Friday, September 7, 2018

New Evidence that Unions Raise Wages for Less-Skilled Workers

From a new post by Steve Maas:

“New Evidence that Unions Raise Wages for Less-Skilled Workers: Tapping into eight decades of private and public surveys, a new study finds evidence that unions have historically reduced income inequality.

For Unions and Inequality over the Twentieth Century: New Evidence from Survey Data (NBER Working Paper No. 24587), Henry S. Farber, Daniel Herbst, Ilyana Kuziemko, and Suresh Naidu assembled a household-level database on union membership dating back to 1936.

The U.S. Bureau of the Census has tracked wages and education consistently since 1940. Aggregate data on union membership goes back to the early 20th century, but data on individual workers were not readily available until the Census Bureau started asking about union affiliation in 1973. By that time, unions were already in decline, and higher-skilled workers accounted for an increasing share of their membership.

The researchers draw on more than 500 surveys conducted by Gallup and other pollsters from 1936 through 1986, extending their dataset into the present day with information from government surveys and other sources.

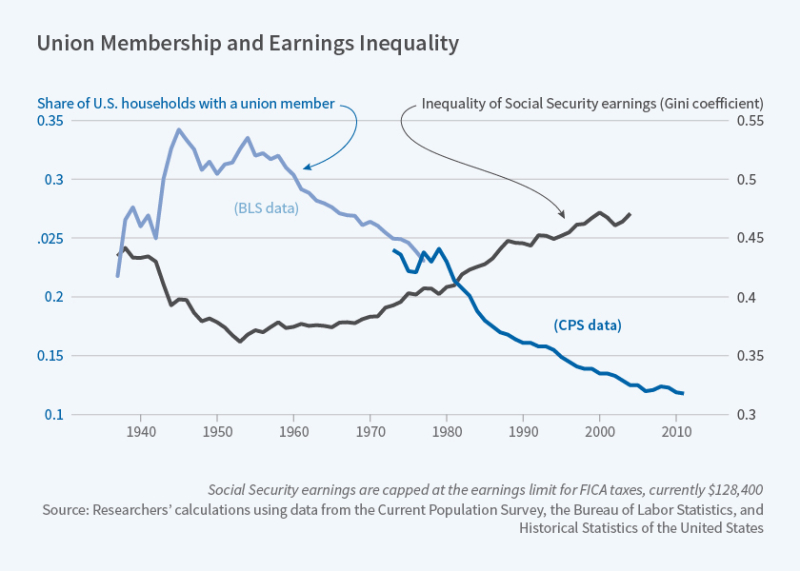

Their study finds that the salary premium for union members compared to workers with comparable skills and demographic characteristics has remained relatively steady over the last 80 years despite large swings both in the overall number of union members and in their education levels. The less skilled the workers were, the greater the wage premium associated with their union membership. The researchers find a negative correlation between unionization rates and measures of inequality such as the Gini coefficient.

Between 1940 to 1970, when unionization peaked and income inequality narrowed, unions were drawing in the least-skilled workers. Before and after that period, unions were smaller and a higher fraction of their members were drawn from the ranks of high-skill workers. The 1940 – 1970 period also coincided with the highest share of union members drawn from minority groups.

The clear implication of the researchers’ analysis is that, because unions offer a larger wage premium to less-skilled workers, unions have an important equalizing effect on the income distribution to the extent that they are successful in organizing the less-skilled. Recent decades have seen growth in educational attainment in the workforce, and, importantly, not only has the overall share of workers who are unionized declined, but unions have also become relatively less successful in organizing less-skilled workers. The remaining unionized workforce is more highly educated than it was earlier. The combination of the declining presence of unions in the labor market and the increased skill level of the remaining union workers means that the important equalizing effect of unions on the income distribution that was seen in the middle of the 20th century has diminished substantially.”

From a new post by Steve Maas:

“New Evidence that Unions Raise Wages for Less-Skilled Workers: Tapping into eight decades of private and public surveys, a new study finds evidence that unions have historically reduced income inequality.

For Unions and Inequality over the Twentieth Century: New Evidence from Survey Data (NBER Working Paper No. 24587), Henry S. Farber,

Posted by at 12:45 PM

Labels: Inclusive Growth

A Shorter Work Week?

From a new Conversable Economist post by Timothy Taylor:

“The biggest European union has managed to achieve a long-standing goal: German metal-workers can now work a 28-hour week, if they wish. […] What do German employers get out of this deal? They get flexibility, in the sense that if some workers want to work longer hours, the firm can hire them to do so. Furthermore, Pencavel argues that for many workers, labor exhibits diminishing marginal productivity over the work-week: that is, the 25th hour worked in a week is on average more productive than the 35th or the 45th hour worked. Thus, employers will be getting the more productive hours from workers, for the same hourly pay.”

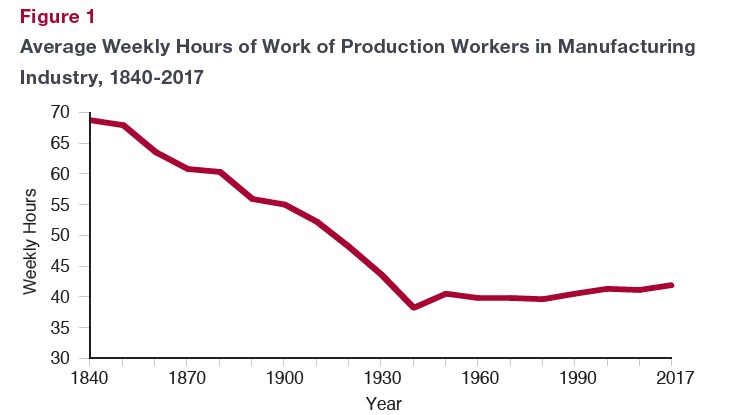

“Does a drive for lower hours have any resonance in the US economy? Pencavel points out that in the US labor market, weekly hours worked dropped sharply in the decades leading up to 1930 or so, but since then, the decline has largely stopped. (And for the record, American unions in certain induistries remained quite powerful in the 1950s and 1960s, and they might well have succeeded in pushing for lower weekly hours if it had been a priority for them.)”

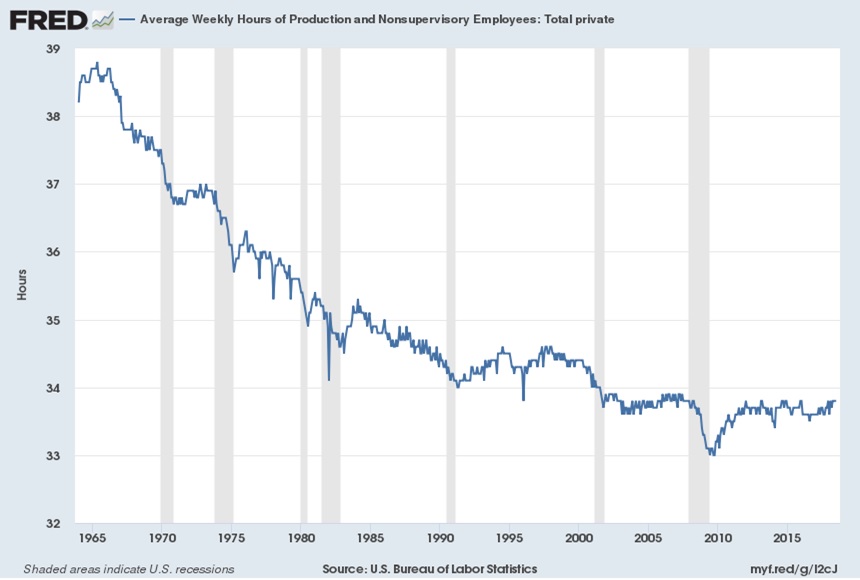

“Here’s a different figure, not from Pencavel’s brief, showing average weekly hours for production and nonsupervisory workers in all industries, not just manufacturing. This average includes part-timers. This shows an ongoing drop over time, although it may have levelled out around the year 2000. Specifically: “Average weekly hours relate to the average hours per worker for which pay was received and is different from standard or scheduled hours. Factors such as unpaid absenteeism, labor turnover, part-time work, and stoppages cause average weekly hours to be lower than scheduled hours of work for an establishment. … Average weekly hours are the total weekly hours divided by the employees paid for those hours.””

“It’s an interesting Labor Day question as to how many US workers would we willing to make the tradeoff of lower hours for less total income (assuming they would not see diminished job security as a result). From a US context, one interesting pattern is that lower-wage workers used to be the ones who on average worked the longest hours, but now it’s higher-wage workers. “

From a new Conversable Economist post by Timothy Taylor:

“The biggest European union has managed to achieve a long-standing goal: German metal-workers can now work a 28-hour week, if they wish. […] What do German employers get out of this deal? They get flexibility, in the sense that if some workers want to work longer hours, the firm can hire them to do so. Furthermore, Pencavel argues that for many workers,

Posted by at 11:29 AM

Labels: Inclusive Growth

Understanding the Decline of U.S. Manufacturing Employment

From a new working paper by Susan N. Houseman:

“Two stylized facts underlie the prevailing view that automation largely caused the relative decline and, in the 2000s, the large absolute decline in U.S. manufacturing employment: first, manufacturing real output growth has largely kept pace with that of the aggregate economy for decades, and second, manufacturing labor productivity growth has been considerably higher. These statistics appear to provide a compelling case that domestic manufacturing is strong, and that, as in agriculture, productivity growth, assumed to reflect automation, is largely responsible for the relative and absolute decline in manufacturing employment. Although the size and scope of the decline in employment manufacturing industries in the 2000s was unprecedented, many

see it as part of a long-term trend and deem the role of trade small.”

“That view, I have argued, reflects a misinterpretation of the numbers. First, aggregate manufacturing output and productivity statistics are dominated by the computer industry and mask considerable weakness in most manufacturing industries, where real output growth has been much slower than average private sector growth since the 1980s and has been anemic or declining since 2000. Second, labor productivity growth is not synonymous with, and is often a poor indicator of, automation. Measures of labor productivity growth may capture many forces besides automation—including improvements in product quality, outsourcing and offshoring, and a changing industry composition owing to international competition. Indeed, the rapid productivity growth in the computer and electronics products industry, and by extension in the manufacturing sector, largely reflects improvements in product quality, not automation. In short, the stylized facts, when properly interpreted, do not provide prima facie evidence that automation drove the relative and absolute decline in manufacturing employment.”

“It is difficult to parse out the effects of various factors on manufacturing employment, and research does not provide simple decompositions of the total contribution that trade and the broader forces of globalization make to manufacturing’s recent employment decline. Nevertheless, the research evidence points to trade and globalization as the major factor behind the large and swift decline of manufacturing employment in the 2000s. Although manufacturing processes continue to be automated, there is no evidence that the pace of automation in the sector accelerated in the 2000s; if anything, research comes to the opposite conclusion.”

“Manufacturing still matters, and its decline has serious economic consequences. Reflecting the sector’s deep supply chains, manufacturing’s plight contributed to the weak employment growth and poor labor market outcomes prevailing during much of the 2000s. Research shows that such large-scale shocks have persistent adverse effects on affected communities and their residents, though these costs rarely are fully considered in policy making (Klein, Schuh, and Triest 2003). In addition, because manufacturing accounts for a disproportionate share of R&D, the health of manufacturing industries has important implications for innovation in the economy. The widespread denial of domestic manufacturing’s weakness and globalization’s role in its employment collapse has inhibited much-needed, informed debate over trade policies.”

From a new working paper by Susan N. Houseman:

“Two stylized facts underlie the prevailing view that automation largely caused the relative decline and, in the 2000s, the large absolute decline in U.S. manufacturing employment: first, manufacturing real output growth has largely kept pace with that of the aggregate economy for decades, and second, manufacturing labor productivity growth has been considerably higher. These statistics appear to provide a compelling case that domestic manufacturing is strong,

Posted by at 10:56 AM

Labels: Inclusive Growth, Macro Demystified

Housing View – September 7, 2018

On cross-country:

- Global developments in residential property prices – first quarter of 2018 – Bank for International Settlements

- Hypostat 2018: recent developments in housing and mortgage markets in Europe and beyond – European Mortgage Federation

- The effect of house prices on household borrowing: A new approach – VOX

- Global luxury house prices: performance in 2018 so far – Knight Frank

On the US:

- The story of a house: how private equity swooped in after the subprime crisis – Financial Times

- Measuring Gentrification: Using Yelp Data to Quantify Neighborhood Change – NBER

- Liquidity vs. Wealth in Household Debt Obligations: Evidence from Housing Policy in the Great Recession – NBER

- Lessons from the financial crisis: The central importance of a sustainable, affordable and inclusive housing market – Brookings

- Three ways to strengthen the affordable rental housing supply – Urban Institute

On other countries:

- [Australia] Australia’s property boom ends as credit squeeze begins – Financial Times

- [Brazil] Can Housing Be Affordable Without Being Efficient? – World Resources Institute

- [China] China struggles to heed Xi’s call to develop rental housing – Financial Times

- [China] Housing Affordability in Urban China: A Comprehensive Overview – SSRN

- [Hong Kong] Hong Kong’s hot property sector show signs of cooling – Financial Times

- [Hong Kong] Hong Kong’s Runaway Property Market May Be Heading for a Fall – Bloomberg

- [Netherlands] Netherlands’ housing market remains strong – Global Property Guide

- [United Kingdom] History Dependence in the Housing Market – Centre for Economic Performance

- [United Kingdom] London housing: the bearish Brexit take – Financial Times

- [United Kingdom] Can house prices teach us anything about schools? – BBC

Photo by Aliis Sinisalu

On cross-country:

- Global developments in residential property prices – first quarter of 2018 – Bank for International Settlements

- Hypostat 2018: recent developments in housing and mortgage markets in Europe and beyond – European Mortgage Federation

- The effect of house prices on household borrowing: A new approach – VOX

- Global luxury house prices: performance in 2018 so far – Knight Frank

On the US:

- The story of a house: how private equity swooped in after the subprime crisis – Financial Times

- Measuring Gentrification: Using Yelp Data to Quantify Neighborhood Change – NBER

- Liquidity vs.

Posted by at 10:26 AM

Labels: Global Housing Watch

Thursday, September 6, 2018

Housing Market in Latvia

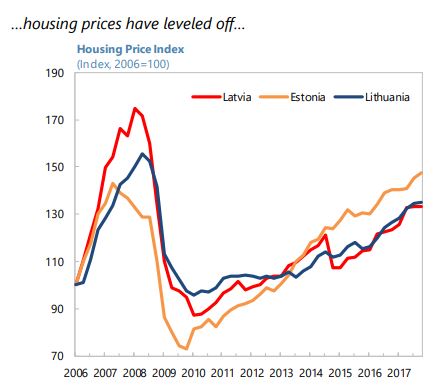

The IMF’s latest report on Latvia says:

“Improve access to housing. Current rental regulations discourage investment in rental housing. Below-market rents are common—a legacy of Soviet-era rental agreements—and rental dispute resolution mechanisms are time consuming and costly. More rental housing would facilitate labor mobility and help stem emigration.”

The IMF’s latest report on Latvia says:

“Improve access to housing. Current rental regulations discourage investment in rental housing. Below-market rents are common—a legacy of Soviet-era rental agreements—and rental dispute resolution mechanisms are time consuming and costly. More rental housing would facilitate labor mobility and help stem emigration.”

Posted by at 10:34 AM

Labels: Global Housing Watch

Subscribe to: Posts