Monday, July 20, 2015

LTV and DTI Limits—Going Granular

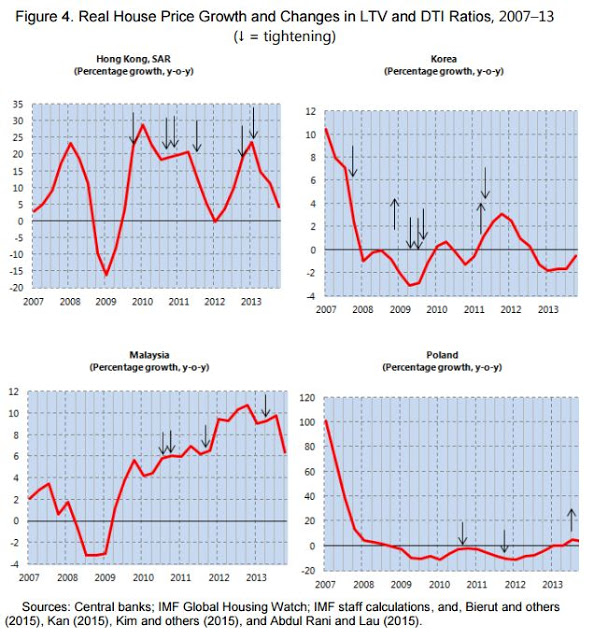

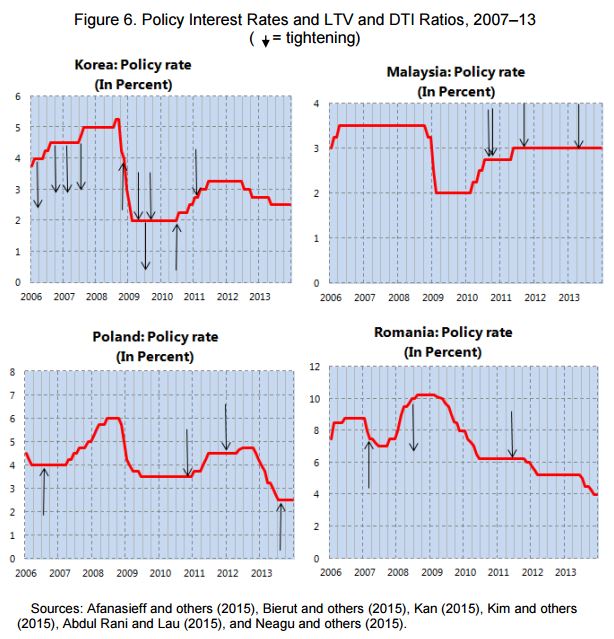

A new IMF paper by Luis I. Jácome and Srobona Mitra looks at how loan-to-value (LTV) and debt-service-to-income (DTI) limits work in practice (Brazil, Hong Kong SAR, Korea, Malaysia, Poland, and Romania). The authors find that “(…) rapid growth in high-LTV loans with long maturities or in the number of borrowers with multiple mortgages can be signs of build up in systemic risk; monitoring nonperforming loans by loan characteristics can help in calibrating changes in the LTV and DTI limits; Read the full article…

Posted by at 6:26 PM

Labels: Global Housing Watch

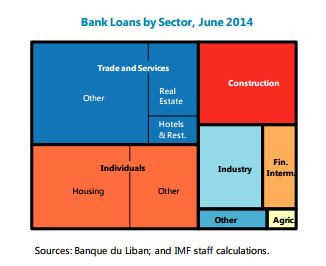

Housing Market in Lebanon

“Risks could arise following a sharper downturn of the real estate market. A sizable fraction of bank loans to the private sector have been directed at the real estate sector, where activity is softening. But, in the absence of a price index, the number and value of property sales can serve as a proxy for the housing cycle. Both indicators grew by close to 3 percent in 2014. This is slightly more than the 2009–14 average for the number of transactions, Read the full article…

Posted by at 6:09 PM

Labels: Global Housing Watch

Friday, July 17, 2015

IMF Staff Paper: Unionization, Minimum Wages and Inequality

“IMF economists have found a decline in unionization—that is, the reduction in the proportion of workers who are union members—and the erosion of minimum wages to be associated with rising inequality in advanced economies. However, these findings do not necessarily constitute a blanket recommendation for higher unionization and minimum wages.” Read the IMF Survey story and the paper.

This work adds to the growing stock of IMF work on inequality. Here’s:

- a guide to previous IMF work on inequality;

- a special feature on Jobs & Inequality,;

- new work on the impact of capital account liberalization on inequality; and,

- the IMF’s work on inequality in China

“IMF economists have found a decline in unionization—that is, the reduction in the proportion of workers who are union members—and the erosion of minimum wages to be associated with rising inequality in advanced economies. However, these findings do not necessarily constitute a blanket recommendation for higher unionization and minimum wages.” Read the IMF Survey story and the paper.

This work adds to the growing stock of IMF work on inequality.

Posted by at 10:03 PM

Labels: Inclusive Growth

Wednesday, July 15, 2015

House Prices in Germany

“The moderate upward trend in housing prices continues and the appropriate response at this stage is close monitoring and readying the macroprudential toolkit. After years of stagnation, nominal housing prices at the aggregate level have grown at an annual pace of 3–4 percent for the past five years—only marginally faster than the growth in disposable income. In spite of falling lending rates, mortgage loan growth remains modest and lending standards appear stable. Thus, there are no signs of overheating yet. Read the full article…

Posted by at 6:52 PM

Labels: Global Housing Watch

Tuesday, July 14, 2015

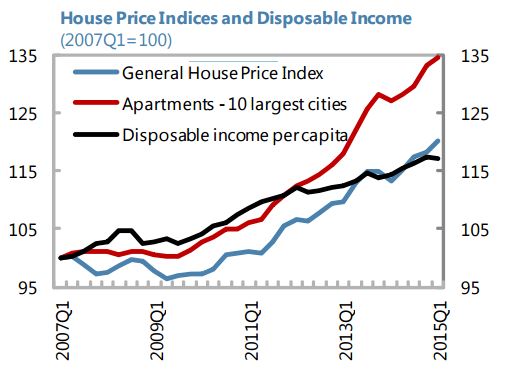

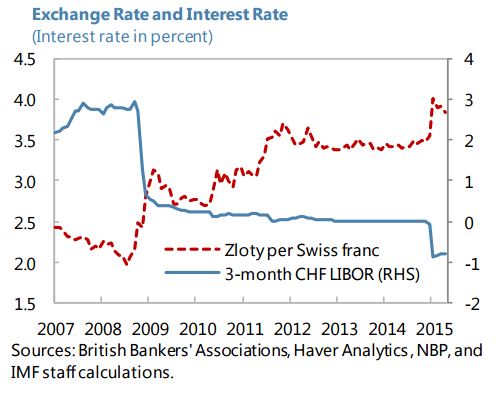

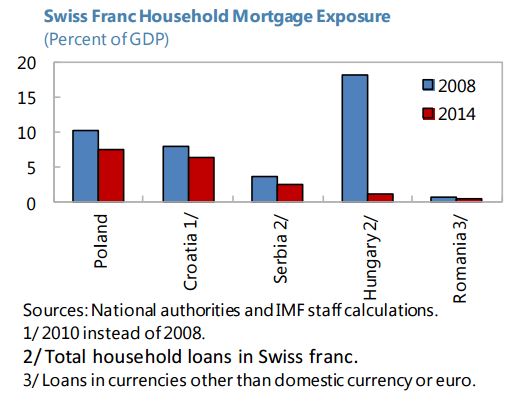

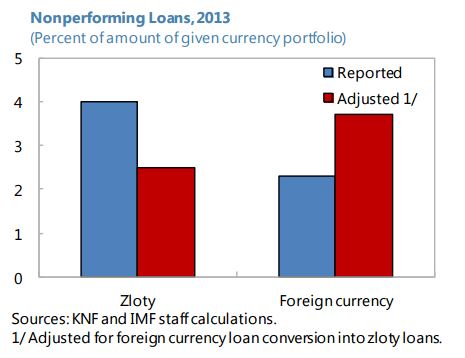

Housing Market in Poland

On foreign-currency mortgages, the new IMF report on Poland says that “While tighter prudential regulation has halted new FX lending, a substantial legacy stock of these loans remains. Close to half of mortgages are denominated in FX (mostly Swiss franc), exposing households and banks to sudden zloty depreciation—as was the case in January when the zloty depreciated around 20 percent against the Swiss franc. As such, the January episode had little macroeconomic impact and high capital buffers in banks mitigated financial stability risks. Read the full article…

Posted by at 6:52 PM

Labels: Global Housing Watch

Subscribe to: Posts