Friday, July 10, 2015

Housing Market in France

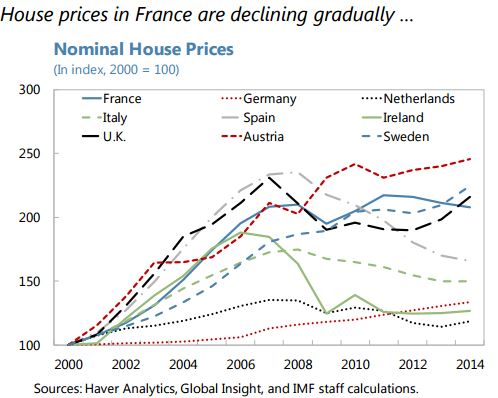

Moreover, the report says that “More could be done to alleviate structural rigidities in the housing market. Residential construction has fallen by 14 percent, and real house prices by 11 percent, since the peak in 2007. While this decline is partly cyclical, a succession of laws introducing regulatory and tax changes may also have contributed. Another long-standing factor affecting the market is the extensive system of housing subsidies, which include rental cash assistance (received by 44 percent of tenants), subsidized mortgage rates for households, and fiscal breaks for providers (including of social housing), together amounting to 1.9 percent of GDP in 2013. While these were aimed at making housing more affordable, studies have found that rental assistance may contribute to rising rents. Staff recommended reviewing the functioning of the housing market, with a view to alleviating constraints on the supply of affordable housing and improving the targeting of benefits.”

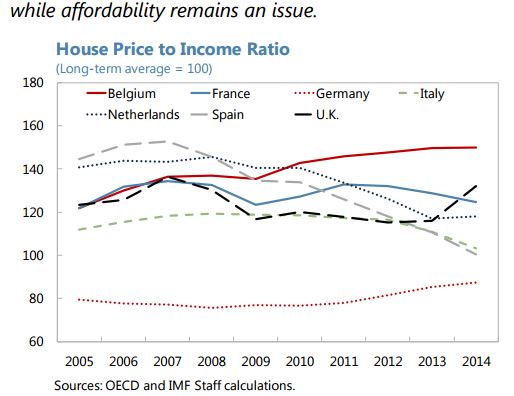

A separate IMF note on the Financial Sector, Housing Prices and Private Balance Sheets notes the following: “House prices have continued to decline gently since their peak in 2011, but affordability metrics remain above long-run averages. House price overvaluation is currently estimated at around 10–15 percent. Nevertheless, household debt appears manageable, at around 10–15 percent.

On the housing market, “they [the French government] do not see risks to financial stability at this point, given prudent lending practices based on repayment ability, the predominance of fixed-rate mortgages, and the mortgage insurance scheme”, according to the new IMF report on France.

Moreover, the report says that “More could be done to alleviate structural rigidities in the housing market. Residential construction has fallen by 14 percent, and real house prices by 11 percent,

Posted by at 6:11 PM

Labels: Global Housing Watch

Tuesday, July 7, 2015

US Housing Market

Also, a separate IMF report on US housing finance notes that “While a number of important steps have been taken to address the structural weaknesses exposed by the crisis in mortgage markets, comprehensive housing finance reform remains the largest piece of unfinished business. In particular, it is not clear when Fannie Mae and Freddie Mac will exit conservatorship and what an end point for a reformed housing finance system will look like. This creates not only fiscal but also financial risks: moral hazard from coverage of credit losses by the government or the government-sponsored enterprises, a distorted competitive landscape due to the dominant footprint of Fannie Mae and Freddie Mac, and large subsidies for homeownership that create incentives to take on excessive levels of household debt.”

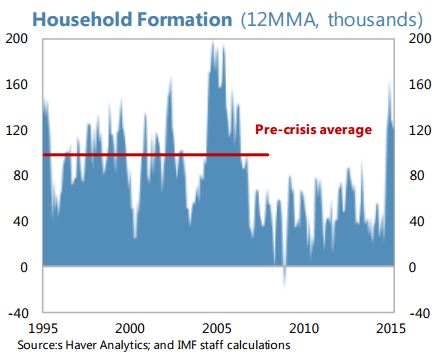

The latest IMF report on the United States points out the following: “Housing market activity has struggled to recover. Up until recently, household formation has been depressed despite the potential for pent-up demand from demographics and more secure job prospects. The slow return of millennials to the first-time home buyers market could signal a preference shift away from traditional suburban, owner-occupied housing. Indeed, the urban rental market remains strong which could represent an enduring increase in demand for multi-family housing units with a smaller square footage. Read the full article…

Posted by at 5:12 PM

Labels: Global Housing Watch

Subscribe to: Posts