in alternative investment destinations outside the United States rise.

Posted by at 10:29 AM

Labels: Global Housing Watch

For Home Prices in London, Check the Tokyo Listings

From IMFBlog:

“If house prices are rising in Tokyo, are they also going up in London?

Increasingly, the answer is yes.

In recent decades, house prices around the world have shown a growing tendency to move in the same direction at the same time. What accounts for this phenomenon, and what are the implications for the world economy? These are questions that IMF economists explore in Chapter 3 of the latest Global Financial Stability Report.

Our study of 44 cities and 40 advanced and emerging-market economies shows that the growing integration of financial markets plays an important role. As a result, housing markets in one country are more sensitive to swings in another. Policy makers should pay attention, because the heightened tendency for house prices to move in tandem may signal greater odds of an economic slowdown. An economic shock in one part of the world is more likely to affect housing markets elsewhere.

Let’s look at why home prices are more synchronized in a financially integrated world.

- Interest rates: The world’s major central banks have kept interest rates unusually low for a long time in a bid to stimulate growth. That has produced a ripple effect of low borrowing costs, including cheap mortgages, across the globe, which has helped push up prices.

- Institutional investors , private equity firms, and Real Estate Investment Trusts have been increasingly active in major cities such as Amsterdam, Sydney, and Vancouver as they seek out higher returns.

- Wealthy individuals have also snapped up properties in major financial centers in search of safe places to invest their money (and perhaps to live). One result: because the wealthy prefer high-end properties, their investments push up prices in expensive neighborhoods in places like New York and London at the same time.

- Economic growth: In addition to financial factors, coordinated movements in the real economy contribute to the phenomenon. In 2017, growth picked up in 120 economies, accounting for three-quarters of world GDP. It was the broadest synchronized growth surge since 2010. Economic growth is a major driver of demand for homes, and hence prices.

All of this suggests that house prices are starting to behave more like the prices of financial assets, such as stocks and bonds, which are influenced by investors elsewhere in the world. In countries that are more open to global capital flows, prices of both homes and equities tend to be more synchronized with global markets.”

Continue reading here.

From IMFBlog:

“If house prices are rising in Tokyo, are they also going up in London?

Increasingly, the answer is yes.

In recent decades, house prices around the world have shown a growing tendency to move in the same direction at the same time. What accounts for this phenomenon, and what are the implications for the world economy? These are questions that IMF economists explore in Chapter 3 of the latest Global Financial Stability Report.

Posted by at 10:25 AM

Labels: Global Housing Watch

Monday, April 9, 2018

Financial Times: IMF Shows Poor Track Record at Forecasting Recessions

The FT cites my new working paper with Zidong An and Joao Jalles:

“Recessions are not rare,” echoed Prakash Loungani, a macro-economist at the IMF. “What is rare is a recession that is forecast in advance.” Despite an increased amount of economic data being available, “the ability to predict downturns remains dismal”, he told the FT.”

[…]

The fact that forecasts are “typically over-optimistic for horizons beyond the current year” is not necessarily the result of economist optimism. They “fail to forecast strong booms, just as they fail to predict recessions,” said Mr Loungani, suggesting that economic forecasts “are too rooted in thinking that things stay close to normal or will revert to normal soon”.

[…]

“The IMF’s April outlook is often more accurate. This is because it is easier to get a forecast right for the current year than the following year. The April report is better able to signal a recession for the current year than the October publication, “but one that is much milder than what transpires”, says Mr Loungani, author of several studies.”

Continue reading here.

The FT cites my new working paper with Zidong An and Joao Jalles:

“Recessions are not rare,” echoed Prakash Loungani, a macro-economist at the IMF. “What is rare is a recession that is forecast in advance.” Despite an increased amount of economic data being available, “the ability to predict downturns remains dismal”, he told the FT.”

[…]

The fact that forecasts are “typically over-optimistic for horizons beyond the current year”

Posted by at 11:08 AM

Labels: Forecasting Forum

Friday, April 6, 2018

Work-Welfare Trade-offs and Structural Unemployment in Luxembourg

From the IMF’s latest report on Luxembourg:

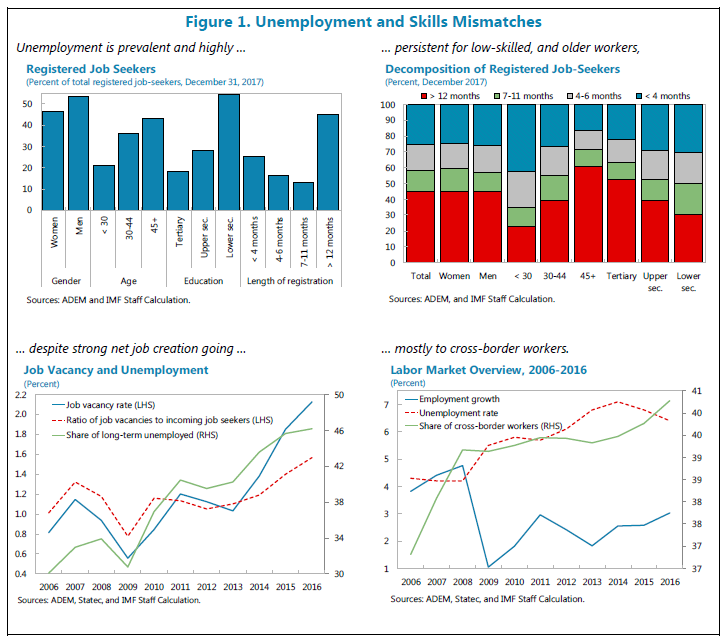

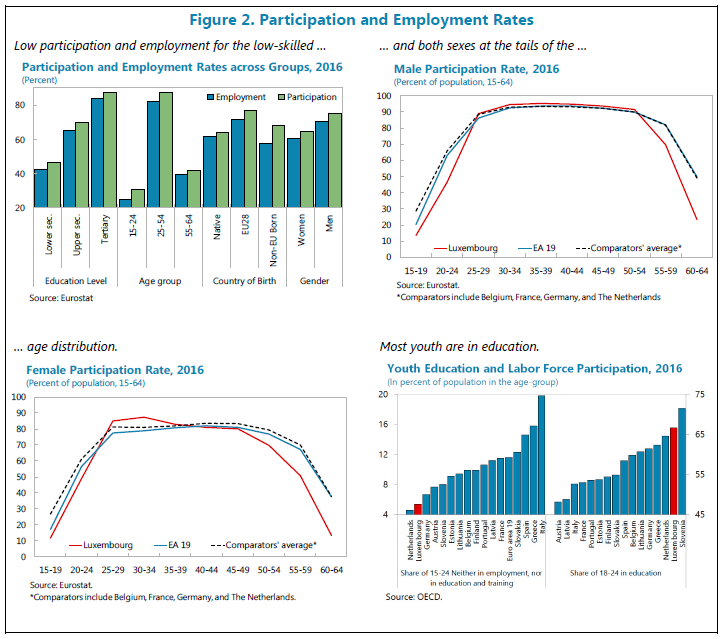

“Job creation is strong in Luxembourg, but unemployment is declining gradually and many newly created jobs go to cross-border workers. The employment rate of residents is relatively low, especially for low-skilled, young, and older workers. Moreover, female attachment to the labor market is weak, and the share of the long-term unemployed has increased over the last ten years, but seems to have come down somewhat in recent months. In addition to skills mismatches, work disincentives inherent to the tax-benefits system are a factor in explaining structural unemployment.”

“[…] low employment of older workers and women is largely driven by low participation rates among these groups, while both higher unemployment and lower participation contribute to the low employment rates of low-skilled workers. The relative importance of the different benefit schemes varies across groups of workers. The high unemployment of young and low-skilled workers reflects substantial unemployment traps inherent to the tax-benefits system, while high disincentives for second earners contribute to lower participation of women, and weak labor market attachment of seniors is predominantly driven by the generosity of the pensions system. Substantially increasing employment requires efforts to reduce skills mismatches and to make work more rewarding.”

Continue reading here.

From the IMF’s latest report on Luxembourg:

“Job creation is strong in Luxembourg, but unemployment is declining gradually and many newly created jobs go to cross-border workers. The employment rate of residents is relatively low, especially for low-skilled, young, and older workers. Moreover, female attachment to the labor market is weak, and the share of the long-term unemployed has increased over the last ten years, but seems to have come down somewhat in recent months.

Posted by at 1:23 PM

Labels: Inclusive Growth

Impact of Monetary Policy on Luxembourg

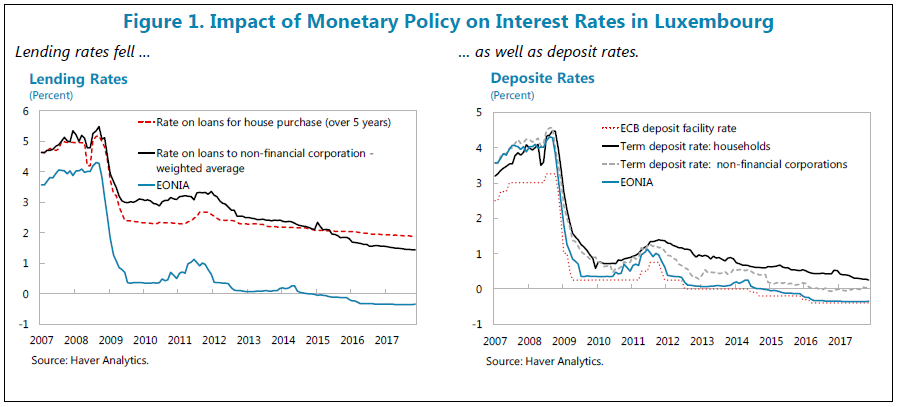

A new IMF report says that “Accommodative monetary policy has contributed to the performance of the Luxembourg economy through some expansion of aggregate demand and through its impact on the financial system. Banks have remained profitable and interest margins stable, while fee and commission income from fund and other activity has been healthy. The investment fund industry has benefited from various factors such as portfolio rebalancing, search for yield, and other market developments leading to strong inflows into various classes of investment funds, and through strong valuation effects. Scenario analysis suggest that the fund industry could be adversely impacted by sharp interest rate increases and that, because of interconnections, the banking system would also be affected. Margins of some banks could also decline when interest rate normalize. Against this backdrop, it is important to implement all 2017 FSAP recommendations that will contribute to making the financial system more resilient to shocks, including those arising from faster-than-expected monetary policy normalization.”

Continue reading here.

A new IMF report says that “Accommodative monetary policy has contributed to the performance of the Luxembourg economy through some expansion of aggregate demand and through its impact on the financial system. Banks have remained profitable and interest margins stable, while fee and commission income from fund and other activity has been healthy. The investment fund industry has benefited from various factors such as portfolio rebalancing, search for yield, and other market developments leading to strong inflows into various classes of investment funds,

Posted by at 1:13 PM

Labels: Inclusive Growth

Subscribe to: Posts