Thursday, December 5, 2019

Accuracy and Determinants of Self-Assessed Euro Area House Prices

From an ECB working paper by Julien Le Roux and Moreno Roma:

“Using microdata from the second wave of the Household Finance and Consumption Survey, we investigate the accuracy of property values estimated by homeowners – so called “self-assessed” house prices – and explore the drivers of possible deviations of these prices from official hedonic house price indices. We find evidence that euro area homeowners overestimate the value of their properties by around 9%. Across the largest euro area countries, the overestimation lies in a range between 3.2% in Germany and 22% in Italy. Household characteristics, including the level of indebtedness, appear to explain significant discrepancies between hedonic and self-assessed house price indices, while the limited available data related to property characteristics are generally not affecting this gap. For the euro area, we find that higher self-assessed house prices are associated with a mild increase in consumption expenditures.”

From an ECB working paper by Julien Le Roux and Moreno Roma:

“Using microdata from the second wave of the Household Finance and Consumption Survey, we investigate the accuracy of property values estimated by homeowners – so called “self-assessed” house prices – and explore the drivers of possible deviations of these prices from official hedonic house price indices. We find evidence that euro area homeowners overestimate the value of their properties by around 9%.

Posted by at 3:42 PM

Labels: Global Housing Watch

Housing Market in Hungary

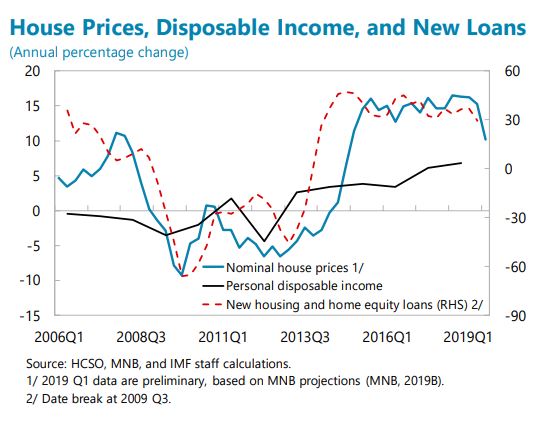

From the IMF’s latest report on Hungary:

“Efforts to scale back house purchase incentives and to address supply constraints are needed to mitigate market pressures. In 2018, housing price growth was in double digits, especially in Budapest, partly supported by high wage growth, fiscal incentives, and labor scarcity in the construction sector (Figure 3). Budapest house prices appear high compared to fundamentals. Given that a large part of purchases is paid for with private savings, including by foreign citizens, and is done for investment purposes, tightening of macroprudential measures (loan-to-value and debt service-to-income (DSTI) may not be sufficient to contain house price inflation, but can reduce the likelihood of risky mortgages. Moderating price increases would therefore be helped by reviewing the various fiscal incentives for house purchases, basing them on means-testing and targeting, reducing impediments to doing business to spur construction, improving transportation network and commuting options, and improving urban planning to increase housing supply over time. In the context of money laundering risks in the sector, staff also encouraged the authorities to continue their AML/CFT efforts, as Hungary remains on enhanced follow-up based on Moneyval’s 2016 assessment, including by continuing to monitor large purchases of luxury real estate.

The authorities launched several initiatives to reduce the mortgage interest rate risk. While most new housing loans now have longer interest fixation periods—likely facilitated by the MNB Certified Consumer-Friendly Housing Loans and the DSTI requirements—there is still a high portion of existing housing loans with variable rates. The MNB thus agreed with banks that they inform their clients about the interest rate risk and offer to convert to fixed-rates.3 Thus far, the impact of this measure has been limited. To contain potential risks from FX exposure of some of the commercial real estate companies, the MNB has announced that beginning in 2020 a small riskweight would be also assigned to FX performing project loans when calculating the systemic risk buffer.

The authorities are monitoring housing prices, especially in Budapest, even though they are still much lower than in comparable cities in Western Europe. They also noted that assessment models do not capture the fact that many of these purchases are for investment and generate rental income. They agree that additional tightening of macro prudential measures is unlikely to have a significant impact. There is preliminary evidence that the introduction of the retail bond MÁP+ coincided with a decline in apartment sales transactions in Budapest. Some of the MNB’s proposals—included in the MNB’s Competitiveness Program, like tightening the rules for purchases of residences for investment purposes and expanding construction capacity, could help moderate the market.”

From the IMF’s latest report on Hungary:

“Efforts to scale back house purchase incentives and to address supply constraints are needed to mitigate market pressures. In 2018, housing price growth was in double digits, especially in Budapest, partly supported by high wage growth, fiscal incentives, and labor scarcity in the construction sector (Figure 3). Budapest house prices appear high compared to fundamentals. Given that a large part of purchases is paid for with private savings,

Posted by at 10:59 AM

Labels: Global Housing Watch

Wednesday, December 4, 2019

South and Midwest Regions are Gaining Larger Share of Homebuyers

From National Association of Realtors:

“The South and Midwest regions have accounted for an increasing fraction of existing home sales since 2012 while the shares of the North and West regions have declined, according to the October 2019 existing home sales estimates of the National Association of REALTORS®. The South region’s share of existing home sales increased from 36% in 2000 to 43% (as of October 2019), while the Northeast region’s share from 18% to 13% during the same period. The West region’s home sales share has slightly fallen from 23% to 21% while the Midwest region’s share has remained the same at 24%. However, since 2011, the Midwest region has been gaining market share, from 21% to 24%. The share of the West region rose to as high as 27% in 2011 but started declining in 2012, to just 21% in 2019.”

Continue reading here.

From National Association of Realtors:

“The South and Midwest regions have accounted for an increasing fraction of existing home sales since 2012 while the shares of the North and West regions have declined, according to the October 2019 existing home sales estimates of the National Association of REALTORS®. The South region’s share of existing home sales increased from 36% in 2000 to 43% (as of October 2019), while the Northeast region’s share from 18% to 13% during the same period.

Posted by at 10:29 AM

Labels: Global Housing Watch

Summer reading list for the Prime Minister 2019

From New Zealand Institute of Economic Research:

“Summer reading list for the Prime Minister 2019. Presented in alphabetical order by lead author:

- The Narrow Corridor: States, societies, and the fate of liberty, Daron Acemoglu & James A Robinson, 2019

- Fatal Necessity: British Intervention in New Zealand, 1830-847, Peter Adams, 1977

- Good economics for hard times: Better answers to our biggest problems, Abhijit V Banerjee and Esther Duflo, 2019

- The Sex Factor: How women made the West Rich, Victoria Bateman, 2019

- Tutira: The story of a New Zealand Sheep Station, Herbert Guthrie-Smith, 1921

- Confronting Inequality: How Societies Can Choose Inclusive Growth, Jonathan D Ostry, Prakash Loungani & Andrew Berg, 2019

- Island Time: New Zealand’s Pacific Future, Damon Salesa, 2017

- Economics for the Common Good, Jean Tirole, 2019

- Deep Medicine: How Artificial Intelligence Can Make Healthcare Human Again, Eric Topol, 2019″

From New Zealand Institute of Economic Research:

“Summer reading list for the Prime Minister 2019. Presented in alphabetical order by lead author:

- The Narrow Corridor: States, societies, and the fate of liberty, Daron Acemoglu & James A Robinson, 2019

- Fatal Necessity: British Intervention in New Zealand, 1830-847, Peter Adams, 1977

- Good economics for hard times: Better answers to our biggest problems, Abhijit V Banerjee and Esther Duflo,

Posted by at 10:28 AM

Labels: Inclusive Growth

Monday, December 2, 2019

Chile’s insurgency and the end of neoliberalism

From a VOX post by Sebastian Edwards:

“In a few decades, Chile experienced dramatic economic growth and the fastest reduction of inequality in the region. Yet, many Chilean citizens feel that inequality has greatly increased. Such feelings of ‘malestar’ triggered the violent social unrest of October 2019. This paper explains this seeming paradox by differentiating ‘vertical’ (income) inequality from ‘horizontal’ (social) inequality. It argues that the neoliberalism that created Chile’s economic growth is no longer effective and that Chile may be headed towards adopting a welfare state model.

The October 2019 social explosion in Chile took everyone by surprise. The scale of protests and the violence of demonstrators had no precedent. Millions of people marched demanding change. Protesters embraced all sort of causes but one demand united them: they were against inequality and privilege. The police responded with force and were accused of multiple human rights violations.

For a long time, economists praised Chile’s market-oriented reforms. Moreover, Chile’s political system and institutions were ranked highly by think tanks such as Freedom House (2019). However, many analysts pointed out that inequality was Chile’s Achilles heel (Edwards 2010). Its Gini coefficient is one of the highest in the OECD although it has declined rapidly; during the last two decades, there has been significant progress in social conditions.

Chile went from being the poorest country in a sample of Latin American countries (jointly with Peru) to having the highest GDP per capita in the region (Figure 1). In 2016, Chile’s Gini was equal to the median in the region (Figure 2). Chile is among the countries that reduced inequality the fastest since 2000: the Gini declined from 56 to 46 between 2000 and 2016 (Figure 3). Other indicators of social progress, such as the Human Development Index,1 rank Chile in the first place in Latin America.’

Continue reading here.

From a VOX post by Sebastian Edwards:

“In a few decades, Chile experienced dramatic economic growth and the fastest reduction of inequality in the region. Yet, many Chilean citizens feel that inequality has greatly increased. Such feelings of ‘malestar’ triggered the violent social unrest of October 2019. This paper explains this seeming paradox by differentiating ‘vertical’ (income) inequality from ‘horizontal’ (social) inequality. It argues that the neoliberalism that created Chile’s economic growth is no longer effective and that Chile may be headed towards adopting a welfare state model.

Posted by at 12:34 PM

Labels: Inclusive Growth

Subscribe to: Posts