Friday, March 4, 2022

Short in Supply!

Source: Project Syndicate

In a recent column, John H. Cochrane of the Hoover Institution and Jon Hartley of Foundation for Research on Equal Opportunity write about the US’ long-ignored issue of supply-chain bottlenecks contributing to raging inflation today.

“The return of inflation is an economic cold shower”

They write how sclerotic growth in the country is not so much due to the “secular stagnation” of demand-side factors, but more due to clogging of the economy’s productive capacity. “The United States needs infrastructure. The problem is not money. The problem is that building anything in America has become almost impossible, owing to the thicket of regulations and lawsuits that will stop or drive up the costs of any project.” Barriers such as rocketing housing costs, deteriorating quality of public education, restrictive labor laws, trade protectionism, and other things all add to the problem. The authors also discuss some solutions to systematically eliminate such challenges.

Source: Project Syndicate

In a recent column, John H. Cochrane of the Hoover Institution and Jon Hartley of Foundation for Research on Equal Opportunity write about the US’ long-ignored issue of supply-chain bottlenecks contributing to raging inflation today.

“The return of inflation is an economic cold shower”

They write how sclerotic growth in the country is not so much due to the “secular stagnation” of demand-side factors,

Posted by at 10:32 AM

Labels: Inclusive Growth, Macro Demystified

Saturday, January 15, 2022

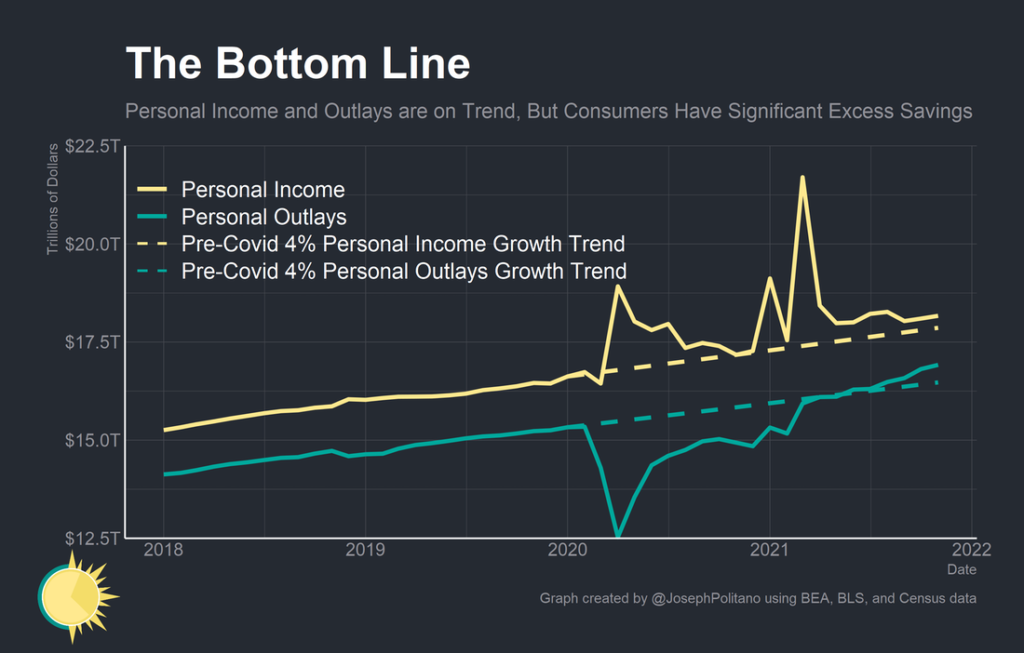

The Inflation Outlook

As described by the tagline of this blog post, it dives deeper into CPI figures for the USA for December 2021 and then discusses their implications. CPI rose by 7 percent year on year in December and 0.5 percent since November 2021, although the rise in demand causing it wasn’t all uniform. The pattern of uneven growth of consumer expenditure on manufactured goods and durables rather than services has been discussed in greater detail, besides issues like inhouse oil production in the US which also exert some influence on the general price level.

Looking ahead, it elaborates upon visible signs that signal a quickly abating inflation using measures like wage growth, prevailing inflation expectations in the market, and the state of aggregate spending in the economy.

Click here to read the full blog.

As described by the tagline of this blog post, it dives deeper into CPI figures for the USA for December 2021 and then discusses their implications. CPI rose by 7 percent year on year in December and 0.5 percent since November 2021, although the rise in demand causing it wasn’t all uniform. The pattern of uneven growth of consumer expenditure on manufactured goods and durables rather than services has been discussed in greater detail, besides issues like inhouse oil production in the US which also exert some influence on the general price level.

Posted by at 9:08 AM

Labels: Macro Demystified

Thursday, January 13, 2022

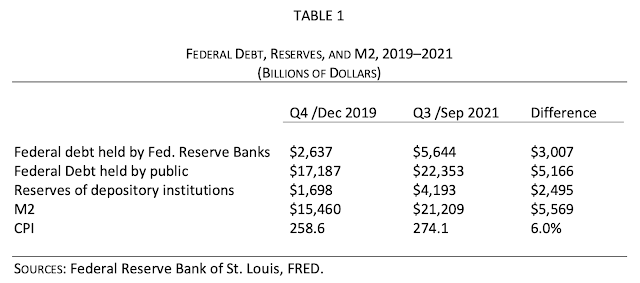

Fiscal Inflation

In his blog, The Grumpy Economist, John H. Cochrane, Senior Fellow at Stanford University’s Hoover Institution writes about the role of fiscal policy in pushing inflation.

“Starting in March 2020, in response to the disruptions of Covid-19, the U.S. government created about $3 trillion of new bank reserves, equivalent to cash, and sent checks to people and businesses. (Mechanically, the Treasury issued $3 trillion of new debt, which the Fed quickly bought in return for $3 trillion of new reserves. The Treasury sent out checks, transferring the reserves to people’s banks. See Table 1.) The Treasury then borrowed another $2 trillion or so, and sent more checks. Overall federal debt rose nearly 30 percent. Is it at all a surprise that a year later inflation breaks out? It is hard to ask for a clearer demonstration of fiscal inflation, an immense fiscal helicopter drop, exhibit A for the fiscal theory of the price level (Cochrane 2022a, 2022b).”

Click here to read the full blog.

Related Reading:

In his blog, The Grumpy Economist, John H. Cochrane, Senior Fellow at Stanford University’s Hoover Institution writes about the role of fiscal policy in pushing inflation.

“Starting in March 2020, in response to the disruptions of Covid-19, the U.S. government created about $3 trillion of new bank reserves, equivalent to cash, and sent checks to people and businesses. (Mechanically, the Treasury issued $3 trillion of new debt, which the Fed quickly bought in return for $3 trillion of new reserves.

Posted by at 8:53 AM

Labels: Macro Demystified

Tuesday, January 4, 2022

Rising Inflation and the Cause for Concern

In a piece for the VoxEU CEPR blog, Professors Francesco D’ Acunto of Boston College and Michael Weber of Booth School of Business, University of Chicago write about rising inflation in the times of Covid-19 pandemic, and why it may be worrisome for reasons even beyond those that we think most about. Aside from the three channels that have been discussed often (pent-up demand pressures, supply constraints, and labor shortages), they bring into focus the self-fulfilling nature of consumers’ expectations of prices that impacts inflation rates.

The natural question then is why should policymakers be concerned about households’ expectations of price levels anyway.

“The concern is that a surge in inflation expectations might become self-fulfilling. Recent research uses microdata to document that higher inflation expectations often result in higher consumer spending before prices increase. Further demand pressure given the post-COVID supply bottlenecks would push inflation even higher.” They further go on to add, “households might also demand higher wages to keep their perceived purchasing power constant based on their elevated inflation expectations.”

Click here to read the full article.

In a piece for the VoxEU CEPR blog, Professors Francesco D’ Acunto of Boston College and Michael Weber of Booth School of Business, University of Chicago write about rising inflation in the times of Covid-19 pandemic, and why it may be worrisome for reasons even beyond those that we think most about. Aside from the three channels that have been discussed often (pent-up demand pressures, supply constraints, and labor shortages), they bring into focus the self-fulfilling nature of consumers’

Posted by at 9:52 AM

Labels: Macro Demystified

Thursday, December 30, 2021

Measuring US Core Inflation: The Stress Test of COVID-19

Laurence M. Ball of the Johns Hopkins University, and Daniel Leigh, Prachi Mishra, and Antonio Spilimbergo of the International Monetary Fund write about the core inflation rate in the US in a paper for the National Bureau of Economic Research (NBER).

Abstract:

“Large price changes in industries affected by the COVID-19 pandemic have caused erratic fluctuations in the U.S. headline inflation rate. This paper compares alternative approaches to filtering out the transitory effects of these industry price changes and measuring the underlying or core level of inflation over 2020-2021. The Federal Reserve’s preferred measure of core, the inflation rate excluding food and energy prices, has performed poorly: over most of 2020-21, it is almost as volatile as headline inflation. Measures of core that exclude a fixed set of additional industries, such as the Atlanta Fed’s sticky-price inflation rate, have been less volatile, but the least volatile have been measures that filter out large price changes in any industry, such as the Cleveland Fed’s median inflation rate and the Dallas Fed’s trimmed mean inflation rate. These core measures have followed smooth paths, drifting down when the economy was weak in 2020 and then rising as the economy has rebounded.”

Click here to read the full paper.

Laurence M. Ball of the Johns Hopkins University, and Daniel Leigh, Prachi Mishra, and Antonio Spilimbergo of the International Monetary Fund write about the core inflation rate in the US in a paper for the National Bureau of Economic Research (NBER).

Abstract:

“Large price changes in industries affected by the COVID-19 pandemic have caused erratic fluctuations in the U.S. headline inflation rate. This paper compares alternative approaches to filtering out the transitory effects of these industry price changes and measuring the underlying or core level of inflation over 2020-2021.

Posted by at 9:41 AM

Labels: Macro Demystified

Subscribe to: Posts