Thursday, January 3, 2019

Countries are advancing efforts to stop criminals from laundering their trillions

From Finance & Development:

“Al Capone had a problem: he needed a way to disguise the enormous amounts of cash generated by his criminal empire as legitimate income. His solution was to buy all-cash laundromats, mix dirty money in with clean, and then claim that washing ordinary Americans’ shirts and socks, rather than gambling and bootlegging, was the source of his riches.

Almost a century later, the basic concept of money laundering is the same, but its scale and complexity have grown considerably. Were Capone alive today, he would have to run his washers and dryers around the clock to keep pace with demand; the United Nations recently estimated that the criminal proceeds laundered annually amount to between 2 and 5 percent of global GDP, or $1.6 to $4 trillion a year.

Threat to stability

Money laundering is what enables criminals to reap the benefits of their crimes, including corruption, tax evasion, theft, drug trafficking, and migrant smuggling. Many of these crimes pose a direct threat to economic stability. Corruption and tax evasion make it difficult for governments to deliver sustainable and inclusive growth by diminishing the resources available for productive purposes, such as building roads, schools, and hospitals. Criminal activity undermines state authority and the rule of law while squeezing out legitimate economic activity. And money laundering may create asset bubbles in markets like real estate, a common vehicle.

A recent example illustrates the point. A Guinean minister helped a foreign company obtain important mining concessions in exchange for $8.5 million in bribes. Falsely reporting that money as income from consulting work and private land sales, the minister transferred it to the United States and bought a luxury estate in New York. But his effort to turn ill-gotten gains into a seemingly legitimate asset was ultimately unsuccessful; last year, he was convicted of money laundering.

In some ways, expensive homes are the modern mobster’s collection of laundromats. A public advisory issued by US authorities last year indicated that over 30 percent of high-value, all-cash real estate purchases in New York City and several other major metropolitan areas were conducted by individuals already suspected of involvement in questionable dealings. The governments of Australia, Austria, Canada, and other countries have concluded that their own real estate markets could also be used to invest and launder dirty money.

Terrorism financing

More worrying still, dirty money—along with clean—may be a source of funding for terrorism and the proliferation of weapons of mass destruction. Terrorist groups need money, lots of it, to compensate fighters and their families; buy weapons, food, and fuel; and bribe crooked officials. Similarly, proliferation does not come cheap. For example, North Korea has reportedly devoted a substantial portion of its scarce resources to developing nuclear weapons.”

Continue reading here.

Rhoda Weeks-Brown

From Finance & Development:

“Al Capone had a problem: he needed a way to disguise the enormous amounts of cash generated by his criminal empire as legitimate income. His solution was to buy all-cash laundromats, mix dirty money in with clean, and then claim that washing ordinary Americans’ shirts and socks, rather than gambling and bootlegging, was the source of his riches.

Almost a century later, the basic concept of money laundering is the same,

Posted by at 9:43 AM

Labels: Inclusive Growth

Friday, December 28, 2018

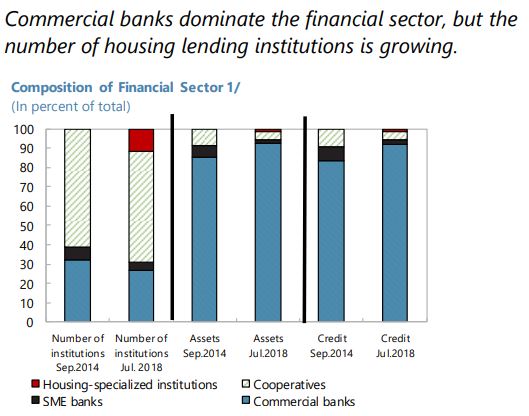

Housing Market in Bolivia

The IMF’s latest report on Bolivia says:

“Credit quotas should be relaxed to limit poor-quality credit growth. Interest caps should also be removed so that lending decisions better reflect intrinsic risks. This would remove distortions in the allocation of credit and support desirable allocation of resources in support of growth. ASFI is urged to monitor closely capital quality for its ability to absorb potential shocks and to scrutinize possible risks arising from rapid credit growth to housing. In this context, the Fund welcomes the opportunity to assist the authorities to prepare a real estate price index and urges rapid progress.”

The IMF’s latest report on Bolivia says:

“Credit quotas should be relaxed to limit poor-quality credit growth. Interest caps should also be removed so that lending decisions better reflect intrinsic risks. This would remove distortions in the allocation of credit and support desirable allocation of resources in support of growth. ASFI is urged to monitor closely capital quality for its ability to absorb potential shocks and to scrutinize possible risks arising from rapid credit growth to housing.

Posted by at 10:15 AM

Labels: Global Housing Watch

Top Ten Posts of 2018

As 2018 draws to a close, below is our list of the top ten blogs of the year.

- RIP Herman Stekler, A Forecasting Giant

- RIP Deena Khatkhate, far-sighted IMF and RBI economist

- How Well Do Economists Forecast Recessions? A Groundhog Day Update

- Economic Growth from Octavian to Obama

- Affordable Housing: Views from Albert Saiz

- The Distribution of Gains from Globalization

- Housing View – January 5, 2018 [2018 AEA Annual Meeting Special Edition]

- Household Credit, Global Financial Cycle, and Macroprudential Policies: Credit Register Evidence from an Emerging Country

- Understanding Singapore’s Housing Market

- Growth and well-being: policy should not be based on GDP alone

Photo by Colton Duke

As 2018 draws to a close, below is our list of the top ten blogs of the year.

- RIP Herman Stekler, A Forecasting Giant

- RIP Deena Khatkhate, far-sighted IMF and RBI economist

- How Well Do Economists Forecast Recessions? A Groundhog Day Update

- Economic Growth from Octavian to Obama

- Affordable Housing: Views from Albert Saiz

- The Distribution of Gains from Globalization

- Housing View – January 5,

Posted by at 9:39 AM

Labels: Macro Demystified

Thursday, December 27, 2018

Top charts of 2018

From Economic Policy Institute:

“Twelve charts that show how policy could reduce inequality—but is making it worse instead

With the unemployment rate at 4 percent or below for eight consecutive months, 2018 appears to be the year when the economy finally became healthy again. But while low unemployment is good news, it doesn’t tell the whole story of how typical families are faring in the current economy.

As the economy normalizes following a long, slow recovery from the Great Recession, we are quickly resuming our prerecession course of rising inequality. The fruits of economic growth are bypassing typical families and going straight into the hands of the already-rich.

Our current policy trajectory is doing nothing to reverse the trend of inequality. But it’s doing plenty to widen it. This year’s edition of Top Charts highlights how policy choices continue to exacerbate inequality and how we can achieve more broadly shared prosperity through better policy choices.

Continue reading here.

From Economic Policy Institute:

“Twelve charts that show how policy could reduce inequality—but is making it worse instead

With the unemployment rate at 4 percent or below for eight consecutive months, 2018 appears to be the year when the economy finally became healthy again. But while low unemployment is good news, it doesn’t tell the whole story of how typical families are faring in the current economy.

As the economy normalizes following a long,

Posted by at 12:07 PM

Labels: Macro Demystified

Transmission of U.S. Monetary Policy to Commodity Exporters and Importers

From a new working paper by Myunghyun Kim:

“This paper studies international transmission of U.S. monetary policy shocks to commodity exporters and importers. After first showing empirically that the shocks have stronger effects on commodity exporters than on importers, I then augment a standard three-country model to include commodities. Consistent with the empirical evidence, the model

indicates that an expansionary monetary policy shock to the U.S. increases the aggregate output of commodity exporters by more than that of importers. This is because the increased U.S. aggregate demand triggered by the shock leads to greater U.S. demand for commodities and higher real commodity prices, and thus the exports of commodity exporters increase relative to those of commodity importers. Furthermore, I show that if commodity exporters’ currencies are pegged to the U.S. dollar, then the U.S. monetary policy shocks have stronger spillovers to commodity exporters and importers. In the event that the U.S. becomes a net energy exporter, the shocks will have weaker effects on commodity exporters and stronger impacts on importers.”

From a new working paper by Myunghyun Kim:

“This paper studies international transmission of U.S. monetary policy shocks to commodity exporters and importers. After first showing empirically that the shocks have stronger effects on commodity exporters than on importers, I then augment a standard three-country model to include commodities. Consistent with the empirical evidence, the model

indicates that an expansionary monetary policy shock to the U.S. increases the aggregate output of commodity exporters by more than that of importers.

Posted by at 12:03 PM

Labels: Energy & Climate Change

Subscribe to: Posts