Tuesday, December 6, 2016

Austerity and Inequality: New Evidence from the IMF

The IMF Economic Review just published a paper that looks into the “distributional consequences of fiscal austerity measures” for 17 OECD countries over the last 30 years. This new paper adds to the stock of IMF papers on the impacts of fiscal consolidation of inequality. Here are links and a cheat sheet to the key papers:

1) Painful Medicine: This (non-wonkish) paper documented that fiscal consolidations not only lower aggregate incomes but have distributional consequences—wage incomes fall more than profits; and the long-term unemployed are affected more than short-term unemployed.

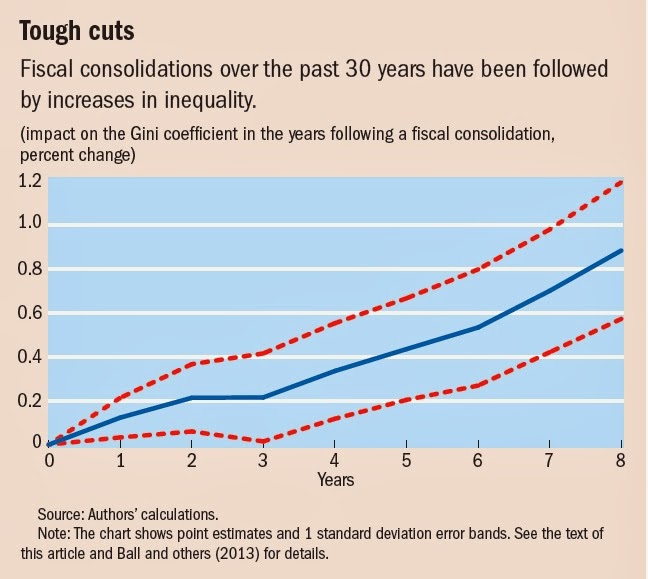

2) The Distributional Effects of Fiscal Consolidation: A wonkish version of the “Painful Medicine” article, with the additional result that, between 1978 and 2009, fiscal consolidations in advanced economies increased the Gini measure on income inequality.

3) Distributional Consequences of Fiscal Consolidation and the Role of Fiscal Policy: In addition to confirming the results in the previous papers, this paper brings in evidence from emerging markets. It also discusses how policies can be designed to mitigate the impacts of fiscal policy on inequality.

4) Who Let the Gini Out?: A (non-wonkish) summary of some of the previous papers.

5) Fiscal Policy and Inequality: A key finding of the paper is that fiscal consolidations during the Great Recession did not lead to increases in inequality.

6) Distributional Consequences of Fiscal Adjustments: What Do the Data Say?: “The paper shows that fiscal adjustments are likely to raise inequality through various channels including their effects on unemployment. Spending-based adjustments tend to worsen inequality more significantly, relative to tax-based adjustments. The composition of austerity measures also matters: progressive taxation and targeted social benefits and subsidies introduced in the context of a broader decline in spending can help offset some of the adverse distributional impact of fiscal adjustments.”

The IMF Economic Review just published a paper that looks into the “distributional consequences of fiscal austerity measures” for 17 OECD countries over the last 30 years. This new paper adds to the stock of IMF papers on the impacts of fiscal consolidation of inequality. Here are links and a cheat sheet to the key papers:

1) Painful Medicine: This (non-wonkish) paper documented that fiscal consolidations not only lower aggregate incomes but have distributional consequences—wage incomes fall more than profits;

Posted by at 10:22 AM

Labels: Inclusive Growth

Sunday, December 4, 2016

European Unemployment: Deja Vu All Over Again?

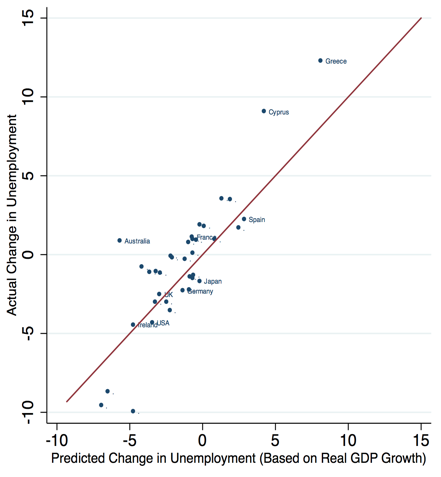

Thirty years ago, a distinguished group of economists advocated a ‘two-handed’ approach to unemployment that targeted supply as much as demand. This column examines recent work on the effectiveness of cyclical and structural policies – the two ‘hands’ – targeting unemployment in Europe. It further considers the pressures from greater integration of capital and labour markets on the success of these reforms. Cyclical measures, particularly the easing of monetary policy, have been successful, but further structural reforms are still needed in many countries where average unemployment remains too high.

Read the rest at Vox.

Figure 1. Actual and predicted changes in unemployment, advanced economies, 2010 to 2015

Notes: The chart compares the actual change in unemployment in each country with what could have been predicted on the basis of the hisotrical relationship between unemployment and output (Okun’s Law).

Thirty years ago, a distinguished group of economists advocated a ‘two-handed’ approach to unemployment that targeted supply as much as demand. This column examines recent work on the effectiveness of cyclical and structural policies – the two ‘hands’ – targeting unemployment in Europe. It further considers the pressures from greater integration of capital and labour markets on the success of these reforms. Cyclical measures, particularly the easing of monetary policy, have been successful, but further structural reforms are still needed in many countries where average unemployment remains too high.

Posted by at 10:45 PM

Labels: Inclusive Growth

Will Interest Rates Stay Low?

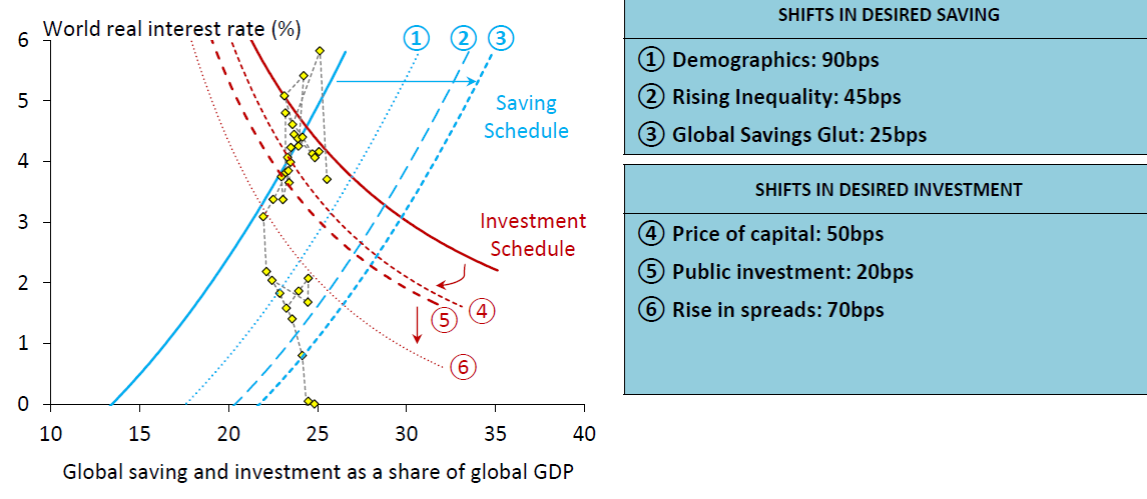

Jim Hamilton offers a characteristically clear summary of a Bank of England paper on the factors affecting global saving and investment and hence global real interest rates. It is a good example of how economists use supply and demand to analyze current developments.

http://econbrowser.com/archives/2016/12/factors-in-low-real-interest-rates

Jim Hamilton offers a characteristically clear summary of a Bank of England paper on the factors affecting global saving and investment and hence global real interest rates. It is a good example of how economists use supply and demand to analyze current developments.

http://econbrowser.com/archives/2016/12/factors-in-low-real-interest-rates

Posted by at 7:02 AM

Labels: Macro Demystified

Wednesday, November 30, 2016

Housing Policies: What Works?

From Global Housing Watch Newsletter: November 2016

The Housing Challenge in Emerging Asia: Options and Solutions is an excellent new book that has just been published by the Asian Development Bank Institute (ADBI). In this issue of the Global Housing Watch Newsletter, Jera Beah H. Lego interviews Matthias Helble, one of the editors of this timely new book. Lego is a Research Associate, and Helble is a Research Economist. Both are at the ADBI.

Jera Beah H. Lego: The urbanization rate in Asia is nearly 50 percent, with more than 2 billion urban dwellers. About 127,000 people flood into cities every day and the number is rising. What are the challenges for policy makers?

Matthias Helble: These numbers mean that the housing stock in urban areas needs to be continuously expanded, and this has huge implications beyond housing. For example, every household needs to have access to clean water, sanitation, and electricity. New dwellings need to be connected to roads and, if possible, public transportation. New neighborhoods should provide access to health care, education, and jobs. Urban safety and crime prevention need to be ensured. Climate change adaptation and mitigation measures also have to be integrated into the planning process.

Jera Beah H. Lego: How have advanced economies confronted the challenge of housing an increasing urban population?

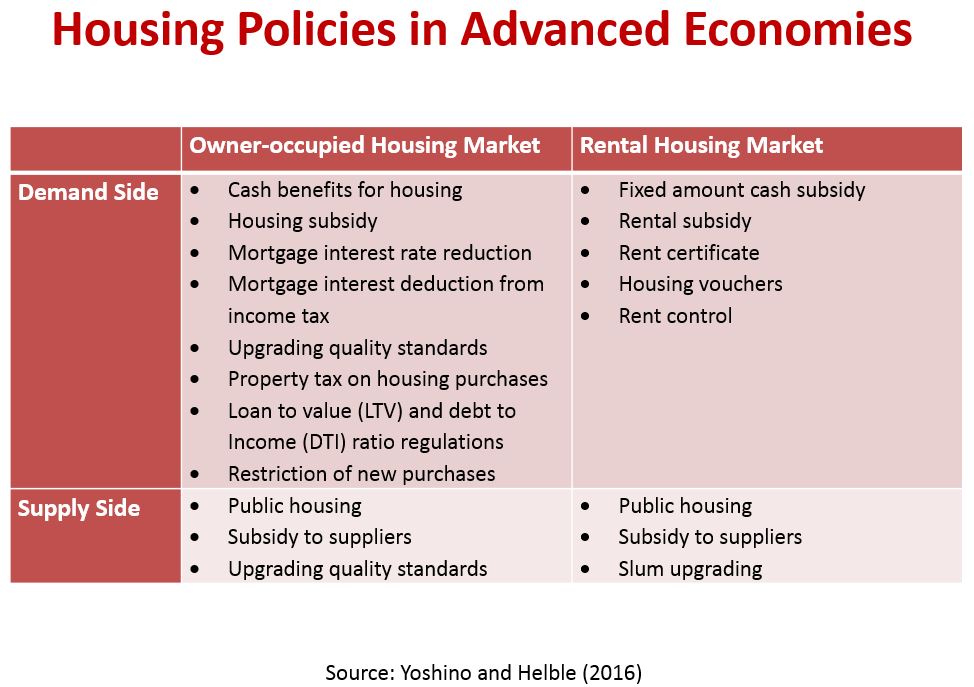

Matthias Helble: They have experimented with policies targeting both the supply and demand side of rental housing and homeownership. On the demand side, they have eased access to homeownership of low-income groups, typically through direct cash transfers or indirect subsidies such as mortgage guarantees. Success, however, has been mixed, as supply often proved to be inelastic. On the supply side, governments have controlled rents. However, rent controls often reduce the supply of rental housing as it becomes a less attractive investment. Consequently, the rental market becomes tighter, with landowners preferring high-income tenants. So even advanced economies struggle to achieve change.

Figure 1

Jera Beah H. Lego: Many parts of the world have housing shortages. Which countries have successfully dealt with them?

Matthias Helble: The public sector has had a major role in providing affordable and adequate housing in many countries. For example, postwar Japan used a three-pillar approach. One, it established the government Housing Loan Corporation to expedite housing construction. Two, it built rental houses for low-income groups. And three, it provided large-scale supply of residential land. Housing stock was restored by the 1960s.

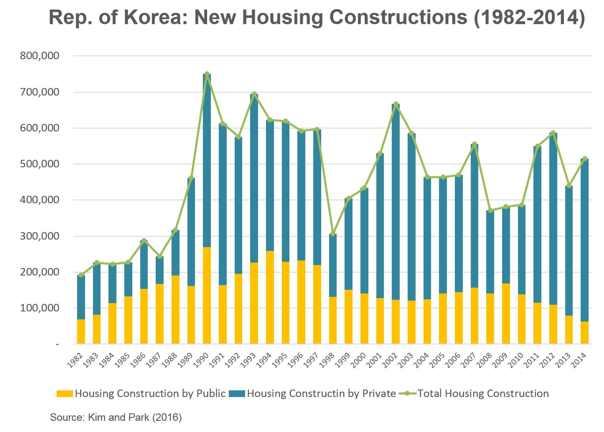

South Korea followed a similar strategy in the 1970s by expanding land supply and providing more housing loans. But government interventions couldn’t meet increased demand and prices went up sharply in the late 1980s. In response, the South Korean government expanded its housing programs with the Two Million Housing Drive and eventually curbed the property prices. Since then, South Korea has been relatively successful in containing price surges and avoiding real estate bubbles.

These policies are based on the idea that the public sector must supply land, the market should be allowed to solve housing problems, and government regulations must ensure that low-income groups can access adequate housing either through rent subsidies or housing finance.

Figure 2

Jera Beah H. Lego: You point out that from the 1950s to the 1970s, supply-side policies were common. Why did many countries switch to demand-side policies in the 1990s?

Matthias Helble: One reason was the belief that the supply side is elastic and will respond to increased demand. However, this did not often occur because the housing market depends crucially on the government to remove supply constraints such as unclear land titles or a shortage of land. Another reason was that demand-side policies are easier to implement. It is often much easier to stimulate demand using various types of subsidies rather than removing supply constraints, which can be administratively and politically costly.

Jera Beah H. Lego: The book points out that there is not enough housing finance available in Asia. Other studies have also pointed out that the mortgage market is small in developing and emerging countries. Why does housing finance remain elusive?

Matthias Helble: Large parts of the population still have limited or no access to financial services. Households that do have access to banking services often don’t know how to use them. Financial inclusion and education are essential. Many commercial banks see housing finance as a risk because they often find it difficult to establish creditworthiness and to foreclose property. Governments have to both ease people’s access to finance and provide an environment that will make commercial banks eager to loan to would-be homeowners.

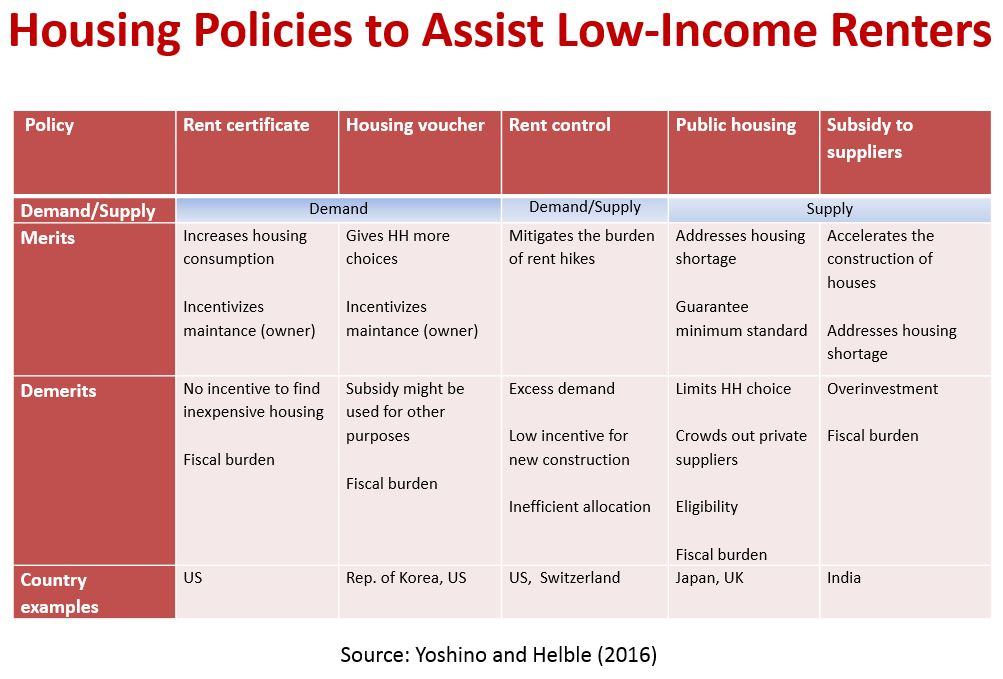

Jera Beah H. Lego: To stimulate housing demand, the US uses mortgage interest deduction while the UK uses the Help-to-Buy scheme. Is it correct to say that very little is done to stimulate the rental housing market? Why?

Matthias Helble: I would not say that very little is done, just relatively little. In both countries, the mantra of homeownership persists, which has advantages such as encouraging accumulation of a physical asset. However, homeownership is expensive, lowers labor mobility, and comes with risks like over-borrowing. Governments should therefore encourage tenure choices such as co-housing and community land trust.

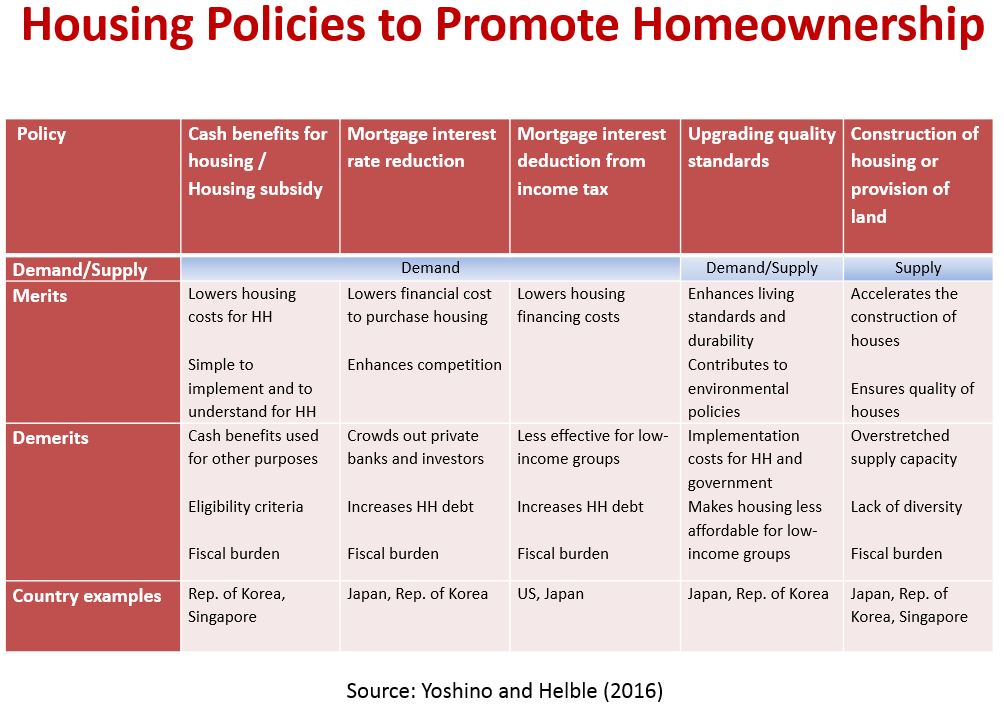

Jera Beah H. Lego: In the book’s case studies, what is the most common policy for promoting homeownership and the rental market?

Matthias Helble: Many countries have experimented with easing mortgage financing, using either direct cash transfers or indirect subsidies like mortgage interest rate reduction. However, mortgage interest reduction in the US shows that a policy aimed at low-income groups can benefit high-income earners instead. In Japan and the UK, the rental market was stimulated by providing public rental housing. Another policy is providing subsidies to suppliers of new housing, as in the case in India.

Figure 3a

Figure 3b

From Global Housing Watch Newsletter: November 2016

The Housing Challenge in Emerging Asia: Options and Solutions is an excellent new book that has just been published by the Asian Development Bank Institute (ADBI). In this issue of the Global Housing Watch Newsletter, Jera Beah H. Lego interviews Matthias Helble, one of the editors of this timely new book. Lego is a Research Associate,

Posted by at 5:00 AM

Labels: Global Housing Watch

Global House Prices: Time to Worry Again?

Our global house price index is almost back to its level before the global financial crisis. Is it time to worry again? Find out my answer in my talk and presentation today at the European Commission.

Our global house price index is almost back to its level before the global financial crisis. Is it time to worry again? Find out my answer in my talk and presentation today at the European Commission.

Posted by at 4:44 AM

Labels: Global Housing Watch

Subscribe to: Posts