Monday, June 17, 2019

Housing Market in Ireland

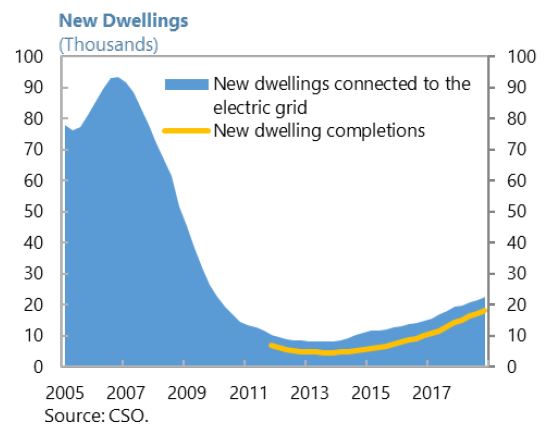

From the IMF’s latest report on Ireland:

“Unlike during the pre-crisis period, rising housing prices have not been fueled by excessive credit but rather by a lagging supply response to rising demand. Robust job creation, rising wages, low interest rates, and population growth have all contributed to a strong recovery in housing demand since 2013. The supply of housing, however, has not kept pace. The main factors that have prevented a faster expansion in housing supply are constraining regulations, weaknesses in the zoning and planning process, financial difficulties of construction firms, skills shortages in the construction sector, and land hoarding.

The government has taken several measures to increase housing supply, develop the rental market, and improve affordability.1 The Rebuilding Ireland Action Plan for Housing and Homelessness, announced in July 2016, seeks to double the annual level of residential construction to 25,000 homes by 2020, deliver an additional 50,000 social housing units in the period to 2021, and meet the housing needs of an additional 87,000 households through housing assistance schemes. Home Building Finance Ireland, a newly established state lender for financially constrained developers, aims to deliver up to 7,500 new homes over the next five years, financed by a €750 million investment from the Ireland Strategic Investment Fund. Other initiatives include an infrastructure fund designed to provide local public infrastructure to facilitate housing development, and a new fast-track planning process for large-scale housing developments.

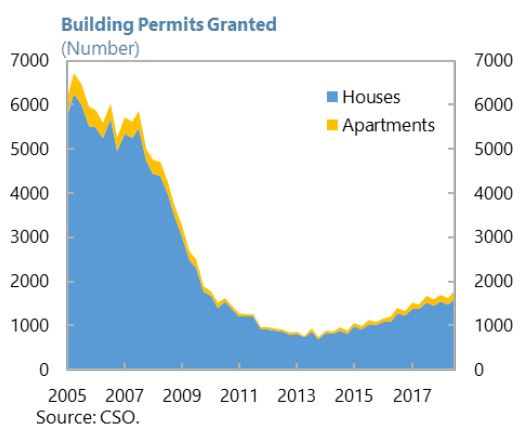

There are indications that the housing supply will continue to expand. The number of new dwellings connected to the electric grid increased by 17 percent in 2018—the fifth consecutive year of growth, albeit from a low base—while new dwelling completions have also grown rapidly. Forward-looking indicators point to further growth. Building permits granted for the construction of houses and apartments increased by 8.5 percent year-on-year in 2018:Q3, and employment continues to increase in the construction sector.”

From the IMF’s latest report on Ireland:

“Unlike during the pre-crisis period, rising housing prices have not been fueled by excessive credit but rather by a lagging supply response to rising demand. Robust job creation, rising wages, low interest rates, and population growth have all contributed to a strong recovery in housing demand since 2013. The supply of housing, however, has not kept pace. The main factors that have prevented a faster expansion in housing supply are constraining regulations,

Posted by at 10:30 AM

Labels: Global Housing Watch

Friday, June 14, 2019

Some Snapshots of the Global Energy Situation

From Conversable Economist:

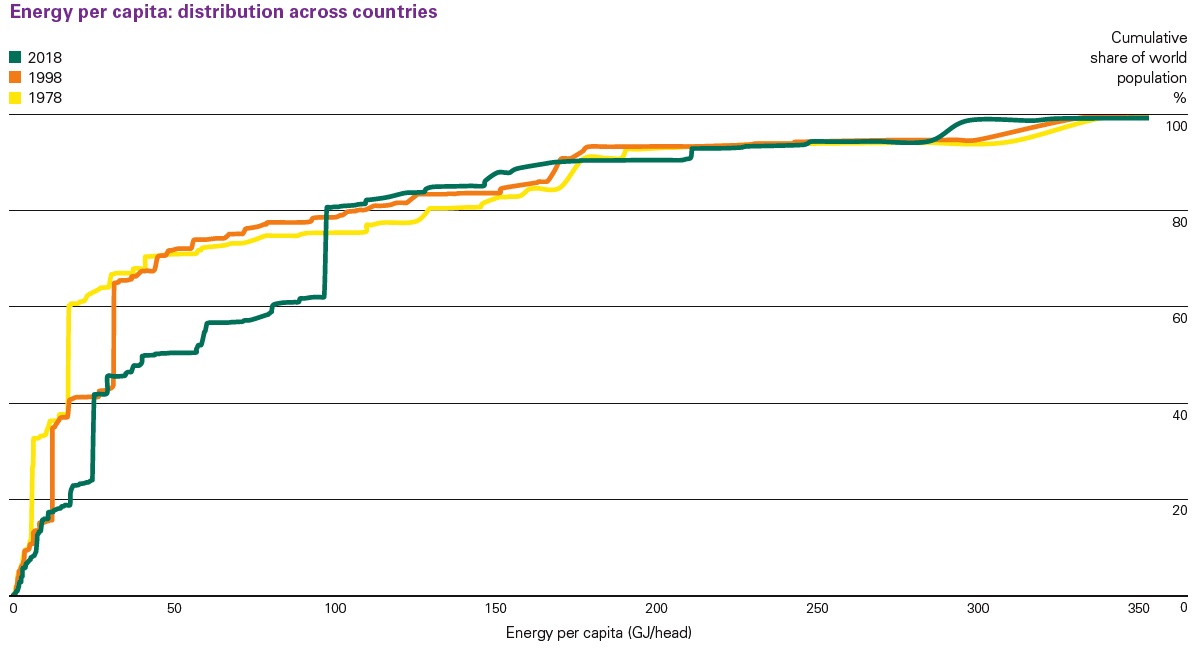

“Global primary energy grew by 2.9% in 2018 – the fastest growth seen since 2010. This occurred despite a backdrop of modest GDP growth and strengthening energy prices. At the same time, carbon emissions from energy use grew by 2.0%, again the fastest expansion for many years, with emissions increasing by around 0.6 gigatonnes. That’s roughly equivalent to the carbon emissions associated with increasing the number of passenger cars on the planet by a third.” Spencer Dale offers these and other insights in his introduction to the the 2019 BP Statistical Review of World Energy. It’s one of those books of charts and tables I try to check each year just to keep my personal perceptions of economic patterns connected to actual statistics. Here are a few figures that jumped out at me.

One main drive of the rise in world energy use is economic growth in emerging market countries. The horizontal axis of this figure shows average energy use per person. The vertical axis shows the cumulative share of total world population. The yellow line shows the pattern for 1978, while the green line shows four decades later in 2018.”

Continue reading here.

From Conversable Economist:

“Global primary energy grew by 2.9% in 2018 – the fastest growth seen since 2010. This occurred despite a backdrop of modest GDP growth and strengthening energy prices. At the same time, carbon emissions from energy use grew by 2.0%, again the fastest expansion for many years, with emissions increasing by around 0.6 gigatonnes. That’s roughly equivalent to the carbon emissions associated with increasing the number of passenger cars on the planet by a third.”

Posted by at 2:46 PM

Labels: Energy & Climate Change

Thursday, June 13, 2019

Housing Market in Czech Republic

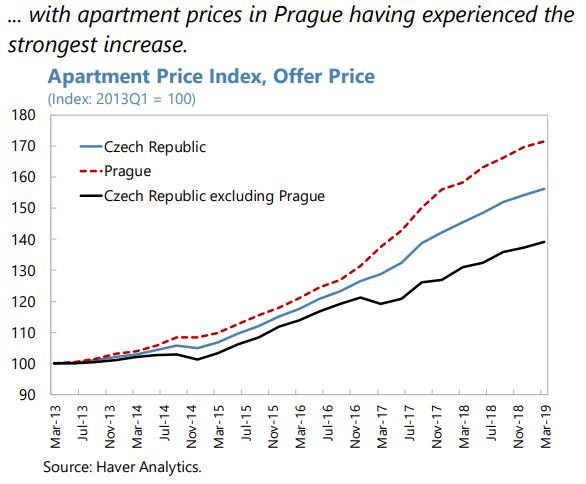

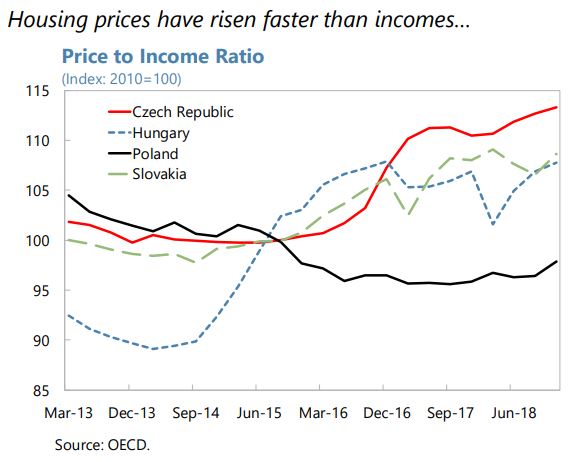

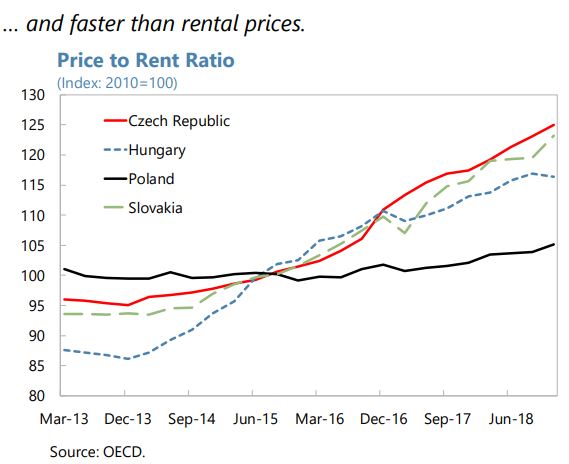

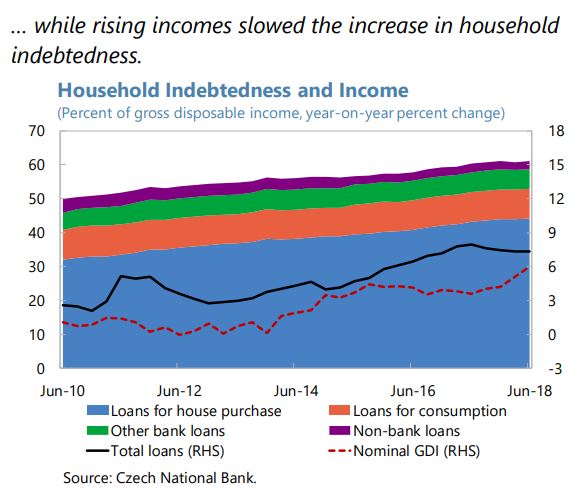

From the IMF’s latest report on Czech Republic:

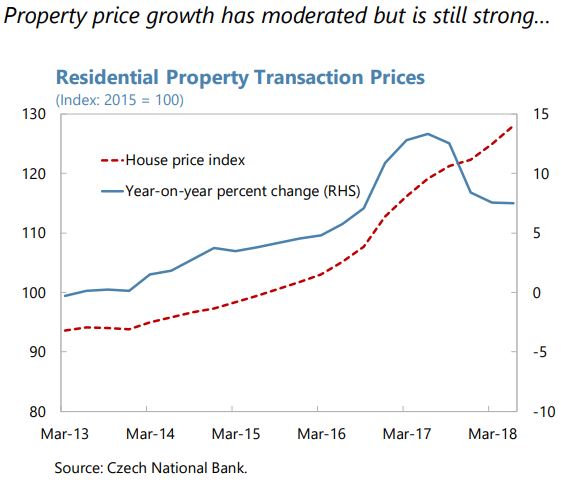

“The housing market remains pressured.

Despite a recent deceleration, house price growth was still among the 5 highest in the EU in 2018, outpacing wage and income growth (Figure 7). In Prague, where most property transactions take place, offered prices for apartments have increased by 44 percent in the three years from 2016 to 2018. The price-to-income ratio has increased by a cumulative 12.6 percent between 2015: Q4 and 2018: Q4, after having been stable over the preceding 5 years. House price increases have also made a substantial contribution to the measure of CPI targeted by the CNB.

Private nonfinancial sector credit accelerated from the previous year, growing ahead of nominal incomes. This was driven primarily by mortgage credit, which continues to grow at a high rate (…). But new mortgage volumes are decreasing amid increasing lending rates and tighter macroprudential borrower recommendations. Nonfinancial corporate lending growth also increased in 2018.”

From the IMF’s latest report on Czech Republic:

“The housing market remains pressured.

Despite a recent deceleration, house price growth was still among the 5 highest in the EU in 2018, outpacing wage and income growth (Figure 7). In Prague, where most property transactions take place, offered prices for apartments have increased by 44 percent in the three years from 2016 to 2018. The price-to-income ratio has increased by a cumulative 12.6 percent between 2015: Q4 and 2018: Q4,

Posted by at 2:40 PM

Labels: Global Housing Watch

Housing View – June 14, 2019

On cross-country:

- Global House Price Index – Q1 2019 – Knight Frank

- Literature Review Article: Recent Developments in the Economics of Housing – Elgar Research Reviews in Economics

- The evolution of prime property pricing across global cities – Knight Frank

- Recent changes in housing policies and their distributional impact across Europe – EURMOD

On the US:

- Fix Mortgage Finance, or We’ll Do It for You, Regulator Tells Congress – Wall Street Journal

- Landmark Deal Reached on Rent Protections for Tenants in N.Y. – New York Times

- We need more housing. Local governments are standing in the way – Washington Post

- The Largest Co-Living Building in the World Is Coming to San Jose – Citylab

- The surprisingly effective pilot program stopping real estate money laundering in the US – Quartz

- Affordable Housing Is Not an Easy Fix, Lens Says – UCLA

- Recalibrating Local Politics to Increase the Supply of Housing – Cato Institute

- Housing Lab helps startups that aim to make housing less expensive – UC Berkely

- Housing Crunch Sends Bigger Populations to Smaller Towns – The Pew Charitable Trusts

On other countries:

- [Canada] Canada’s house price boom takes off – Global Property Guide

- [China] Chinese city tells property developers to cease offering drastic price cuts – Reuters

- [China] China’s debt disease might wreck its uncrashable housing market – Quartz

- [Finland] Finland’s housing market remains weak – Global Property Guide

- [Greece] Greek housing sector rebound gains pace as economy recovers – Reuters

- [Hong Kong] The Trade War Could Pop Hong Kong’s Property Bubble – Bloomberg

- [Indonesia] The housing market in Indonesia rarely makes big moves – Global Property Guide

- [Latvia] Latvia’s house prices are now falling – Global Property Guide

- [New Zealand] New Zealand’s house prices rising strongly again – Global Property Guide

- [Thailand] Thailand’s modest house price rises – Global Property Guide

- [Spain] Recent housing market developments in Spain – Banco de España

- [Spain] The Spanish housing market: is it fundamentally broken? – IDEAS

On cross-country:

- Global House Price Index – Q1 2019 – Knight Frank

- Literature Review Article: Recent Developments in the Economics of Housing – Elgar Research Reviews in Economics

- The evolution of prime property pricing across global cities – Knight Frank

- Recent changes in housing policies and their distributional impact across Europe – EURMOD

On the US:

- Fix Mortgage Finance,

Posted by at 1:40 PM

Labels: Global Housing Watch

Wednesday, June 12, 2019

House Prices in Norway

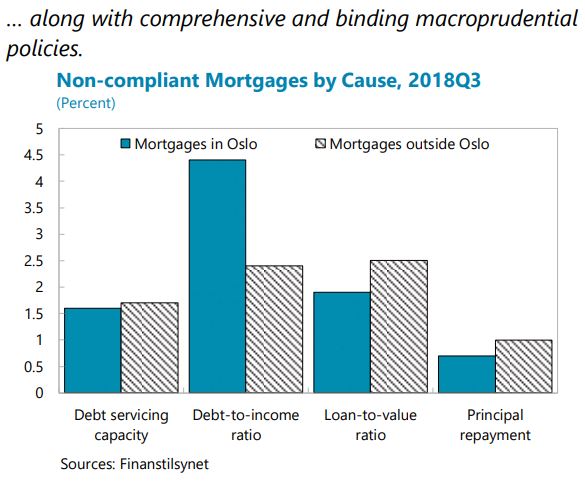

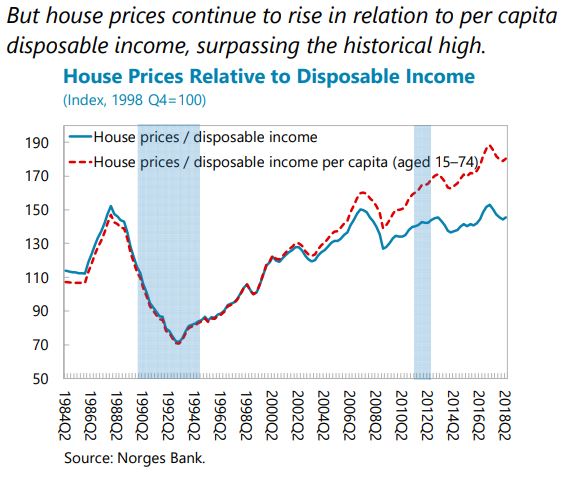

From the IMF’s latest report on Norway:

- “House prices remain overvalued, albeit less so than last year, and household debt continues to rise from an already elevated level (…). The house price moderation discussed earlier has improved housing affordability and correspondingly lowered the risks of a price crash. Nevertheless, house prices remain above fundamentals per staff estimates (0–10 percent at the national level and 5–20 percent in Oslo). Moreover, household indebtedness continues to increase from already high levels, leaving households vulnerable to sharp interest rate rises. Besides mortgages, the rapid growth of consumer credit also warrants close watch, even if it starts from a small base.

- Risks from commercial real estate are rising (…). Commercial real estate prices have increased by about 60 percent since 2000 in real terms, and more than twice that in prime Oslo. Although yields in Norway are not especially low, Oslo’s prime market has the lowest yield compression among major European cities. Banks have substantial exposure to CRE loans25 which account for 15 percent of banks’ loan portfolio (23 percent of GDP), higher than peer countries.”

- The current prudential toolkit to mitigate financial stability risks is quite comprehensive and should not be loosened at this stage.

Residential housing: The current mortgage regulations, renewed last year, consist of both capital and borrower-based measures such as maximum LTV and DTI ratios, and are welltargeted to areas with higher risks such as Oslo. Together, they have contributed to containing the incidence of risky mortgages, not least in the capital. Given that prices are still overvalued, and that household debt continues to rise, the regulations should be extended as is when reviewed at year-end, barring large unexpected developments in the coming months. The tighter limits for Oslo should be preserved. As recommended in previous years, the mortgage regulations could also be made permanent; the parameters could then be adjusted as needed over the financial cycle.”

From the IMF’s latest report on Norway:

- “House prices remain overvalued, albeit less so than last year, and household debt continues to rise from an already elevated level (…). The house price moderation discussed earlier has improved housing affordability and correspondingly lowered the risks of a price crash. Nevertheless, house prices remain above fundamentals per staff estimates (0–10 percent at the national level and 5–20 percent in Oslo). Moreover, household indebtedness continues to increase from already high levels,

Posted by at 2:22 PM

Labels: Global Housing Watch

Subscribe to: Posts