Monday, January 21, 2019

Predicting recessions using term spread at the zero lower bound: The case of the euro area

From a new VOX post:

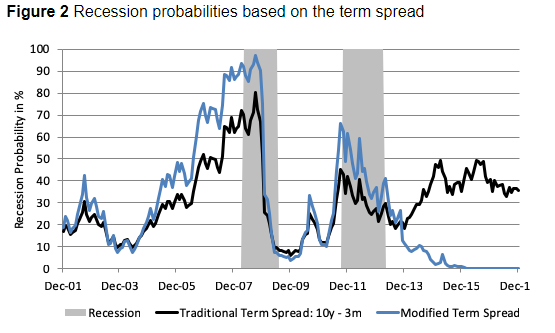

“The flattening of the US yield curve has left academics, central bankers and market commentators divided, with one camp interpreting it as a sign of impending recession (in line with historical patterns), and the other camp arguing that this time is different given unprecedented changes in monetary policy and other structural forces. This column argues that the ECB’s quantitative easing programme undermined the performance of term spreads as predictors of recessions. It suggests and tests a modified term spread and several other variables that are more successful at predicting recessions. ”

“This revised version of the term spread successfully predicts the 2011 recession with a lead time of two months, and signals an average recession probability above 50% during the first half of the recession. It also sees recession probabilities falling to 1% for the period between January 2015 and December 2017, which compares to an average recession signal of 40%, indicated by the traditional term spread over the same period (Figure 2). Given this, we find that switching to the shadow rate in face of the zero lower bound brings a valuable perspective on the term spread as an input factor to recession models.”

Posted by at 12:54 PM

Labels: Inclusive Growth

Subscribe to: Posts