Wednesday, July 10, 2013

House Prices in Chile

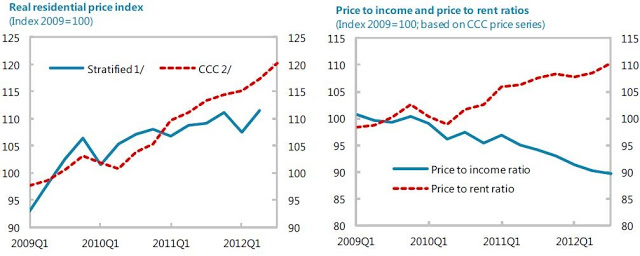

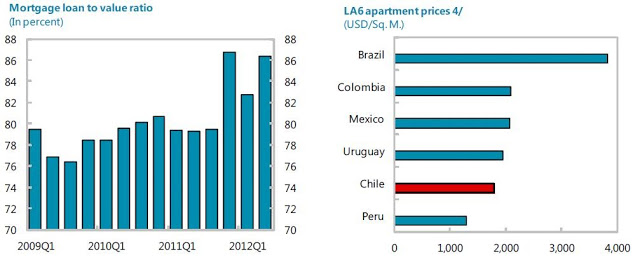

“The increase in housing prices has been strong but standard indicators do not suggest significant misalignment with fundamentals,” according to latest IMF’s report on Chile. On real estate developments, the report says that “real estate activity (supply and demand) has been dynamic. While residential housing prices in aggregate do not suggest bubbles, these averages hide considerable variation and some regions have seen substantial price increases that could spill over to other parts of the country. One sign of incipient froth in the housing market is the jump in average loan-to-value ratios to above 85 percent since late 2011, as highlighted in recent central bank financial stability reports. Another issue is the above-mentioned worsening in construction companies’ financial strength. As for construction, while residential housing activity seems to be cooling off, commercial real estate (for which data are spotty) remains hot with a substantial amount of office space being completed in 2013-14.”

“The increase in housing prices has been strong but standard indicators do not suggest significant misalignment with fundamentals,” according to latest IMF’s report on Chile. On real estate developments, the report says that “real estate activity (supply and demand) has been dynamic. While residential housing prices in aggregate do not suggest bubbles, these averages hide considerable variation and some regions have seen substantial price increases that could spill over to other parts of the country. One sign of incipient froth in the housing market is the jump in average loan-to-value ratios to above 85 percent since late 2011,

Posted by at 2:39 PM

Labels: Global Housing Watch

Friday, June 21, 2013

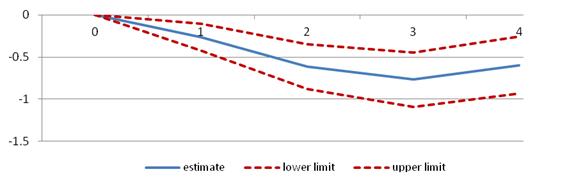

Does Fiscal Consolidation Raise Inequality?

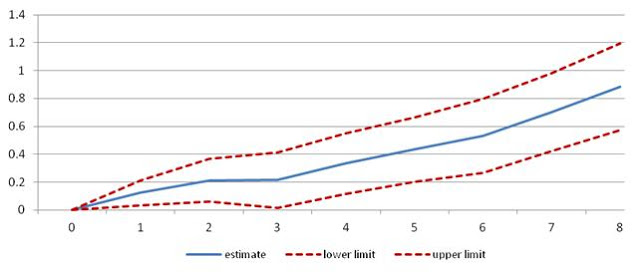

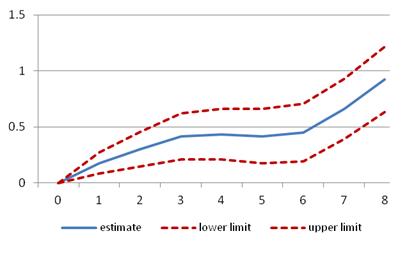

Fiscal tightening, whether based on cutting spending or raising taxes, has raised inequality and lowered the wage share of income. These are the main findings of my co-authored IMF working paper released today. The results are based on 173 episodes of fiscal consolidation during 1978-2009 for 17 OECD economies (Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Netherlands, Portugal, Spain, Sweden, the United Kingdom, and the United States). Some of the key charts from the paper are given below.

Fiscal consolidation raises inequality (as measured by the Gini Coefficient)

(The horizontal axis shows the year of the consolidation—year 0—and the impact up to 8 years after the consolidation)

Consolidation based on spending cuts raises inequality …

… as does consolidation based on tax increases

Fiscal consolidation lowers the wage share of income

Fiscal tightening, whether based on cutting spending or raising taxes, has raised inequality and lowered the wage share of income. These are the main findings of my co-authored IMF working paper released today. The results are based on 173 episodes of fiscal consolidation during 1978-2009 for 17 OECD economies (Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Netherlands, Portugal, Spain, Sweden, the United Kingdom, and the United States). Some of the key charts from the paper are given below.

Posted by at 7:07 PM

Labels: Inclusive Growth

Wednesday, June 19, 2013

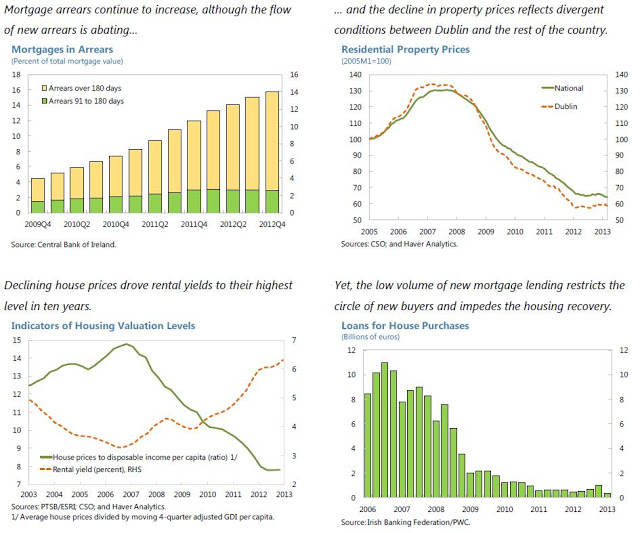

House Prices in Ireland

“House prices slipped back reflecting developments outside Dublin. After stabilizing over much of 2012, national residential property prices fell 2.6 percent in the first quarter of 2013, bringing the index to a new low 51 percent below its pre-crisis peak,” according a new IMF report on Ireland. What explains the drop in prices? The report says that “this decline was driven by an almost 4 percent price fall outside Dublin, reflecting divergent market conditions—the stock of property available for sale in Dublin amounts to around 6 months‘ supply, Read the full article…

Posted by at 4:49 PM

Labels: Global Housing Watch

Monday, June 17, 2013

MAULDIN: Economists Are Totally Clueless About The Economy

“In November of 2008, as stock markets crashed around the world, the Queen of England visited the London School of Economics to open the New Academic Building. While she was there, she listened in on academic lectures. The Queen, who studiously avoids controversy and almost never lets people know what she’s actually thinking, finally asked a simple question about the financial crisis: “How come nobody could foresee it?” No one could answer her.”

“If you’ve suspected all along that economists are useless at the job of forecasting, you would be right. Dozens of studies show that economists are completely incapable of forecasting recessions. But forget forecasting. What’s worse is that they fail miserably even at understanding where the economy is today. In one of the broadest studies of whether economists can predict recessions and financial crises, Prakash Loungani of the International Monetary Fund wrote very starkly, “The record of failure to predict recessions is virtually unblemished.” He found this to be true not only for official organizations like the IMF, the World Bank, and government agencies but for private forecasters as well. They’re all terrible. Loungani concluded that the “inability to predict recessions is a ubiquitous feature of growth forecasts.” Most economists were not even able to recognize recessions once they had already started.” Read the full article here.

“In November of 2008, as stock markets crashed around the world, the Queen of England visited the London School of Economics to open the New Academic Building. While she was there, she listened in on academic lectures. The Queen, who studiously avoids controversy and almost never lets people know what she’s actually thinking, finally asked a simple question about the financial crisis: “How come nobody could foresee it?”

Posted by at 6:43 PM

Labels: Forecasting Forum

Wednesday, May 29, 2013

Tackling Unemployment: Return of the Two-Handed Approach

Unemployment in advanced economies averages 8% today, a sharp rise from 5 ½ % at the start of the Great Recession. European unemployment is particularly high—about 11% on average. What can be done?

In a celebrated mid-1980s paper, Olivier Blanchard, along with Rudi Dornbusch and others, argued that tackling the high unemployment and low growth in Europe at that time would require a ‘two-handed approach’: a combination of demand-side and supply-side policies. It is not coincidental that the IMF’s current advice to countries reflects the return of the two-handed approach.

In presentations delivered at the European Commission, ILO, World Bank and other venues, Prakash Loungani—advisor in the Research Department and co-chair of the IMF’s “Jobs & Growth” working group—has made the case for balancing demand and supply initiatives to tackle unemployment in advanced economies. He notes that, contrary to some assertions, unemployment and growth have remained linked during the Great Recession and the Not-So-Great Recovery. This preserves the hope that the jobs will return when the growth does.

Evidence suggests that the bulk of the rise in unemployment in most countries has been cyclical. Hence, as the Wall Street Journal noted recently, it’s time to “stop worrying about the ‘jobless recovery’ [and] start worrying about the recovery-less recovery.” Citing work on Okun’s Law by IMF authors and other recent evidence, the Journal concluded that “it isn’t unemployment benefits or other specific [structural] factors that are holding back hiring. It’s the economy, stupid.”

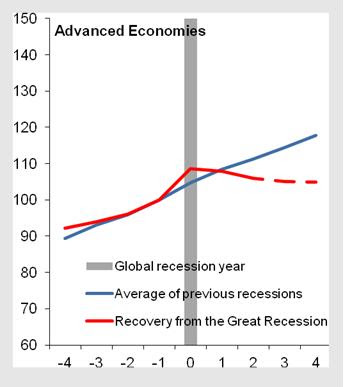

Several factors are behind the tepid recovery in output. In work done for the recent World Economic Outlook, Ayhan Kose, Prakash Loungani and Marco Terrones note that a key difference between the current global recovery and past global recoveries is that fiscal policy has not been able to provide the support this time that it did in the past—a point that has been picked by many observers including Paul Krugman (see the figure on fiscal spending below and Krugman’s essay here).

|

| Real Primary Government Expenditures |

The two-handed approach does not neglect supply. In a recent Staff Discussion Note, Olivier Blanchard, Florence Jaumotte and Prakash Loungani discuss many labor market reforms that have been advocated in recent IMF programs in Europe. They argue that, by and large, these reforms can be expected to contribute to ‘micro flexibility’ (the ability of the economy to reallocate workers across jobs to boost productivity) and ‘macro flexibility’ (the ability of the economy to adjust to macroeconomic shocks).

Unemployment in advanced economies averages 8% today, a sharp rise from 5 ½ % at the start of the Great Recession. European unemployment is particularly high—about 11% on average. What can be done?

In a celebrated mid-1980s paper, Olivier Blanchard, along with Rudi Dornbusch and others, argued that tackling the high unemployment and low growth in Europe at that time would require a ‘two-handed approach’: a combination of demand-side and supply-side policies.

Posted by at 1:39 PM

Labels: Inclusive Growth

Subscribe to: Posts