Monday, November 28, 2016

Spillovers from the Oil Sector to the Housing Market Cycle

A new paper “assess the spillovers from the oil sector to the housing market cycle using quarterly data for 20 net oil-exporting and -importing industrial countries, and employing continuous- and discrete-time duration models. [The paper does] not uncover a statistically significant difference in the average duration of booms and normal times in the housing markets of those net oil-importers and net oil-exporters. Similarly, the degree of exposure to commodity price fluctuations does not seem to significantly affect the housing market cycle. However, [the authors] find that housing booms are shorter when oil prices increase than housing busts when oil prices decrease. We also show that the net oil-importers are more vulnerable to protracted housing slump episodes than the net-oil exporters.”

Also see another related work on housing and oil prices.

A new paper “assess the spillovers from the oil sector to the housing market cycle using quarterly data for 20 net oil-exporting and -importing industrial countries, and employing continuous- and discrete-time duration models. [The paper does] not uncover a statistically significant difference in the average duration of booms and normal times in the housing markets of those net oil-importers and net oil-exporters. Similarly, the degree of exposure to commodity price fluctuations does not seem to significantly affect the housing market cycle.

Posted by at 2:24 PM

Labels: Global Housing Watch

Housing in Developed and Developing Countries

The 2016 International Housing Association (IHA) Interim Meeting took place on November 1-4, in Durban, South Africa. The meeting brought together housing market experts from different countries to discuss and share information about their respective housing markets. The countries represented at the meeting were: Australia, Canada, Japan, Namibia, Nigeria, Norway, Peru, South Africa, Tanzania, The Gambia, Uganda, United States, Zambia, and Zimbabwe. The presentations focused on country specific situations, and special topics.

Country Specific Presentations

How access to housing finance varied across countries was one of the highlight of the country specific presentations. Several papers and the 2014 IIMB-IMF housing conference have pointed out that access to housing finance is a bit easier in the developed countries compared to developing countries. This finding is consistent with what is reported on the ground. The presentations from developed countries showed single digit mortgage rates (Australia: 4.5%, Canada: 2.5-2.9%, Japan: 0.625-0.750%, Norway: 2.2-3.4%, United States: 3.6%). In contrast the presentations from emerging and developing countries showed double digit mortgage rates except for Peru (Namibia: 11.75%, Peru: 8.7%, South Africa: 10.5%, Tanzania: 19%, The Gambia: 20-23%, Uganda: 22%, Zambia: 22.5%, and Zimbabwe: 12-18%).

A growing housing deficit in emerging and developing countries was also highlighted at the meeting. Most of the representatives from emerging and developing countries reported a housing backlog that is growing. For example, Namibia has a backlog of 110,000 housing units that is growing at annual rate of 3,700 units. Other countries also reported housing deficits: Peru: 1.9 million units, The Gambia: 50,000 units, Uganda: 1.6 million units, Zambia: 1.5 million units, Zimbabwe: 1 million units. In Tanzania, demand for housing is projected at about 200,000 units annually.

Special Topics:

Human settlements, affordable housing, green building, IHA Africa, and a dataset on cross-country housing supply were some of the special topics that were presented. First, there was a presentation that described the fundamental elements of human settlements policy and legislation in South Africa. Second, there was a very fascinating presentation and site visit to the Cornubia Project. This affordable housing project aims at being a multi-billion Rand mixed use, mixed income development incorporating industrial, commercial, residential, and open space use. The overall project area is approximately 1,200ha in extent comprising of mainly agricultural land. Third, Green Building Council of South Africa made a presentation on green building. Green building has started to gain traction and emerging as an important topic.

Fourth, there was a presentation that calls for creating an International Housing Association for Africa or developing countries. One of the ideas is to bring more members from the Africa and developing countries and shed more light on the housing market in this part of the world. Five, there was a presentation on a dataset on housing supply. The presentation focused on showing the trends and patterns in housing construction since the Great Recession across 42 countries.

The 2016 International Housing Association (IHA) Interim Meeting took place on November 1-4, in Durban, South Africa. The meeting brought together housing market experts from different countries to discuss and share information about their respective housing markets. The countries represented at the meeting were: Australia, Canada, Japan, Namibia, Nigeria, Norway, Peru, South Africa, Tanzania, The Gambia, Uganda, United States, Zambia, and Zimbabwe. The presentations focused on country specific situations, and special topics.

Posted by at 1:49 PM

Labels: Global Housing Watch

Tuesday, November 22, 2016

Mexico’s welfare gains from hedging oil-price risk

An IMF paper notes: “Since at least 2001, Mexico’s federal government has hedged the near-term fiscal impact of declines in oil prices through put options. Using a structural model calibrated to the Mexican economy, we quantify the overall benefits of this long-standing policy. Compared to a self-insurance alternative, we find welfare gains from hedging through put options equivalent to a permanent increase in consumption of 0.4 percent. These gains arise mostly from a reduction in sovereign spreads and to a lesser extent from smoothing income volatility. In terms of design, expanding the program to cover domestic fuel sales could yield further gains once gasoline and diesel markets are liberalized. Relying more on liquid instruments—such as options on the Brent—is an avenue worth exploring to ensure the program remains cost effective.”. Read the paper.

An IMF paper notes: “Since at least 2001, Mexico’s federal government has hedged the near-term fiscal impact of declines in oil prices through put options. Using a structural model calibrated to the Mexican economy, we quantify the overall benefits of this long-standing policy. Compared to a self-insurance alternative, we find welfare gains from hedging through put options equivalent to a permanent increase in consumption of 0.4 percent. These gains arise mostly from a reduction in sovereign spreads and to a lesser extent from smoothing income volatility.

Posted by at 4:45 PM

Labels: Energy & Climate Change

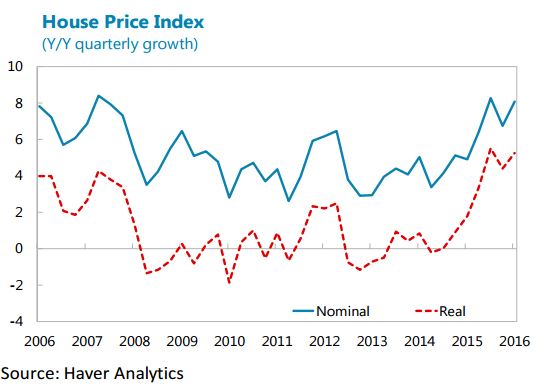

House Prices in Mexico

“House prices have increased broadly in line with income growth on average over the last five years, and there is no evidence of an overvaluation”, says IMF’s new report on Mexico.

“House prices have increased broadly in line with income growth on average over the last five years, and there is no evidence of an overvaluation”, says IMF’s new report on Mexico.

Posted by at 10:57 AM

Labels: Global Housing Watch

Monday, November 21, 2016

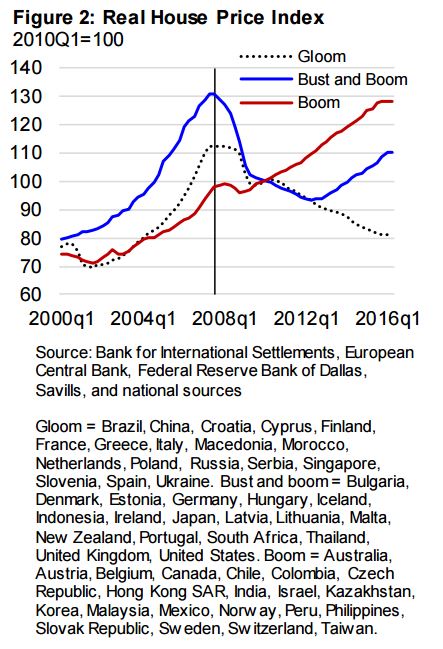

Global Housing Watch Quarterly Update

The IMF’s Global House Price Index—an average of real house prices across countries—is now almost back to its level before the financial crisis. The underlying picture is quite varied. Developments in the countries that make up the index fall into three clusters:

- The first cluster—gloom—consists of 18 economies in which house prices fell substantially at the onset of the Great Recession, and have remained on a downward path.

- The second cluster—bust and boom—consists of 18 economies in which housing markets have rebounded since 2013 after falling sharply during 2007-12.

- The third cluster—boom—comprises 21 economies in which the drop in house prices in 2007–12 was quite modest and was followed by a quick rebound

Read the full report for details and IMF assessments of house price valuations in various countries.

The IMF’s Global House Price Index—an average of real house prices across countries—is now almost back to its level before the financial crisis. The underlying picture is quite varied. Developments in the countries that make up the index fall into three clusters:

- The first cluster—gloom—consists of 18 economies in which house prices fell substantially at the onset of the Great Recession, and have remained on a downward path.

Posted by at 2:55 PM

Labels: Global Housing Watch

Subscribe to: Posts