The latest IMF

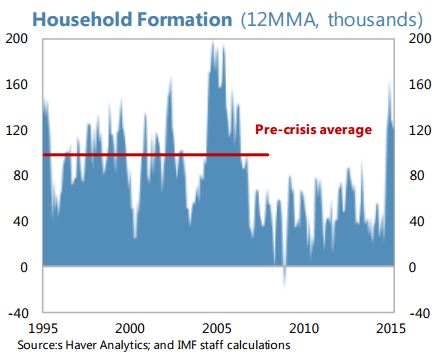

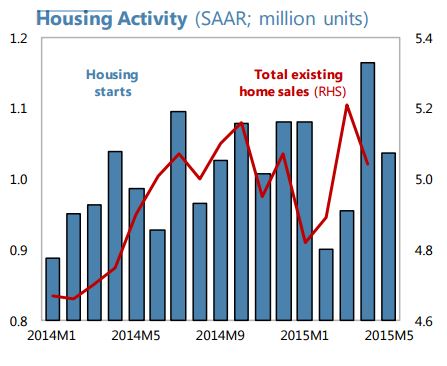

report on the United States points out the following: “Housing market activity has struggled to recover. Up until recently, household formation has been depressed despite the potential for pent-up demand from demographics and more secure job prospects. The slow return of millennials to the first-time home buyers market could signal a preference shift away from traditional suburban, owner-occupied housing. Indeed, the urban rental market remains strong which could represent an enduring increase in demand for multi-family housing units with a smaller square footage. If true, this would permanently lower the steady state growth contribution from residential construction. A less concerning interpretation comes from household surveys, which suggest that attitudes to home ownership haven’t changed much: most renters would prefer to own if they had the necessary financial resources. If that were true, once the job market improves further and millennials have paid off some of their student loans (which have grown to over US$1 trillion or 7½ percent of GDP), the demand for housing could quickly revert to previous norms, with an accompanying step-up in residential investment.”

Also, a separate IMF report on US housing finance notes that “While a number of important steps have been taken to address the structural weaknesses exposed by the crisis in mortgage markets, comprehensive housing finance reform remains the largest piece of unfinished business. In particular, it is not clear when Fannie Mae and Freddie Mac will exit conservatorship and what an end point for a reformed housing finance system will look like. This creates not only fiscal but also financial risks: moral hazard from coverage of credit losses by the government or the government-sponsored enterprises, a distorted competitive landscape due to the dominant footprint of Fannie Mae and Freddie Mac, and large subsidies for homeownership that create incentives to take on excessive levels of household debt.”