Friday, March 13, 2015

House Prices in Iceland

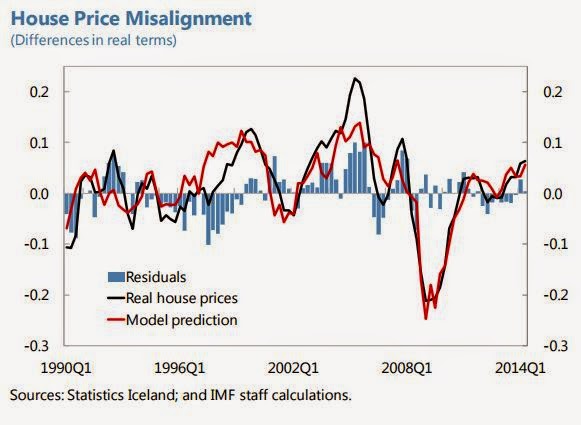

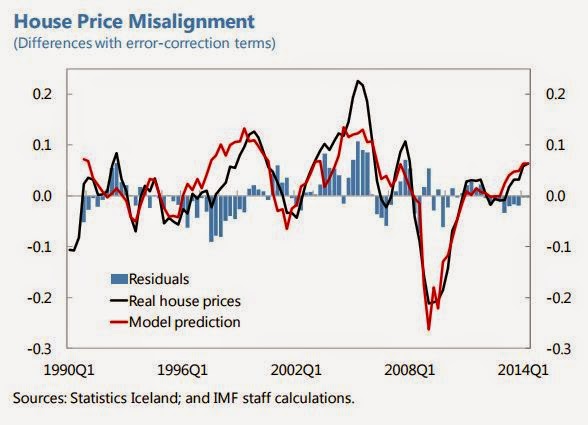

bubbles. House prices in Iceland have been rising rapidly in the recent period, prompting

concerns about possible overvaluation. Based on a cross-country comparison, time-series

analysis, and correlation analysis, house prices in Iceland do not stand out as particularly

misaligned. To formally test whether the housing market is overvalued, we employ the

Igan and Loungani (2012) model based on housing affordability, per capita income,

population, stock prices, credit, and interest rates. We find that there are currently no

misalignments between house prices and the fundamentals, which is consistent with the

recent analysis conducted by the CBI. However, housing supply-side constraints remain

significant, with new starts well below the historic norm. These, together with the ongoing

recovery in mortgage lending, the wealth and income effects of household debt relief and

Pillar III withdrawals to fund debt relief (and, until discontinued in 2015 budget, for

general consumption), increasing demand for vacation properties, and potentially large

wage hikes in the near-term, may lead to an overshooting of house prices. Policies that

could be explored (while keeping an eye on broader macroeconomic considerations) to

help minimize the risks of asset price bubbles in the housing sector include steps to: (i)

support measured increases in housing supply; (ii) maintain non-inflationary growth in

wages; (iii) prevent excessive leveraging; and (iv) increase household savings.”

A new IMF paper on asset price bubbles says that “One of the potential costs of prolonged capital controls is the formation of asset price

bubbles. House prices in Iceland have been rising rapidly in the recent period, prompting

concerns about possible overvaluation. Based on a cross-country comparison, time-series

analysis, and correlation analysis, house prices in Iceland do not stand out as particularly

misaligned. To formally test whether the housing market is overvalued, Read the full article…

Posted by at 5:29 PM

Labels: Global Housing Watch

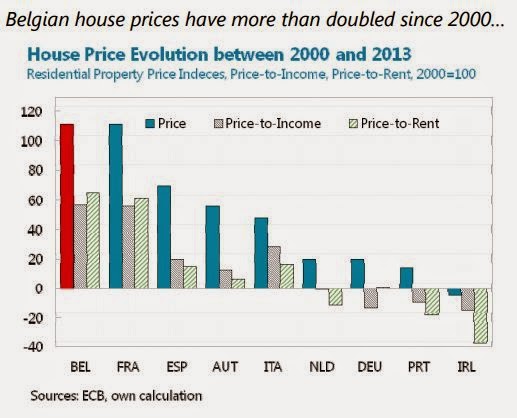

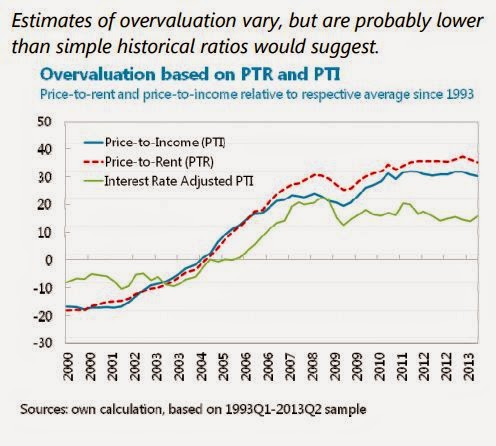

House Prices in Belgium

Moreover, the paper says that “there is a continued need for vigilance and policy coordination. Recent changes in macro-prudential and fiscal policy seem appropriate to make the housing market safer and reduce untargeted fiscal expenditures. To assure that the price adjustment remains orderly and does not lead to overshooting, future policy changes should be gradual and coordinated among different institutions. A well communicated housing strategy could help to avoid price mis-alignments in the future.”

A new IMF paper “(…) argues that current house prices are closer to their equilibrium than simple historical ratios would suggest and that given the moderate overvaluation, a gradual and limited adjustment seems a plausible scenario. Strong household balance sheets, a seemingly well-managed mortgage market and various institutional characteristics reduce the risk of an abrupt correction. Given that historical house price changes have had moderate macro-economic effects – with the exception of residential investment – the repercussions of a gradual decline seem manageable.” Read the full article…

Posted by at 2:32 PM

Labels: Global Housing Watch

Wednesday, March 4, 2015

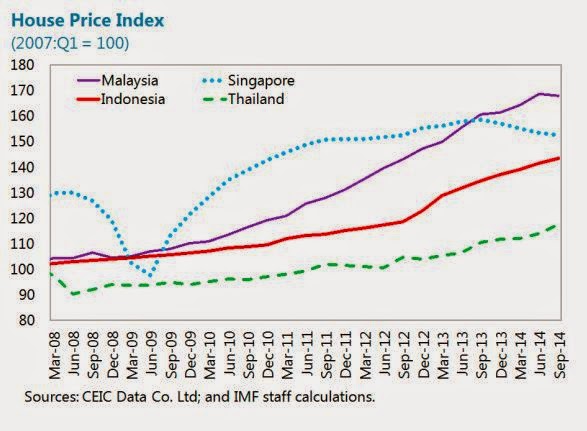

House Prices in Malaysia

“Although there are signs of cooling in the housing market and personal lending growth has been curtailed, financial vulnerabilities remain due to high household debt and elevated house prices,” according to the new IMF report on Malaysia. Specifically, it says “House prices have risen steadily (…) outpacing incomes and rents. Although population growth is strong this cannot fully explain the increase in house prices compared with other countries. However, there are tentative signs of cooling in the housing market in Kuala Lumpur. Read the full article…

Posted by at 3:05 PM

Labels: Global Housing Watch

House Prices in Malta

“After a period of downward correction in 2008-09, Malta’s housing market seems to have stabilized,” notes the latest IMF report on Malta. However, the report says that “One of the main risks facing core domestic banks relates to their exposure to the real estate sector. Around two thirds of loans extended by banks are secured with real estate collateral, and mortgages are one of the few segments of bank loans which have been increasing recently (unlike loans to NFCs). Read the full article…

Posted by at 2:58 PM

Labels: Global Housing Watch

Subscribe to: Posts