Monday, November 5, 2018

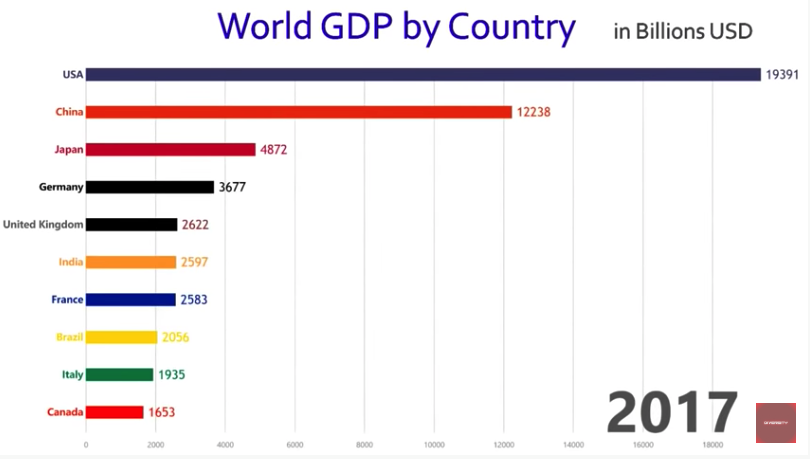

Dynamic chart: World’s ten largest economies, 1961 to 2017

From a new AEI post:

“Watch the top ten largest economies in the world based on GDP, year-by-year from 1961 to 2017. A few interesting observations:

1. The global slowdown in the early 1980s.

2. China’s ranking in the world’s ten largest economies has sure bounced around a lot. It was the world’s fifth largest economy in 1962 and remained in the top ten economies until it dropped out in 1978 and 1979, before returning in 1980, dropping out again for a few years and returning to the top ten in 1982. In 1987, China fell out for a year, came back in 1988, dropped out again in 1989 before returning to the top ten for good in 1992. By 2000, China rose to the No. 6 position by passing Italy, then to No. 5 in 2005 when it surpassed France, to No. 4 in 2006 when it surpassed the UK, No. 3 in 2007 surpassing Germany, and finally rising to No. 2 in 2010 by surpassing Japan.

3. As of 2017, the US economy at $19.4 trillion was 58.4% larger than China’s GDP of $12.2 trillion.”

Watch the dynamic chart here.

From a new AEI post:

“Watch the top ten largest economies in the world based on GDP, year-by-year from 1961 to 2017. A few interesting observations:

1. The global slowdown in the early 1980s.

2. China’s ranking in the world’s ten largest economies has sure bounced around a lot. It was the world’s fifth largest economy in 1962 and remained in the top ten economies until it dropped out in 1978 and 1979,

Posted by at 9:42 PM

Labels: Macro Demystified

Balancing Financial Stability and Housing Affordability: The Case of Canada

From the IMF’s latest report on Canada:

“Housing market imbalances are a key source of systemic risk and can adversely affect housing affordability. This paper utilizes a stylized model of the Canadian economy that includes policymakers with differing objectives—macroeconomic stability, financial stability, and housing affordability. Not surprisingly, when faced with multiple objectives, deploying more policy instruments can lead to better outcomes. The results show that macroprudential policy can be more effective than policies based on adjusting propertytransfer taxes because property-tax policy entails excessive volatility in tax rates. They also show that if property-transfer taxes are used as a policy instrument, taxes targeted at a broader-set of homebuyers can be more effective than measures targeted at a smaller subset of homebuyers, such as nonresident homebuyers.”

From the IMF’s latest report on Canada:

“Housing market imbalances are a key source of systemic risk and can adversely affect housing affordability. This paper utilizes a stylized model of the Canadian economy that includes policymakers with differing objectives—macroeconomic stability, financial stability, and housing affordability. Not surprisingly, when faced with multiple objectives, deploying more policy instruments can lead to better outcomes. The results show that macroprudential policy can be more effective than policies based on adjusting propertytransfer taxes because property-tax policy entails excessive volatility in tax rates.

Posted by at 9:49 AM

Labels: Global Housing Watch

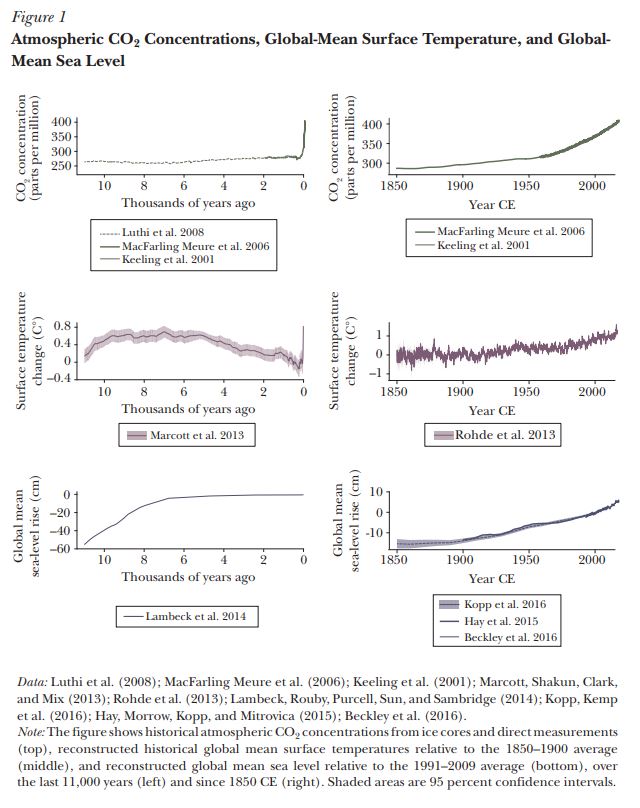

An Economist’s Guide to Climate Change Science

From the latest issue of the Journal of Economic Perspectives by Solomon Hsiang and Robert E. Kopp:

“Humans have engaged in large-scale transformation of natural systems for millennia. Stone Age hunting technologies led to extinctions of large mammals; agricultural revolutions transformed forests into farmlands; pursuit of minerals has carved the earth’s surface; dams and reservoirs now manipulate the flow of almost all rivers; and synthetic fertilizers now flood the nitrogen cycle. But among these transformations, the restructuring of the global carbon cycle and the accompanying alteration of the climate stands apart in its sheer scale, complexity, and economic significance. Essentially all humans that have ever lived contributed, in their own small ways, to reshaping this planetary-scale system. Thousands of years of forest clearance may have added hundreds of billions of tons of carbon to the atmosphere. In the industrial era, every home lit by a coal or natural gas-fired power plant and every petroleum-powered train, plane, and motor vehicle has contributed to the net accumulation of carbon dioxide in the atmosphere. The average human contributes about 5 tonnes of carbon dioxide (CO2) every year (Le Quéré et al. 2018), about a quarter of which will remain in the atmosphere for well over a millennium (Archer et al. 2009).

(…)

The goal of this article is to provide a brief introduction to the physical science of climate change, aimed towards economists. We begin by describing the physics that controls global climate, how scientists measure and model the climate system, and the magnitude of human-caused emissions of carbon dioxide. We then summarize many of the climatic changes of interest to economists that have been documented and that are projected in the future. We conclude by highlighting some key areas in which economists are in a unique position to help

climate science advance. An important message from this final section, which we believe is deeply underappreciated among economists and thus highlight here, is that all climate change forecasts rely heavily and directly on economic forecasts for the world. On timescales of a half-century or longer, the largest source of uncertainty in climate science is not physics, but economics (Hawkins and Sutton 2009).”

From the latest issue of the Journal of Economic Perspectives by Solomon Hsiang and Robert E. Kopp:

“Humans have engaged in large-scale transformation of natural systems for millennia. Stone Age hunting technologies led to extinctions of large mammals; agricultural revolutions transformed forests into farmlands; pursuit of minerals has carved the earth’s surface; dams and reservoirs now manipulate the flow of almost all rivers; and synthetic fertilizers now flood the nitrogen cycle.

Posted by at 9:45 AM

Labels: Energy & Climate Change

Sunday, November 4, 2018

Fall 2018 Journal of Economic Perspectives Available On-line

From a new post by Timothy Taylor:

“I was hired back in 1986 to be the Managing Editor for a new academic economics journal, at the time unnamed, but which soon launched as the Journal of Economic Perspectives. The JEP is published by the American Economic Association, which back in 2011 decided–to my delight–that it would be freely available on-line, from the current issue back to the first issue. Here, I’ll start with Table of Contents for the just-released Fall 2018 issue, which in the Taylor household is known as issue #126. Below that are abstracts and direct links for all of the papers. I may blog more specifically about some of the papers in the next week or two, as well.”

From a new post by Timothy Taylor:

“I was hired back in 1986 to be the Managing Editor for a new academic economics journal, at the time unnamed, but which soon launched as the Journal of Economic Perspectives. The JEP is published by the American Economic Association, which back in 2011 decided–to my delight–that it would be freely available on-line, from the current issue back to the first issue.

Posted by at 9:18 PM

Labels: Macro Demystified

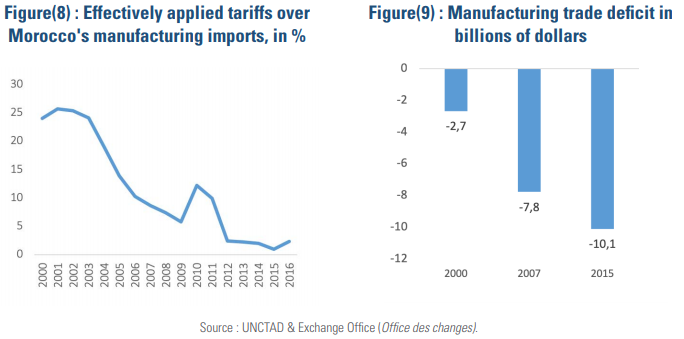

Deindustrialization and Employment in Morocco

A new OCP Policy Center policy brief shows that “downward trend of employment in manufacturing in Morocco is due primarily to labor productivity improvement and that the increased deficit in manufacturing trade also plays an important role. While recognizing the crucial importance of a vibrant manufacturing sector in Morocco, this brief argues that Morocco cannot rely primarily on manufactures to “pull” labor out of agriculture. To provide more jobs, Moroccan policies should pay more attention to sectors which employ large numbers of people and where employment is expanding as a result of the ongoing structural transformation of the Moroccan economy.”

A new OCP Policy Center policy brief shows that “downward trend of employment in manufacturing in Morocco is due primarily to labor productivity improvement and that the increased deficit in manufacturing trade also plays an important role. While recognizing the crucial importance of a vibrant manufacturing sector in Morocco, this brief argues that Morocco cannot rely primarily on manufactures to “pull” labor out of agriculture. To provide more jobs, Moroccan policies should pay more attention to sectors which employ large numbers of people and where employment is expanding as a result of the ongoing structural transformation of the Moroccan economy.”

Posted by at 9:15 PM

Labels: Inclusive Growth

Subscribe to: Posts