Thursday, October 11, 2018

Inequality in and across Cities

From a new article by Jessie Romero and Felipe F. Schwartzman at the Richmond Fed:

“Inequality in the United States has an important spatial component. More-skilled workers tend to live in larger cities where they earn higher wages. Less-skilled workers make lower wages and do not experience similar gains even when they live in those cities. This dynamic implies that larger cities are also more unequal. These relationships appear to have become more pronounced as inequality has increased. The evidence points to externalities among high-skilled workers as a significant contributor to those patterns.”

“A large body of research has identified several key facts about inequality across and within cities. First, larger cities have a greater concentration of high-skilled workers. In the Fifth District, for example, the share of the population over age twenty-five with a bachelor’s degree is 45 percent in the most urban areas, compared with 16 percent in the most rural areas. In the United States as a whole, the proportion ranges from 35 percent in the most urban areas to 17 percent in the most rural areas.”

“Second, nominal wages are higher in larger cities and in cities with a larger proportion of high-skilled workers. In the most urban areas of the Fifth District, average annual pay in 2016 was nearly $64,000; in the most rural areas, it was less than $35,000. Nationwide, workers in the most urban areas earned about $60,000 on average in 2016, while workers in the most rural areas earned about $36,000. (See Figure 2 above.) In recent research, Nathaniel Baum-Snow, Matthew Freedman, and Ronni Pavan find that nominal wages increase 0.065 percent for every percentage point increase in city size (based on data from 2005–07). They also find that the relationship between city size and wages has strengthened over time and that the wage gap between urban and rural areas has increased”

From a new article by Jessie Romero and Felipe F. Schwartzman at the Richmond Fed:

“Inequality in the United States has an important spatial component. More-skilled workers tend to live in larger cities where they earn higher wages. Less-skilled workers make lower wages and do not experience similar gains even when they live in those cities. This dynamic implies that larger cities are also more unequal. These relationships appear to have become more pronounced as inequality has increased.

Posted by at 5:59 PM

Labels: Inclusive Growth

Wednesday, October 10, 2018

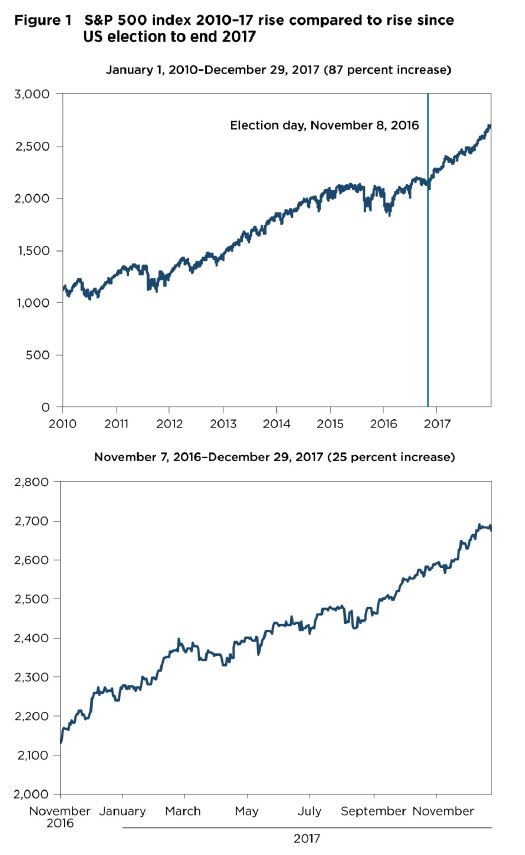

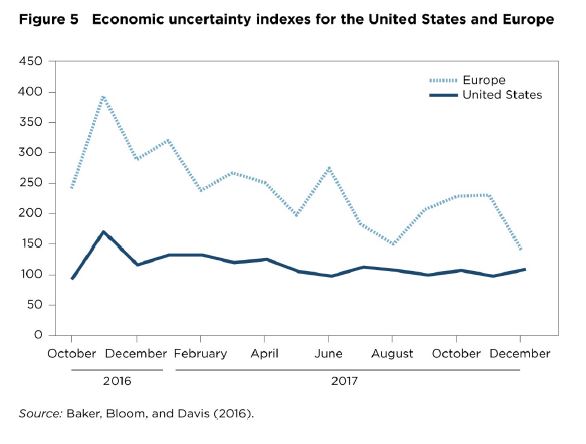

Why Has the Stock Market Risen So Much Since the US Presidential Election?

From a new paper by Olivier Blanchard, Christopher G. Collins, Mohammad R. Jahan-Parvar, Thomas Pellet, and Beth Anne Wilson:

“This paper looks at the evolution of U.S. stock prices from the time of the Presidential elections to the end of 2017. It concludes that a bit more than half of the increase in the aggregate U.S. stock prices from the presidential election to the end of 2017 can be attributed to higher actual and expected dividends. A general improvement in economic activity and a decrease in economic policy uncertainty around the world were the main factors behind the stock market increase. The prospect and the eventual passage of the corporate tax bill nevertheless played a role. And while part of the rise in stock returns came from a decrease in the equity risk premium, this decrease was relatively limited and returned the premium to the levels of the first half of the 2000s.”

From a new paper by Olivier Blanchard, Christopher G. Collins, Mohammad R. Jahan-Parvar, Thomas Pellet, and Beth Anne Wilson:

“This paper looks at the evolution of U.S. stock prices from the time of the Presidential elections to the end of 2017. It concludes that a bit more than half of the increase in the aggregate U.S. stock prices from the presidential election to the end of 2017 can be attributed to higher actual and expected dividends.

Posted by at 4:11 PM

Labels: Macro Demystified

Tuesday, October 9, 2018

Georgia: Residential Property Price Index

From the IMF’s latest report on Georgia:

“The compilation of an RPPI will facilitate the assessment of developments and risks in property markets. It will therefore be useful for monetary policy as it will improve the understanding of the linkages between property asset prices and financial assets. The National Bank of Georgia compiles a rudimentary index that tracks residential and commercial property prices in two districts of Tbilisi—one is known for expensive properties and the other for modestly priced properties. The index is therefore quite limited and is not disseminated.

On the RPPI, the mission proposed that, as a start, the index be restricted to the capital city and cover all transactions in new apartments and houses. Initially, the index will not include transactions in existing dwellings because of the complexity in covering these dwellings. Existing dwellings may be covered at a later stage when the RPPI methodology is stabilized and the staff gain the experience and skills in compiling the index.

Geostat should be able to compile the RPPI on a quarterly basis and disseminate the first index for the first quarter of 2021, in mid-May 2021. The RPPI will be developed by the same staff compiling the CPI; however, the production schedule for the RPPI can be arranged around the production and release schedule for the CPI to accommodate the available staff

resources. Based on the current CPI production schedule and the proposed RPPI development plan, additional staff would not be required.The most suitable data source for the RPPI may be the National Agency of Public Registry of Ministry of Justice (NAPR). Geostat informed the mission that it is compulsory to

register all transactions in dwellings with the NAPR. Therefore, the NAPR may collect information on transaction value, transactors, dwelling specifications, and location. An alternative source would be the two main websites for real estate transactions.”

From the IMF’s latest report on Georgia:

“The compilation of an RPPI will facilitate the assessment of developments and risks in property markets. It will therefore be useful for monetary policy as it will improve the understanding of the linkages between property asset prices and financial assets. The National Bank of Georgia compiles a rudimentary index that tracks residential and commercial property prices in two districts of Tbilisi—one is known for expensive properties and the other for modestly priced properties.

Posted by at 1:37 PM

Labels: Global Housing Watch

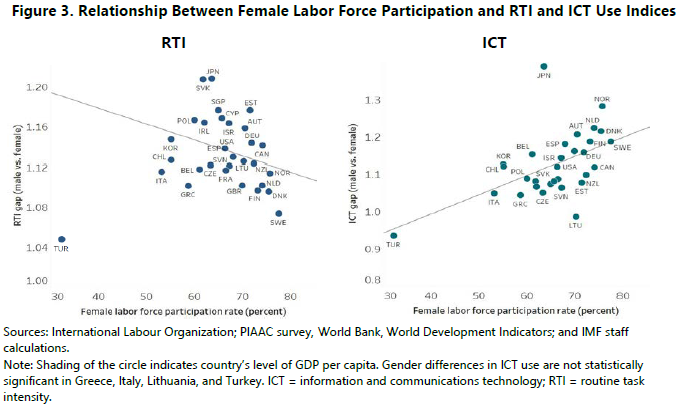

Gender, Technology, and the Future of Work

From a new IMF Staff Discussion Note:

“Opportunities and challenges. Women are underrepresented in science, technology, engineering, and mathematics (STEM) sectors anticipating jobs growth, where technological change can be complementary to human skills. There are some bright spots: job growth in traditionally female-dominated sectors, such as education and health services, will likely expand. The ongoing digital transformation is also likely to confer greater flexibility in work, benefitting women. But, breaking the “glass-ceiling” will be critical. Across sectors and occupations, underrepresentation of women in professional and managerial positions places them at high risk of displacement by technology.

Crucial role for policy. Fostering gender equality and gender empowerment in the changing landscape of work remains an imperative across countries.

- Endowing women with the requisite skills. Early investment in women in STEM fields, along with peer mentoring, can help break down gender stereotypes and increase retention. Fiscal instruments for those already in the workforce (e.g., tax deductions for training, portable individual learning accounts) can remove barriers to lifelong learning.

- Closing gender gaps in leadership positions. Family-friendly policies can play an important role in boosting women’s retention and career progression, but setting relevant recruitment and retention targets for organizations, promotion quotas, as well as mentorship and training programs to promote female talent into managerial positions should be considered.

- Bridging the digital divide. When it comes to the use of new technologies and access to them, countries must close gender gaps to improve women’s labor market prospects in the new world of work. Governments have a role to play through public investment in capital infrastructure and ensuring equal access to finance and connectivity.

- Easing transitions for workers. Ensuring gender equality in support for displaced workers through active labor market policies will be essential, given the high risk of automation faced by women. Ensuring that training and benefits are linked to individuals rather than jobs can help improve their reemployment prospects. Social protection systems will need to adapt to the new forms of work.”

From a new IMF Staff Discussion Note:

“Opportunities and challenges. Women are underrepresented in science, technology, engineering, and mathematics (STEM) sectors anticipating jobs growth, where technological change can be complementary to human skills. There are some bright spots: job growth in traditionally female-dominated sectors, such as education and health services, will likely expand. The ongoing digital transformation is also likely to confer greater flexibility in work, benefitting women. But, breaking the “glass-ceiling” will be critical.

Posted by at 10:49 AM

Labels: Inclusive Growth

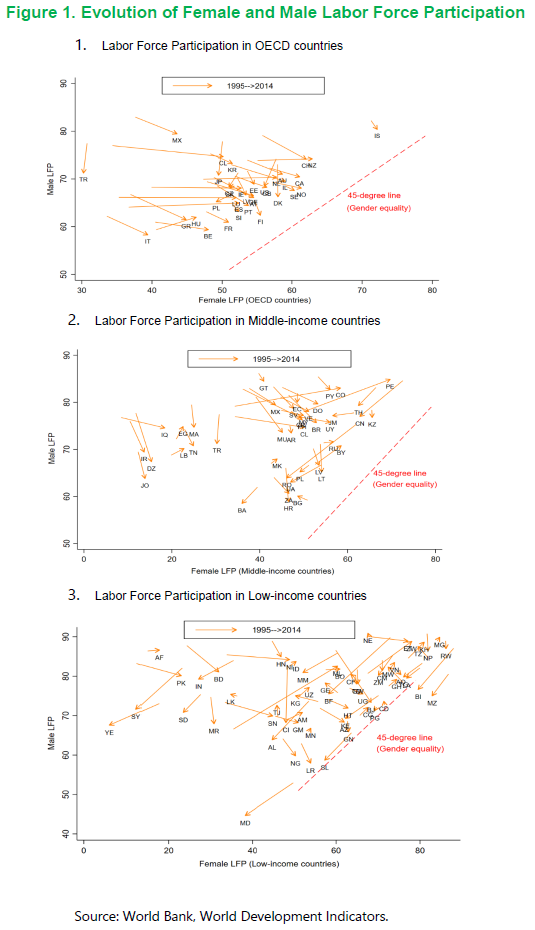

Economic Gains from Gender Inclusion: New Mechanisms, New Evidence

From a new IMF Staff Discussion Note:

“While progress has been made in increasing female labor force participation (FLFP) in the past 20 years, the pace has been uneven, and large gaps remain. FLFP was 54 percent for the median Organisation for Economic Co-operation and Development (OECD) country in 2014, 14 percentage points below male labor force participation (MLFP); for the median middle-income country, FLFP was only 49 percent, 26 percentage points below MLFP; and for the median low-income country, FLFP was 64 percent, 13 points below MLFP.

Narrowing participation gaps between women and men is likely to engender large economic gains, with two mechanisms pointing to larger gains than previously thought:

- Gender diversity: Women bring new skills to the workplace. This may reflect social norms and their impact on upbringing, social interactions, as well as differences in risk preference and response to incentives, for example. As such, there is an economic benefit from diversity—that is, from bringing women into the labor force—over and above the benefit resulting from simply having more workers. This hypothesis finds support in the data—both cross-country macro data and firm-level data. This paper finds that male and female labor are complementary in production. The results also imply that standard models, which do not differentiate between genders in their analysis, understate the favorable impact of gender inclusion on growth, and misattribute to technology a part of growth that is actually caused by women’s participation. The results further suggest that narrowing gender gaps benefits both men and women, because of a boost to male wages from higher FLFP.

- Sectoral reallocation: As households get richer during the process of economic development, demand for services rises, and labor is reallocated to the growing sector. Because services are more gender equal in employment than other sectors, developing economies naturally become more inclusive. But barriers to FLFP (which include tax distortions, discrimination, and social/cultural factors) slow this process, reducing output and welfare. This paper estimates that these barriers can depress FLFP by as much as a tax of up to 50 percent on female labor, depending on the region. Barriers not only hold back gender parity, they have a direct cost: welfare gains from their removal would exceed 20 percent in India, Pakistan and other countries in the Middle East and North Africa, for example.

These mechanisms imply that reducing female underemployment should yield greater gains than an equivalent increase in male employment: gender diversity brings benefits all its own.”

From a new IMF Staff Discussion Note:

“While progress has been made in increasing female labor force participation (FLFP) in the past 20 years, the pace has been uneven, and large gaps remain. FLFP was 54 percent for the median Organisation for Economic Co-operation and Development (OECD) country in 2014, 14 percentage points below male labor force participation (MLFP); for the median middle-income country, FLFP was only 49 percent, 26 percentage points below MLFP;

Posted by at 10:43 AM

Labels: Inclusive Growth

Subscribe to: Posts