Wednesday, February 14, 2018

House Prices in Korea

From the IMF’s latest report on Korea:

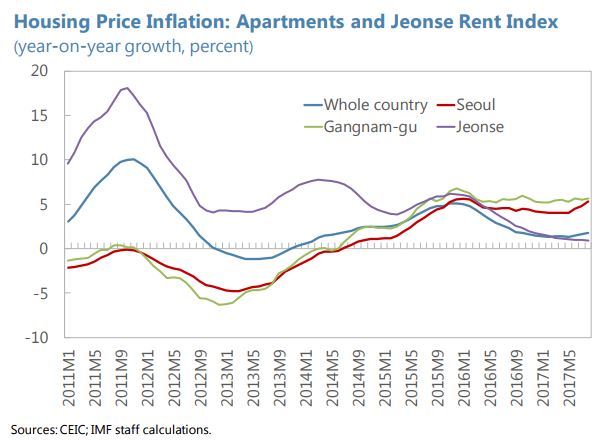

“The financial sector is sound, with high and rising household debt the main domestic financial stability risk. Household debt exceeds 90 percent of GDP, increasing vulnerability to both a housing price correction and a sharp rise in interest rates. A tightening of macroprudential measures has helped slow household credit growth to 7.8 percent year-on-year in October, from the 12-percent average annual growth rate in 2016. The increase in house prices nationally has slowed to about 1 percent year-over-year; but in Seoul apartment prices are still rising at a nearly 5-percent annual rate. Macroprudential policy measures, including some targeting speculative buying of apartments in Seoul, should help stabilize prices. According to staff analysis, the overall housing prices level is in line with fundamentals. However, there remains a risk of a price correction in the region around Seoul, which experienced larger price increase and where the surge in supply from the construction boom could weigh on prices.”

From the IMF’s latest report on Korea:

“The financial sector is sound, with high and rising household debt the main domestic financial stability risk. Household debt exceeds 90 percent of GDP, increasing vulnerability to both a housing price correction and a sharp rise in interest rates. A tightening of macroprudential measures has helped slow household credit growth to 7.8 percent year-on-year in October, from the 12-percent average annual growth rate in 2016.

Posted by at 10:03 AM

Labels: Global Housing Watch

Korea: Macroprudential Policy and High Household Debt

From the latest IMF’s report on Korea:

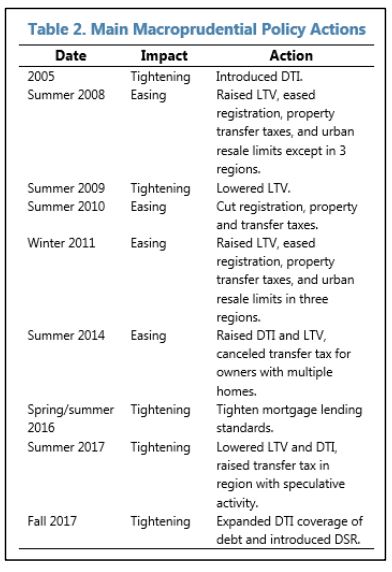

“Macroprudential policies are being extensively used to curb risks from high household debt and credit growth. A broad range of macroprudential instruments that have been tightened and new ones introduced (Table 2). The loan-to-value (LTV) and debt-to-income (DTI) ratios were reduced to record lows of 40 percent, and are now well below recent highs of 70 and 60 percent, respectively, to which they were increased in August 2014. And, a lower level of 30 percent was set for borrowers with multiple mortgages and in designated regions of speculative activity, mostly around Seoul. In October 2017, the DTI was effectively tightened further by broadening the range of debt subject to it. Also announced is a new, debt service ratio (DSR) with comprehensive coverage of all household debts, which will be implemented for banks in mid-2018; and then for NBFIs at the start of 2019.

Evidence suggests that this macroprudential tightening will be effective. The growth in credit to households has slowed significantly over the last few months. Moreover, speculative purchases of apartments before construction is has diminished. An event study analysis by Federal Reserve Board economists finds that hikes in LTVs and DTIs have been effective in slowing credit growth and housing price increases. New cross-country panel regression analysis show that use of LTVs and DTIs is effective in reducing real household credit growth across 34 advanced and emerging market economies, including Korea.”

From the latest IMF’s report on Korea:

“Macroprudential policies are being extensively used to curb risks from high household debt and credit growth. A broad range of macroprudential instruments that have been tightened and new ones introduced (Table 2). The loan-to-value (LTV) and debt-to-income (DTI) ratios were reduced to record lows of 40 percent, and are now well below recent highs of 70 and 60 percent, respectively, to which they were increased in August 2014.

Posted by at 9:55 AM

Labels: Global Housing Watch

Labor Mobility and the Role of Housing Prices in UK

From the IMF’s latest report on UK:

“Barriers to labor mobility may reduce its effectiveness as a regional adjustment mechanism. Migration of workers from poor, low-productivity areas to rich and highly productive ones is an important channel through which cross-region convergence may be achieved. Factors distorting internal labor flows are potentially relevant determinants of regional disparities in income and productivity. Indeed, the pattern of internal flows for England and Wales shows that highly productive regions tend to have net outflows instead of inflows. This suggests that factors other than labor market conditions (i.e. productivity differentials) are likely significant determinants of internal migration patterns in the UK.

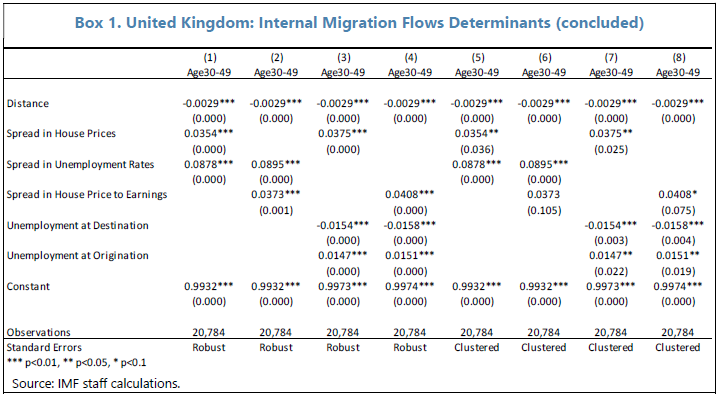

Housing prices (and regulations) have a significant impact on internal migration patterns in the UK. Analysis of bilateral gross flows between regions in England and Wales shows that house prices are negatively related to workers’ movement from one region to another (Box 1). Results are in line with Biswas et al. (2009), who study inter-regional migration in England, Wales, Scotland and Northern Ireland, and Rabe and Taylor (2010), who analyze internal migration flows using household-level data for 11 regions in the UK. In turn, Hilber and Vermeulen (2015) show that housing prices are significantly (causally) affected by housing regulations. The impact is economically large: if the South East (the most regulated English region) had the regulatory restrictiveness of the North East, house prices in the South East would have been roughly 25 percent lower in 2008.

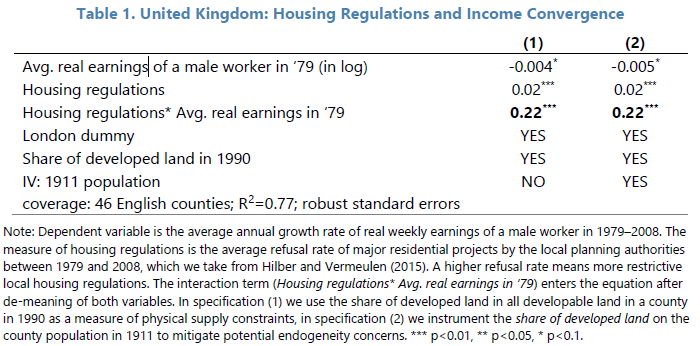

Evidence also suggests that local housing regulatory constraints have affected income convergence across regions. Data on local housing regulatory restrictions for 46 English counties is used to test whether housing restrictions have affected interregional convergence in the UK. The specification, following Ganong and Shoag (2015), models the change in workers’ real earnings between 1979 and 2008 as a function of its starting level in 1979, a measure of severity of housing restrictions in the same period from Hilber and Vermeulen (2015), and an interaction term of the two variables (Table 1). The coefficient on the starting level of earnings is significant and negative, suggesting income convergence between counties with low initial earnings and counties with a high starting level of earnings. The interaction term of earnings and housing regulations is highly significant and positive, indicating a dampening effect of tighter housing regulations on the speed of convergence across counties. To the extent that earnings are correlated with productivity, housing restrictions have likely contributed to differences in productivity across regions as well.

Policy measures to promote housing supply may therefore have a positive impact on labor mobility and growth. Regulatory constraints tend to be higher and more binding in more developed and productive areas (see Hilber and Robert-Nicoud 2013). Evidence from the US suggests that lowering regulatory constraints in the more productive cities would favor a more efficient allocation of labor and have an economically significant effect on growth (Hsieh and Moretti 2017). Efforts should continue to further boost housing supply, including by easing planning restrictions, mobilizing unused publicly-owned lands for construction, and providing incentives for local authorities to facilitate residential development (Hilber 2015, IMF 2016, and OECD 2017).”

From the IMF’s latest report on UK:

“Barriers to labor mobility may reduce its effectiveness as a regional adjustment mechanism. Migration of workers from poor, low-productivity areas to rich and highly productive ones is an important channel through which cross-region convergence may be achieved. Factors distorting internal labor flows are potentially relevant determinants of regional disparities in income and productivity. Indeed, the pattern of internal flows for England and Wales shows that highly productive regions tend to have net outflows instead of inflows.

Posted by at 9:52 AM

Labels: Global Housing Watch, Inclusive Growth

Regional Disparities and Inclusive Growth in UK

A new IMF report on UK says that “Reducing regional disparities by boosting labor productivity in underperforming regions would promote faster and more inclusive growth. Interregional differences in productivity are related to differences in well-being and inclusion. For instance, UK regions with low productivity tend to have a larger share of young population that is neither employed, in training or in education. At the same time, disparities may signal untapped potential for catching up, and if addressed may contribute to overall growth. The potential benefits of addressing regional disparities have long been recognized by UK authorities, and all recent major party manifestos promised action to reduce them. Policies should be judged based on their impact on growth and inclusion, rather than whether they narrow the gap between particular regions. The challenge for the government is to help address failures or frictions underpinning regional disparities, allowing those less successful regions to build the conditions for economic success, while not cutting off the ability of leading regions to play their role.”

Continue reading here.

A new IMF report on UK says that “Reducing regional disparities by boosting labor productivity in underperforming regions would promote faster and more inclusive growth. Interregional differences in productivity are related to differences in well-being and inclusion. For instance, UK regions with low productivity tend to have a larger share of young population that is neither employed, in training or in education. At the same time, disparities may signal untapped potential for catching up,

Posted by at 9:39 AM

Labels: Inclusive Growth

Monday, February 12, 2018

The Harsh Realism of Adam Smith

From Branko Milanovic and the Globalist:

“Under the influence of Amartya Sen, we have been “nudged” towards a reassessment of the relative merits of “The theory of moral sentiments “ (TMS) and “The Wealth of Nations” (WN). Sen has done a lot to bring Smith’s early work out of relative obscurity where it was consigned by two centuries of success of The Wealth of Nations.

What remains true is that many people around the world continue to have a remarkably distorted view of The Wealth of Nations. Not much beyond the (in)famous “invisible hand of the market.”

Bad government

In reality, there are no “good guys” in The Wealth in Nations. Of course, the government comes in for special criticism.

Smith argues against its rapacity in putting up high tariffs, its foolishness in following mercantilist policies, its pettiness in constraining the system of “natural liberty,” its attempts to decide where people should live (the law of settlement, a hukou-like system was then in existence in Britain).

(…)

Bad businessmen

But businessmen are no better. As soon as they are given half a chance, perhaps just after having gotten rid of some particularly nefarious government regulation, they are back to plotting how to “restrain” the market, to pay suppliers less, destroy competitors, cheat workers (see today’s IT companies, Walmart, Amazon).

In the famous quote, “people of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices” (Book 1, Ch. 8).

In their mad ambition, they try to rule the world (see Davos): “…the mean rapacity, the monopolizing spirit of merchants and manufacturers, who neither are, nor ought to be, the rulers of mankind” (Book 4, Ch. 3, p. 621).”

Read the full article here.

From Branko Milanovic and the Globalist:

“Under the influence of Amartya Sen, we have been “nudged” towards a reassessment of the relative merits of “The theory of moral sentiments “ (TMS) and “The Wealth of Nations” (WN). Sen has done a lot to bring Smith’s early work out of relative obscurity where it was consigned by two centuries of success of The Wealth of Nations.

What remains true is that many people around the world continue to have a remarkably distorted view of The Wealth of Nations.

Posted by at 10:28 AM

Labels: Macro Demystified

Subscribe to: Posts