Tuesday, April 17, 2018

World Economic Outlook, April 2018 Cyclical Upswing, Structural Change

The IMF just launched the April 2018 World Economic Outlook:

“The global economic upswing that began around mid-2016 has become broader and stronger. This new World Economic Outlook report projects that advanced economies as a group will continue to expand above their potential growth rates this year and next before decelerating, while growth in emerging market and developing economies will rise before leveling off. For most countries, current favorable growth rates will not last. Policymakers should seize this opportunity to bolster growth, make it more durable, and equip their governments better to counter the next downturn.”

Chapter 2 notes that “Dao, Furceri, and Loungani (2014) highlight the increasing role of participation as an absorber of state-level labor demand shocks.”

Chapter 3 notes the findings from my paper with Saurabh Mishra, Chris Papageorgiou, and Ke Wang that “Cross-border trade in services has been growing steadily over the past four decades, and now accounts for about one-fifth of global exports. […] The increase in the tradability of services is widespread across countries. […] In terms of industries, the increase in service exports has been particularly large in “modern” services that can be delivered at a distance, such as telecommunications, computer and information services, intellectual property, financial intermediation, and other business activities, including research and development and professional services.”

The full report is available here. My paper on regional labor market adjustment is available here. My paper on services trade is available here.

The IMF just launched the April 2018 World Economic Outlook:

“The global economic upswing that began around mid-2016 has become broader and stronger. This new World Economic Outlook report projects that advanced economies as a group will continue to expand above their potential growth rates this year and next before decelerating, while growth in emerging market and developing economies will rise before leveling off. For most countries, current favorable growth rates will not last.

Posted by at 4:17 PM

Labels: Inclusive Growth

Economic Growth from Octavian to Obama

From HumanProgress by Marian L. Tupy:

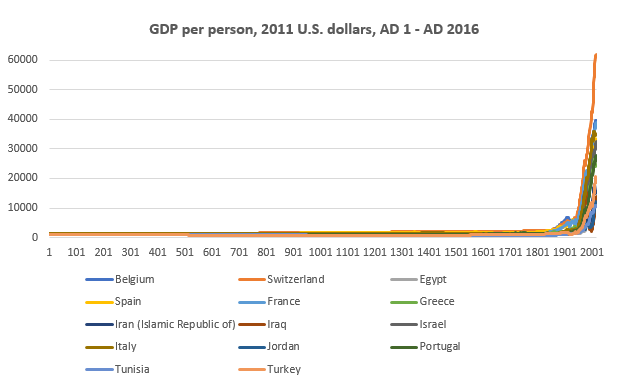

“Earlier this year, the Groningen Growth and Development Centre released a new edition of its Maddison Project Database, which provides information on global growth and income levels over the long run. The 2018 version of the data, first compiled by the late University of Groningen economics professor Angus Maddison, covers 169 countries up to the year 2016. Some information, dealing with parts of Europe and the Middle East, goes back to the time of Christ (or, for the secularly inclined, Rome’s first emperor, Octavian). It provides a stunning window on humanity’s struggle to generate and sustain rapid economic growth, until recent centuries ushered in the current Age of Abundance.”

“Angus Maddison, the British quantitative macroeconomic historian who died in 2010, spent his adult life estimating gross domestic product (GDP) figures for a growing range of countries over a lengthening period of time. In 1995, he published GDP estimates for 56 countries going back to 1820. In 2001, he extended his estimates to the beginning of the Christian Era. To some, Maddison’s numbers are “no more than educated guesses.” To others, they are “fictions, as real as the relics peddled around Europe in the Middle Ages.” But, Maddison’s research served an important purpose. “In disputing his figures,” The Economist predicted, future “scholars would be inspired to provide their own.” And so it proved to be.”

“The Maddison Project started in March 2010, when a group of Maddison’s colleagues decided to continue the Briton’s work on measuring economic performance for different regions and time periods. The latest edition of the GDP data was five years in the making and while the numbers have changed, the economic growth trend lines have stayed the same. As in previous editions of the data, human economic history resembles a hockey stick, with a long straight shaft and an upward-facing blade. For thousands of years, economic growth was negligible (resembling that long straight shaft). At the end of the 18th century, however, economic growth and, consequently, the standard of living, started to accelerate in Great Britain and then in the rest of the world (resembling that upward-facing blade).”

“That the early data should be most readily available for the constituent parts of the Roman Empire and Mesopotamia is unsurprising, since documentary and archeological evidence from those two regions is plentiful. According to the researchers at GGDC, real or inflation adjusted income per person around the time of Octavian (63 BC – AD 14) varied from $1,546 in Italy to $973 in Spain. That amounts to between $4.2 and $2.7 per person per day. It is a testament to the unevenness of economic development that, over two millennia later, some countries are still stuck at those (and even lower) levels. In 2016, GDP per person in Burundi, Central African Republic, Democratic Republic of Congo, Liberia, Malawi and Niger was $692, $619, $836, $764, $950 and $906 respectively.”

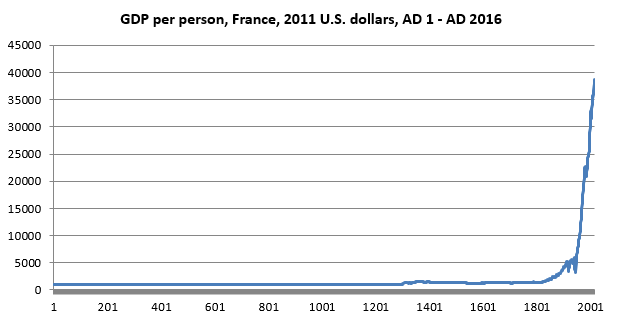

“Those African countries are outliers, of course. In most of the world, GDP per capita has risen dramatically, especially over the last two centuries. To get a sense of how recent and unprecedented the Age of Abundance is, consider France. In AD 1, GDP per person in the Roman province of Gaul was $1,050 – and that’s where it remained for the next 13 (yes, thirteen) centuries. During the first half of the 14th century, however, French incomes rose by some 50 percent, reaching a high of $1,553 in 1355. Why?”

“The end of the Medieval Warm Period in the late 13th century led to cooler weather and higher rainfall. Harvests shrunk and famines proliferated (e.g., 1304, 1305, 1310, 1315–1317, 1330–34 and 1349–51). To make matters much worse, the Black Plague (1347-1351) wiped out between 75 and 80 percent of those French who survived the climate change. Curiously, the two catastrophes had a salutary effect on both the economic and institutional developments in Western Europe. Abundance of land and agricultural tools seemed to have increased productivity of the surviving peasants, while labor shortages encouraged the lower classes to demand better treatment from their feudal overlords. As a consequence, serfdom gradually disappeared from the region, although it continued to persist in Eastern Europe, where the Black Plague was, due to lower population density, much less deadly.”

“As the population of Western Europe recovered, incomes waxed and waned, neither falling to their pre-plague levels, nor rising above their mid-14th century maximum. Thus, as late as 1831, the average GDP per person in France was only $1,534. Put differently, in the 18 centuries that separated the reigns of the first Roman Emperor and the last French king (Louis Phillipe), incomes rose by a paltry 50 percent. The Industrial Revolution, a British import, changed French fortunes considerably. Between 1831 and 1881, incomes rose by 100 percent ($3,067). As such, France made twice as much economic progress in 50 years as it did in the previous 1,800 years. In 2016, French GDP per capita stood at $38,758, meaning that a modern Frenchman is roughly-speaking 24 times better off (in real terms) than his ancestor 200 years ago. Remarkable.”

“France, of course, was not alone. Similar stories unfolded in other parts of the West. A year before the Declaration of Independence, American GDP per person stood at $1,883. By the time Barack Obama left office, U.S. GDP per person stood at $53,015 – a 27 fold increase. Today, abundance is no longer restricted to the West. As previously under-developed countries embraced industrialization and trade, they prospered. In 1978, when China started to reform its failing communist economy, its GDP per person stood at $1,583 (French levels in the early 1830s). By 2016, it rose to $12,320 (the French level in 1964). To put that progress in perspective, China grew as much in 38 years, as France did in 130 years. That, too, is noteworthy, for it demonstrates that, given correct policies, countries don’t have to reinvent the wheel. They can adopt ideas and technologies that took advanced countries millennia to develop and leapfrog from extreme poverty into the Age of Abundance within a couple of generations.”

From HumanProgress by Marian L. Tupy:

“Earlier this year, the Groningen Growth and Development Centre released a new edition of its Maddison Project Database, which provides information on global growth and income levels over the long run. The 2018 version of the data, first compiled by the late University of Groningen economics professor Angus Maddison, covers 169 countries up to the year 2016. Some information, dealing with parts of Europe and the Middle East,

Posted by at 3:31 PM

Labels: Inclusive Growth, Macro Demystified

Sunday, April 15, 2018

Do Wide-Reaching Reform Programmes Foster Growth?

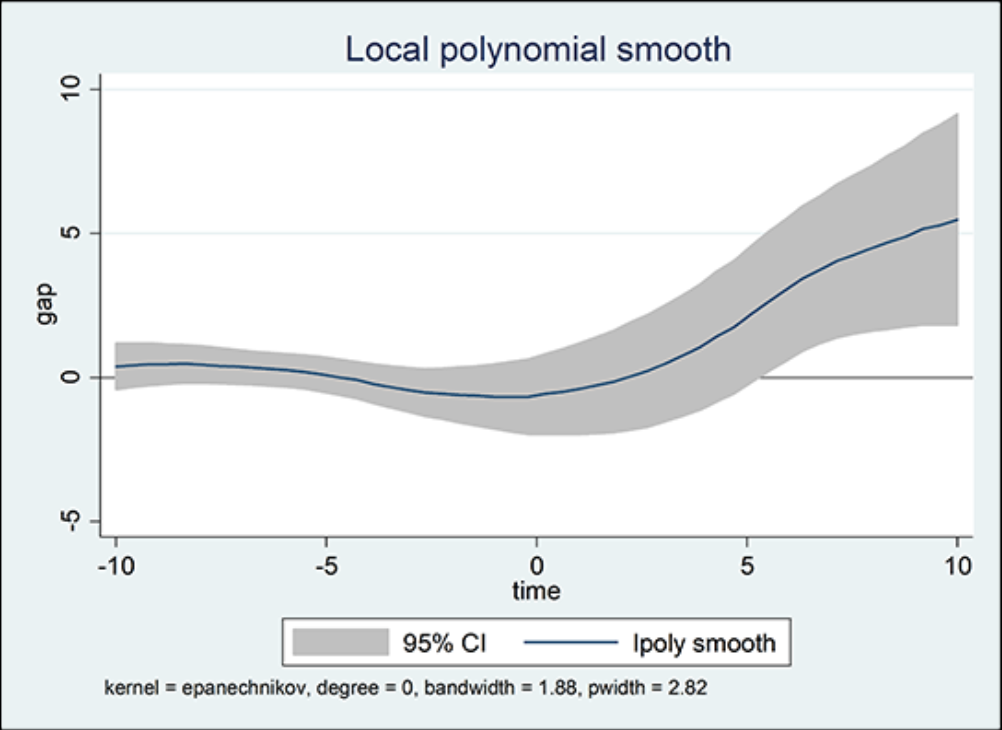

A new Bruegel post estimates “the impact of large reform waves implemented in the past 40 years worldwide, [and shows] that reforms had a negative but statistically insignificant impact in the short term. […] Reforming countries, however, experienced significant growth acceleration in the medium-term. As a result, 10 years after the reform wave started, GDP per capita was roughly six percentage points higher than the synthetic counterfactual scenario.”

Figure 2. Statistical analysis on the difference between the two

Source: Marrazzo and Terzi (2017)

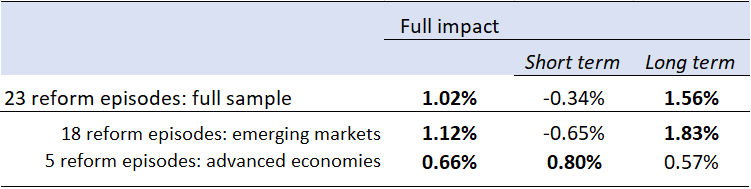

On the heterogeneity of reform impact, “The overall positive effect of reforms is confirmed in both instances (Table 1). However, advanced economies seem to have reaped fewer benefits from their extensive reform programmes than emerging markets. Moreover, the time-profiling of the pay-offs seems somewhat different; while countries closer to the technological frontier, and probably with better institutions, see benefits from reforms in the first five years, these materialise only in the longer run for emerging markets.”

Table 1. Average impact of reforms on yearly per capita GDP growth rate vis-à-vis counterfactual

Note: Bold indicates significance at the 5% level

Source: Marrazzo and Terzi (2017)

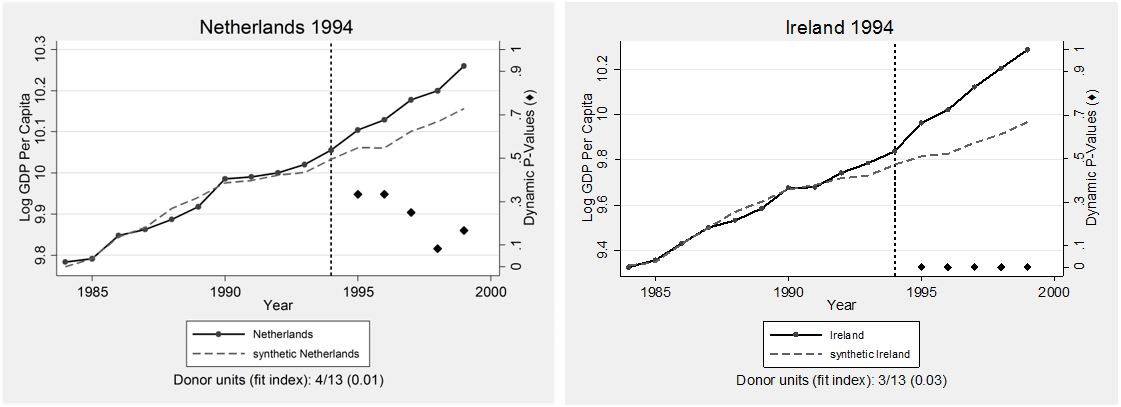

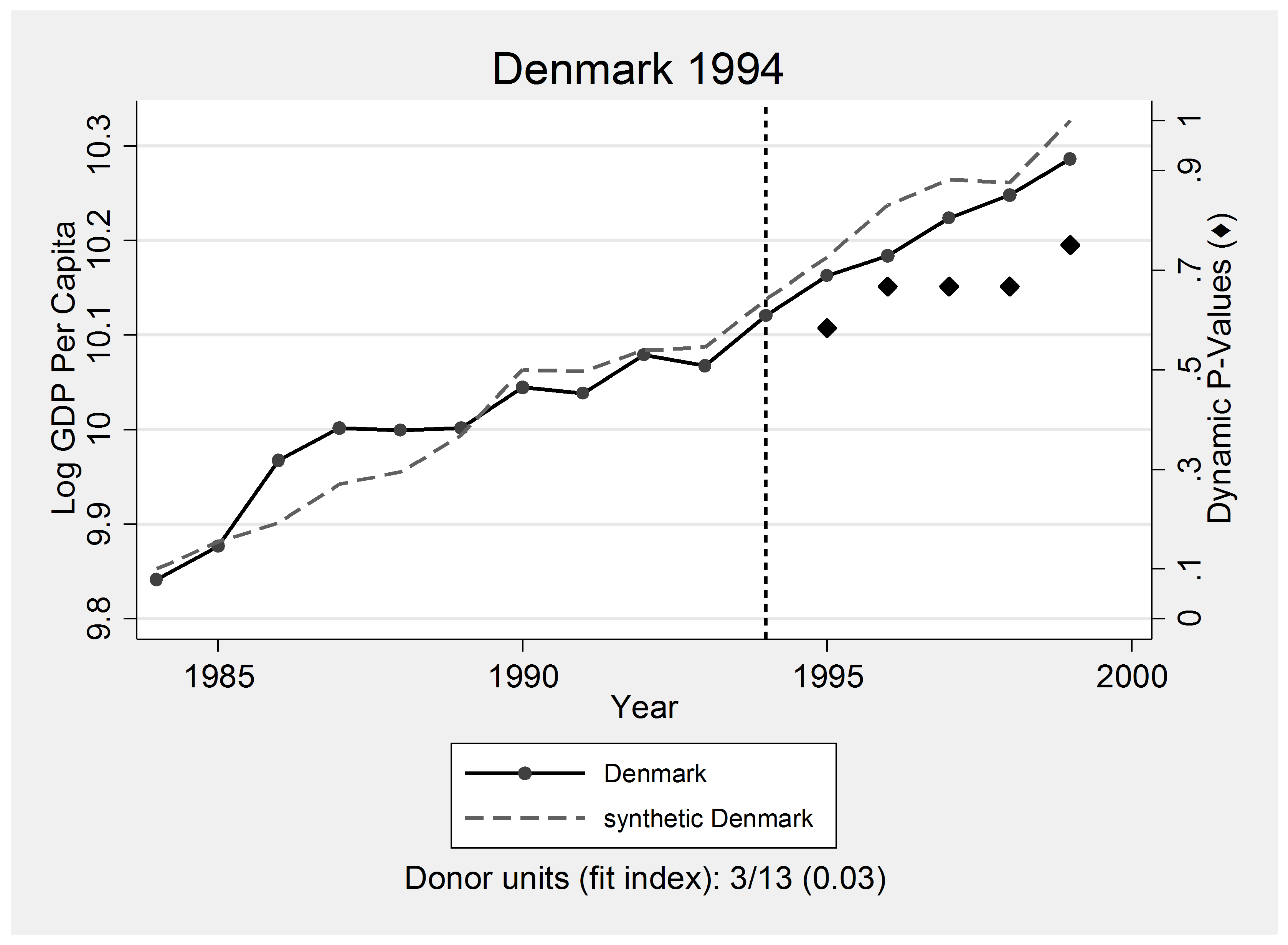

These findings are consistent with those in my forthcoming paper with Bibek Adhikari, Romain Duval, and Bingjie Hu. We use Synthetic Control Method (SCM) and implement six case studies of well-known waves of reforms, those of New Zealand, Australia, Denmark, Ireland and Netherlands in the 1990s, and the labor market reforms in Germany in the early 2000s. Our results suggest a positive but heterogenous effect of reform waves on GDP per capita.

Source: Adhikari, Duval, Hu, and Loungani (2018)

Source: Adhikari, Duval, Hu, and Loungani (2018)

The Bruegel post is available here. Our paper is available here. For those who do not have access, the working paper version is available here.

A new Bruegel post estimates “the impact of large reform waves implemented in the past 40 years worldwide, [and shows] that reforms had a negative but statistically insignificant impact in the short term. […] Reforming countries, however, experienced significant growth acceleration in the medium-term. As a result, 10 years after the reform wave started, GDP per capita was roughly six percentage points higher than the synthetic counterfactual scenario.”

Figure 2. Statistical analysis on the difference between the two

Source: Marrazzo and Terzi (2017)

On the heterogeneity of reform impact,

Posted by at 11:34 AM

Labels: Inclusive Growth

Friday, April 13, 2018

Housing View – April 13, 2018

On cross-country:

- For Home Prices in London, Check the Tokyo Listings – IMF

- Global Investors, House Price Dispersion, and Synchronicity – IMF

- Housing as a Financial Asset – IMF

- The Global Housing Crisis – The Atlantic

- Global Residential Cities Index – Q4 2017 – Knight Frank

On the US:

- Housing Recoveries without Homeowners: A Global Perspective – Federal Reserve Bank of St. Louis

- The Housing Supply Puzzle: Part 1, Divergent Markets – Federal Reserve Bank of St. Louis

- The Housing Supply Puzzle: Part 2, Rental Demand – Federal Reserve Bank of St. Louis

- The Unfulfilled Promise of the Fair Housing Act – The New Yorker

- The Fair Housing Act at 50: Not Sufficiently Powerful to Reverse Residential Racial Segregation – Social Education

- The Fair Housing Act at 50 – Harvard Joint Center for Housing Studies

- VIDEO: Housing Segregation In Everything – NPR

- American Houses Keep Getting Bigger — And so Does American Debt – Mises Institute

- What is holding back housing? – Business Economics

- What Would it Take for Housing Subsidies to Overcome Affordability Barriers to Inclusion in All Neighborhoods? – Harvard Joint Center for Housing Studies

- How Will the New Tax Law Affect Homeowners in High Tax States? It Depends – Federal Reserve Bank of New York

- Have Incomes Kept Up with Rising Rents? – Harvard Joint Center for Housing Studies

- A change to California’s housing supply law could spur a big expansion in home building – Los Angeles Times

- A Small Fix for the Housing Crunch Is in Your Backyard – Bloomberg

Photo by Aliis Sinisalu

On cross-country:

- For Home Prices in London, Check the Tokyo Listings – IMF

- Global Investors, House Price Dispersion, and Synchronicity – IMF

- Housing as a Financial Asset – IMF

- The Global Housing Crisis – The Atlantic

- Global Residential Cities Index – Q4 2017 – Knight Frank

On the US:

- Housing Recoveries without Homeowners: A Global Perspective – Federal Reserve Bank of St.

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, April 10, 2018

Housing as a Financial Asset

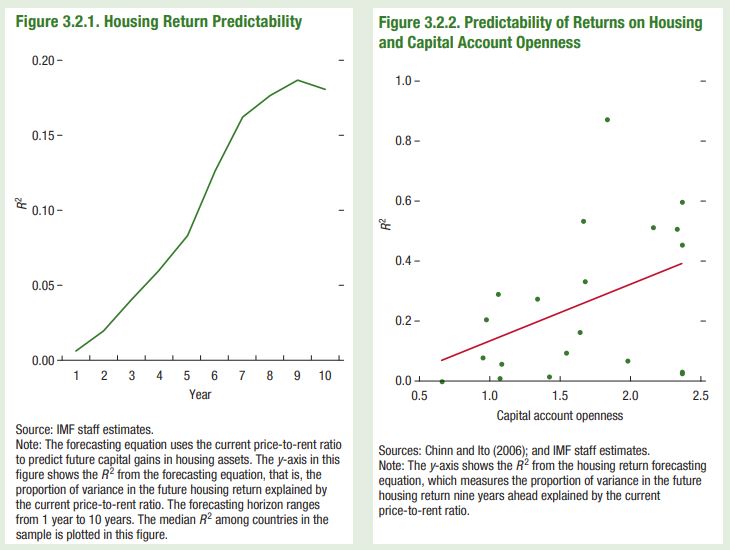

From IMF’s Global Financial Stability Report – April 2018:

“Housing is an important asset class for households and investors. In a typical economy, housing wealth, on average, accounts for roughly one-half of total national wealth and can fluctuate considerably over time (Piketty 2014). Real estate investors often borrow to purchase housing assets, making mortgage payments and receiving rental income and potential capital gains. Publicly traded real estate investment trusts have become available in many countries, allowing investors to invest indirectly in the real estate market. In addition, institutional investors have been increasing their direct exposure to residential real estate in recent years (see Figure 3.3 in the main text).

Investing in housing assets can yield considerable returns in the long term, but is subject to significant variation over time. In many advanced economies, the average annual real return on housing assets between 1950 and 2015 lies between 5 percent and 8 percent,comparable in magnitude to that of equity investment but with a lower standard deviation (Jordà and others 2017). In the shorter term, however, the expected returns on housing assets can vary significantly over time and are affected by the risk appetite of financial market investors as well as other behavioral factors (for example, Cheng, Raina, and Xiong 2014; Brunnermeier and Julliard 2008).”

{kind=link}

Continue reading here.

From IMF’s Global Financial Stability Report – April 2018:

“Housing is an important asset class for households and investors. In a typical economy, housing wealth, on average, accounts for roughly one-half of total national wealth and can fluctuate considerably over time (Piketty 2014). Real estate investors often borrow to purchase housing assets, making mortgage payments and receiving rental income and potential capital gains. Publicly traded real estate investment trusts have become available in many countries,

Posted by at 10:33 AM

Labels: Global Housing Watch

Subscribe to: Posts