Thursday, February 2, 2012

House Prices in Norway

IMF staff report says:

- Over the last two years Norway has seen one of the most rapid paces of real house price appreciation in the OECD.

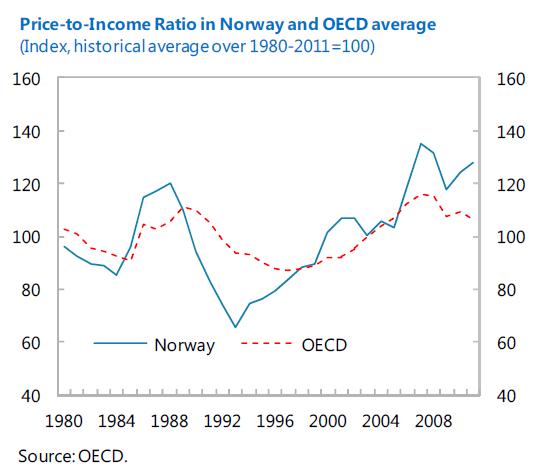

- Housing valuations continue to appear on the high side. Standard metrics, such as price-to-rent and price-to-income ratios, indicate a risk of overvaluation.

- The ratio of house prices to rents has risen sharply during the boom and is now nearly 70 percent above its historical average—the highest such deviation in any OECD country.

- The house price-to-income ratio has also been rising. This ratio is now 28 percent above its historical average—higher than the peak reached before the last major house price bust in Norway two decades ago.

- While fundamentals explain part of the boom, signs also point to risks of overvaluation. On balance, model based estimates from the IMF’s Early Warning Exercise (EWE), which take into account the key determinants of house prices, suggest that Norwegian residential property prices may be misaligned by 15-20 percent. However, there is admittedly a high amount of uncertainty around this estimate in both directions.

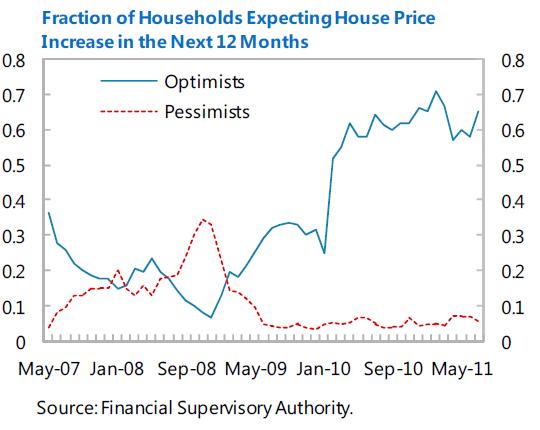

- Expectations of increasing prices may lead agents to buy for speculative motives. An increasing number of households believe that property prices will continue to appreciate. (…) Today, 70 percent of the survey respondents expect price to increase over the next 12 months.

- Another candidate for explaining the boom is loose credit conditions. (…) the share of mortgages with loan-to-value (LTV) ratios over 90 percent has been high since data were first collected in the late 1990s, after the boom was already underway. However, it is somewhat worrisome that the share of mortgages with LTVs over 90 percent has increased since 2010, despite the issuance of FSA guidelines recommending against allowing LTVs to exceed this level, other than in exceptional circumstances.

- About 95 percent of mortgages loans are adjustable-rate and interest payments are front-loaded, low interest rates have made mortgages cheaper and homes significantly more affordable.

- Total household mortgage debt as a fraction of disposable income has increased to 195 percent by end-2010.

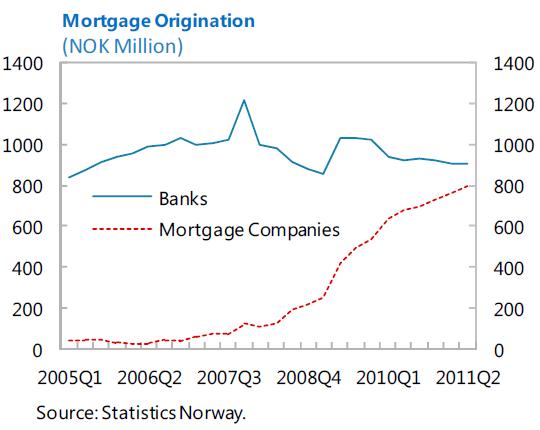

- The volume of secured loans issued by mortgage companies has picked up considerably since 2008. In 2011, loans from mortgage companies represented nearly 50 percent of new mortgages.

- Owner-occupied housing receives quite generous tax treatment in Norway.

- A house price bust would likely be associated with depressed economic activity and increased financial sector stress, especially given high levels of mortgage debt.

- The estimates suggest that a 10 per cent drop in real house prices in Norway is associated with roughly 1 percentage point lower GDP growth than otherwise. (…) A correction of 30 percent in house prices—as occurred during the crisis in the 90s—would exert a non-negligible effect to the real economy.

IMF staff report says:

- Over the last two years Norway has seen one of the most rapid paces of real house price appreciation in the OECD.

- Housing valuations continue to appear on the high side. Standard metrics, such as price-to-rent and price-to-income ratios, indicate a risk of overvaluation.

- The ratio of house prices to rents has risen sharply during the boom and is now nearly 70 percent above its historical average—the highest such deviation in any OECD country.

Posted by at 3:36 PM

Labels: Global Housing Watch

Wednesday, February 1, 2012

Do Groundhogs make Better Forecasters than Economists?

Feb. 2 is Groundhog Day. Legend has it that if the groundhog—Punxsutawney Phil—casts a shadow that day, six weeks of winter lie ahead. No shadow and the forecast is for an early spring. Statistical records suggest the groundhog has been right about 40% of the time. Are we headed for economic spring or winter? If past performance is any guide, we might be better off asking groundhogs than economists.

A dismal record

In 2000, I wrote in the Financial Times that “the record of failure to predict recessions is virtually unblemished.” A dozen years and many recessions later, there is little reason to change my assessment.

My initial conclusion was based on my findings that only two of the 60 recessions that occurred around the world during the 1990s were predicted by private sector forecasters a year in advance. About 40 of the 60 recessions remained undetected seven months before they occurred. As even as late as two months before each recession began, about a quarter of the forecasts still predicted positive growth for the country concerned.

With my colleagues Jair Rodriguez and Hites Ahir, I’ve since looked at the record of forecasting recessions over the decade of the 2000s and during the Great Recession of 2007-09.

Let’s consider the 2000s first and restrict attention to forecasts for twelve large economies—the G7 plus the ‘E7’ (emerging market economies–Brazil, China, India, Korea, Mexico, Russia and Turkey), which together account for over three-quarters of world GDP.

There were a total of 26 recessions in this set of countries. Only two recessions were predicted a year in advance and one of those predictions came toward the turn of the year. Requiring recessions to be predicted a year ahead may seem like an unreasonably high bar to set.

Lowering the bar to the start of the year in which the recession occurred does indeed improve the performance somewhat: 8 of the 26 recessions were predicted in February of the year in which they occurred and 16 were predicted by August. But even as the year drew to a close, 6 of 26 recessions remained undetected by forecasters.

Moreover, while forecasters increasingly started to recognize recessions in the year in which they occurred, the magnitude of the recession was underpredicted in the vast majority of cases. For instance, even as late as December of the year of the recession, the forecast was more optimistic than the outcome in 15 cases.

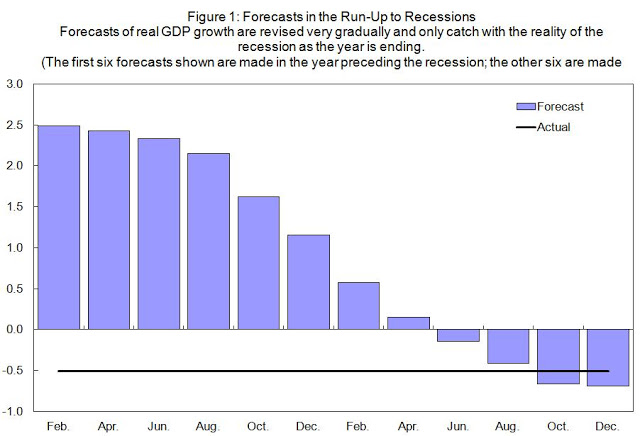

Figure 1 shows the evolution of forecasts on average across the 26 episodes. The forecast in February of the year before was for about 2.5% growth. This forecast was slowly lowered over the course of the year and by the start of the year of the recession the average forecast was for a small decline in real GDP. It was only as the year was drawing to a close that the average forecast caught up with the reality of the recession.

The impression one gets is of forecasts chasing the data rather than staying a step ahead of it.

The forecasting performance at the onset of the Great Recession was no better. Looking at forecasts for over 80 countries, it turns out that none of the nine recessions that started in 2008 was predicted a year in advance. Even by April 2008, none of the nine recessions were predicted and by October 2008, only four were.

Official sector forecasts?

If private sector growth forecasts are of little use in spotting recessions, why not use the forecasts made by the official sector? The IMF, the World Bank and the OECD all provide economic forecasts for free.

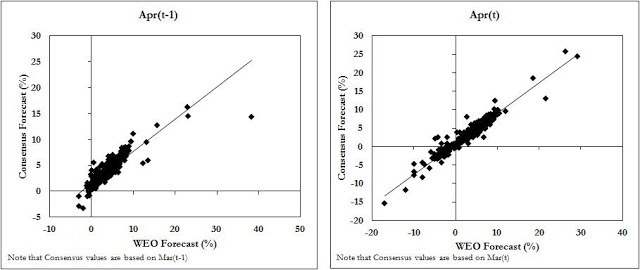

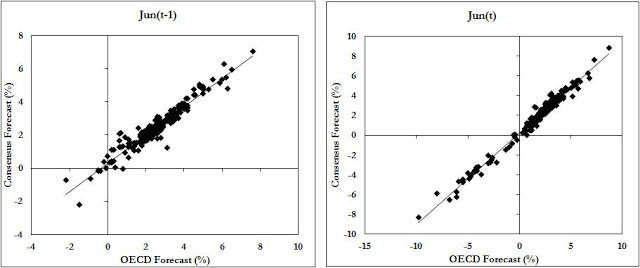

Yet there is not much to choose between private sector and official sector forecasts. Statistical “horse races” between the two tend to end up in a photo-finish in most cases. As just one example of this, look at Figure 2 above which compares private sector (consensus) forecasts vs. the IMF’s World Economic Outlook and the OECD’s forecasts. It is evident from these charts that there is little daylight between private sector forecasts and official sector forecasts: the forecasts have a correlation of over 0.9.

This finding casts new light on claims sometimes made that the growth projections of international organizations tend to be over-optimistic. Since the private sector is not subject to the same pressures, it is puzzling that its forecasts end up so close to those of international organizations. At the same time, the pressures acting on private forecasters to lead them towards over-optimism are not faced by forecasters in international organizations.

One possible explanation for the similarity of the predictions is that private and official sector forecasters feed on each other and—in many countries—are heavily reliant on government forecasts. Exuberance on the part of governments may affect both private sector forecasts and those of international organizations.

Buyer beware

The failure to predict recessions does not mean that forecasts of economic growth have no value. But it does suggest that users of forecasts might be better served by paying greater attention to the description of the outlook and the associated risks than to just the central forecast itself.

Reassuringly, it is becoming more common to show how much uncertainty there is about whether the central forecast will come true. It is particularly useful to be explicit about the downside risks to a growth forecast as it can provide a wake-up call for policies and actions needed to keep those risks from materializing.

Feb. 2 is Groundhog Day. Legend has it that if the groundhog—Punxsutawney Phil—casts a shadow that day, six weeks of winter lie ahead. No shadow and the forecast is for an early spring. Statistical records suggest the groundhog has been right about 40% of the time. Are we headed for economic spring or winter? If past performance is any guide, we might be better off asking groundhogs than economists.

A dismal record

Posted by at 8:03 PM

Labels: Forecasting Forum

Tuesday, January 31, 2012

Tom Sargent on European and U.S. Economic Woes—and History

Thomas Sargent, winner of the 2011 Nobel Prize in Economic Science, has made several visits over the past year to the IMF’s Research Department. Last week, he talked to Prakash Loungani about problems ailing Europe and the United States—and what each could learn from the other’s history.

|

| Photo: Stephen Jaffe/IMF |

Loungani: Europe’s fiscal challenges are foremost on minds here. This is something you have worked on in the past—the interplay of monetary and fiscal policy.

Sargent: Yes. I think Europe can learn from the U.S history. In the 1780s, the U.S. consisted of 13 sovereign states and a weak center. The states could levy taxes, the federal government could not. Government debt, federal plus state, was 40 percent of GDP, very high for a poor country. It was a crisis. Creditors worried that they could not be repaid.

Loungani: How was it resolved? There wasn’t an IMF …

Sargent: Well, in the end the outcome was that the U.S. founding fathers rewrote the constitution so that it gave better protection to creditors. The constitution reflected a grand bargain: the central government bailed out the states, and the states gave up the power to levy tariffs. Knowing that the federal government had the power to raise tax revenues gave creditors reassurance that their debts would be repaid.

A fiscal union

Loungani: You’re saying the present U.S. constitution was adopted to give better protection to creditors?

Sargent: Yeah, makes me sound like a Marxist, doesn’t it? But it’s all there in our history. Alexander Hamilton was basically creating a fiscal union—bailing out the states in return for a transfer of tax-levying authority to the center. And the point of a fiscal union was to change the expectations of creditors about the chances of being repaid now and in the future. Note, by the way, that the U.S. had a fiscal union before it had a monetary union.

Loungani: So what are the lessons for Europe today?

Sargent: Don’t some aspects of the EU today remind you of the historical experience I’ve described? The member states have the power to tax, not the center. Many EU-wide fiscal actions require unanimous consent by member states. But reforms that could lead to a fiscal union are being proposed, as they were in the U.S. in the 1780s. I think at the very least the historical episode—not just the one I described but several others that I could—shows that many configurations of fiscal and monetary arrangements are possible, and some of these work to provide assurance to creditors that there will be enough tax revenues to service the debt. I offer this as hope, but I must say that I am not an expert on day-to-day European economics or on their politics.

Curing U.S. unemployment

Loungani: You are an expert on the U.S., and particularly on unemployment, which you’ve also worked on over the years. What would you do about the high U.S. unemployment rate?

Sargent: I would deal with the fundamental causes of financial crisis—the housing market particularly, where there are debts that haven’t been settled and people can’t yet see how they will be settled. And then to the extent that uncertainty about the course of government regulations is holding things back, I’d tackle that.

Loungani: That could take time. How would you ease the pain of the unemployed in the meantime?

Sargent: Some of the European countries, Germany and the U.K., have the right idea. They seem to do better on what’s called welfare-to-work programs—ways of helping the unemployed get into new jobs. We could have done more of that here in the U.S.

Loungani: We extended unemployment benefits many times. Were you in favor of that?

Sargent: I worry that can be a trap—we could end up with persistently high unemployment.

Loungani: Why?

Sargent: You have to go back to the basic ideas in the work that I’ve done with colleagues over the years. Our work builds on the finding that after about 1980 something changed. The [adverse] hits that people suffered to their incomes became more permanent in nature. In the jargon of our profession, the volatility in the permanent component of earnings increased; workers were more likely to suffer permanent shocks to their human capital. Tom Friedman’s The World is Flat has many examples of all this and the reasons why it happened. So we talk about the Great Moderation at the macro level but for individual workers it was just the opposite.

An unemployment trap

Loungani: How does this lead to the trap?

Sargent: Well, think about what can happen when workers suffer a permanent hit to their incomes, and you offer then the alternative of generous and long-lasting unemployment benefits. For older workers, particularly, the benefits become an attractive option relative to looking hard for another job, which is not going to pay as much because your human capital just took a hit. And getting retrained is hard. I mean I was just 30 when my human capital was hit. You know I went to Harvard, right? I actually got pretty good at playing around with the IS/LM model, which is what I learnt there. And then a new thing—rational expectations—came along and I had to learn all this math and it was hard. Well, if you’re in your 50s you’re not going to be eager to try out the hard things. You’ll try to get by with the unemployment benefits. You end up with lots of workers who are detached from the labor force. I think that’s what happened in Europe in the 1980s. They’d always had more a generous welfare system but the impact of that wasn’t felt until the nature of the shocks to incomes changed in the manner that I described.

Loungani: Yes, the interaction of shocks and institutions. Olivier Blanchard once said when the shocks changed Europe became like someone wearing a winter jacket in the summertime—the labor market institutions curbed flexibility when it was needed.

Sargent: Exactly. So I think the people who want to keep extending U.S. unemployment benefits have the right motives but we can end up in the wrong place—a world of persistent high unemployment. So, while in the case of fiscal institutions Europe could look to early U.S. history, in the case of labor market institutions, the U.S. should keep in mind the European experience of not so long ago.

|

| Photo: Stephen Jaffe/IMF |

|

| Photo: Stephen Jaffe/IMF |

Thomas Sargent, winner of the 2011 Nobel Prize in Economic Science, has made several visits over the past year to the IMF’s Research Department. Last week, he talked to Prakash Loungani about problems ailing Europe and the United States—and what each could learn from the other’s history.

Photo: Stephen Jaffe/IMF

Loungani: Europe’s fiscal challenges are foremost on minds here. This is something you have worked on in the past—the interplay of monetary and fiscal policy.

Posted by at 12:30 AM

Labels: Profiles of Economists

Friday, January 27, 2012

Davos told that stimulus and social protection vital for growth

Owen Tudor at Touch Stone reports:

The World Economic Forum (best known for hosting this week’s Davos conference) plays host to a number of Global Agenda Councils which bring together experts in a particular field to produce reports summing up the best available wisdom on what to do next. There’s a GAC on Employment and Social Protection which has produced a report for Davos 2012 snappily titled “The Case for an Integrated Model of Growth, Employment and Social Protection“. But it makes some very pertinent recommendations for the global leaders gathered in Davos, and is part and parcel of the growing intellectual argument for growth and jobs to have a higher priority than debt and deficit reduction (see recent posts on ILO, IMF and OECD reports).

The GAC on Employment and Social Protection includes people you would expect to make these arguments – like Vice-Chair TUAC General Secretary John Evans, ITUCGeneral Secretary Sharan Burrow and AFLCIO chief economist Ron Blackwell – as well as people who work in the global institutions already leaning this way like Stephen Pursey of the ILO and Prakash Loungani of the IMF. But it also includes academics like Zhang Xiulan from Beijing Normal University and Jose Antonio Ocampo from Columbia University in the US; and business representatives like Premkumar Seshadri of India’s HCL Technologies and Thero Setiloane from Business Leadership South Africa. So it’s a broad-based group.

Their five recommendations are, very briefly:

- a coordinated growth stimulus to ensure employment remains a top priority, including slowing the pace of deficit reduction in countries with the fiscal space to do so (which would certainly include the UK);

- immediate boosts to job creation and retention, such as youth employment promises and short-time working schemes;

- using social protection to help stimulate growth;

- establishing a social protection floor in developing countries, including cash transfers like Brazil’s Bolsa Familia; and

- governments working on growth and social protection with other stakeholders such as unions, business and NGOs.

Owen Tudor at Touch Stone reports:

The World Economic Forum (best known for hosting this week’s Davos conference) plays host to a number of Global Agenda Councils which bring together experts in a particular field to produce reports summing up the best available wisdom on what to do next. There’s a GAC on Employment and Social Protection which has produced a report for Davos 2012 snappily titled “The Case for an Integrated Model of Growth,

Posted by at 1:00 AM

Labels: Inclusive Growth

Monday, January 23, 2012

Manufacturing: Hope or Hopeless?

Recent headlines suggest the ‘Made in the USA’ label is back in business. “Manufacturing employment has grown faster in the US than in any other leading developed economy since the start of the recovery,” says the FT. Indicators of the manufacturing sector also point to an optimistic outlook, according to January’s Business Outlook Survey of Philadelphia Fed.

The manufacturing outlook seems good in the rest of the world too with the exception of Europe. World industrial production will grow 5% next year, compared to 4.5% in 2011, according to Dan Meckstroth (Chief Economist of Manufacturers Alliance for Productivity and Innovation—MAPI).

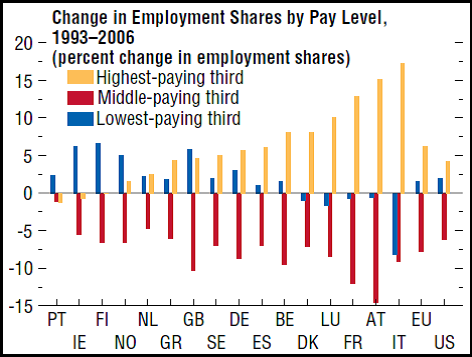

But, beneath the surface things seem less hopeful, particularly in the advanced economies. For more than a decade, there has been a “hollowing out” of jobs in these economies — a striking loss of middle-income and manufacturing jobs – as summarized in a research piece I coauthored. The chart below shows a striking decline in middle-income jobs in advanced economies between 1993 and 2006.

This trend has continued over the past few years. “During the recession and recovery … highly skilled workers have done best, low-skill workers have done poorly, and those in middle-skill employment have done very, very poorly,” according to a recent article in The Economist. “Even as the job market has improved over the past year … employment among workers without a high-school degree rose by 126,000. Employment for workers with a college degree rose by just over 1m jobs. For those with just a high-school diploma, however, employment fell by 551,000.”

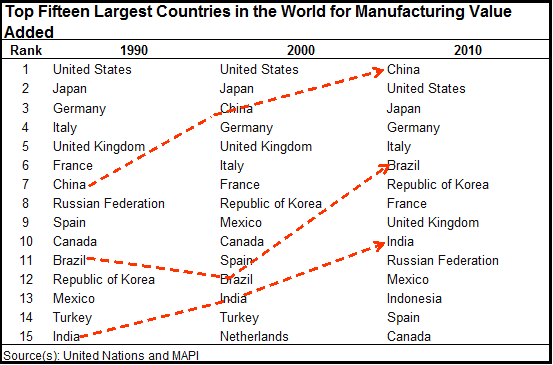

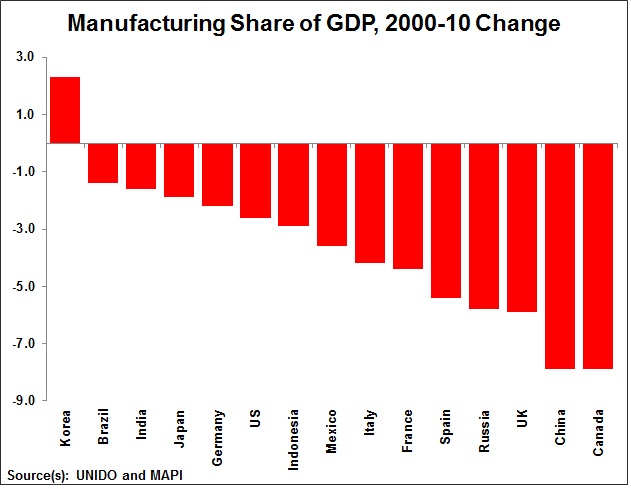

Advanced economies are also losing market share in manufacturing to emerging economies.

And in both advanced and emerging economies, manufacturing share’s of GDP is declining.

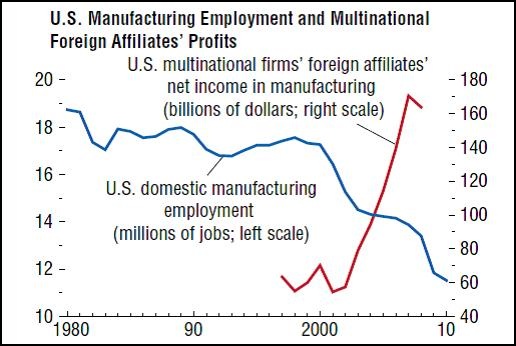

My research notes that the decline in manufacturing jobs accelerated during the 2000s and was accompanied by a huge increase in advanced economies’ imports from low-income countries. Other authors estimate that at least one-third of the aggregate decline in U.S. manufacturing employment during 1990–2007 can be attributed to increased imports from emerging markets. The chart below shows the sharp decline in U.S. manufacturing jobs and the increase in the profits of multinational firms during the 2000s. Meckstroth also points out that non financial corporate profits are nearly back to their peak, in particular, income for foreign affiliates which are extremely profitable.

Recent headlines suggest the ‘Made in the USA’ label is back in business. “Manufacturing employment has grown faster in the US than in any other leading developed economy since the start of the recovery,” says the FT. Indicators of the manufacturing sector also point to an optimistic outlook, according to January’s Business Outlook Survey of Philadelphia Fed.

The manufacturing outlook seems good in the rest of the world too with the exception of Europe.

Posted by at 10:09 PM

Labels: Forecasting Forum

Subscribe to: Posts