Thursday, December 5, 2019

Housing Market in Hungary

From the IMF’s latest report on Hungary:

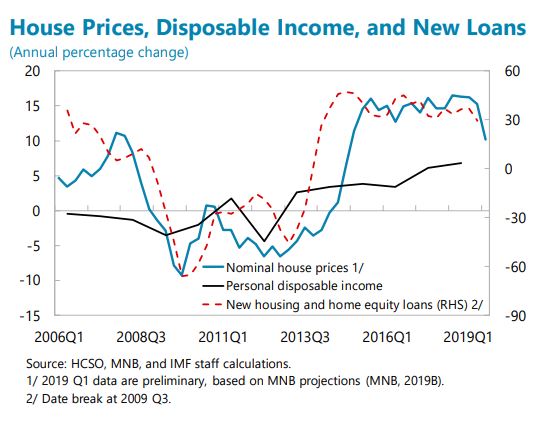

“Efforts to scale back house purchase incentives and to address supply constraints are needed to mitigate market pressures. In 2018, housing price growth was in double digits, especially in Budapest, partly supported by high wage growth, fiscal incentives, and labor scarcity in the construction sector (Figure 3). Budapest house prices appear high compared to fundamentals. Given that a large part of purchases is paid for with private savings, including by foreign citizens, and is done for investment purposes, tightening of macroprudential measures (loan-to-value and debt service-to-income (DSTI) may not be sufficient to contain house price inflation, but can reduce the likelihood of risky mortgages. Moderating price increases would therefore be helped by reviewing the various fiscal incentives for house purchases, basing them on means-testing and targeting, reducing impediments to doing business to spur construction, improving transportation network and commuting options, and improving urban planning to increase housing supply over time. In the context of money laundering risks in the sector, staff also encouraged the authorities to continue their AML/CFT efforts, as Hungary remains on enhanced follow-up based on Moneyval’s 2016 assessment, including by continuing to monitor large purchases of luxury real estate.

The authorities launched several initiatives to reduce the mortgage interest rate risk. While most new housing loans now have longer interest fixation periods—likely facilitated by the MNB Certified Consumer-Friendly Housing Loans and the DSTI requirements—there is still a high portion of existing housing loans with variable rates. The MNB thus agreed with banks that they inform their clients about the interest rate risk and offer to convert to fixed-rates.3 Thus far, the impact of this measure has been limited. To contain potential risks from FX exposure of some of the commercial real estate companies, the MNB has announced that beginning in 2020 a small riskweight would be also assigned to FX performing project loans when calculating the systemic risk buffer.

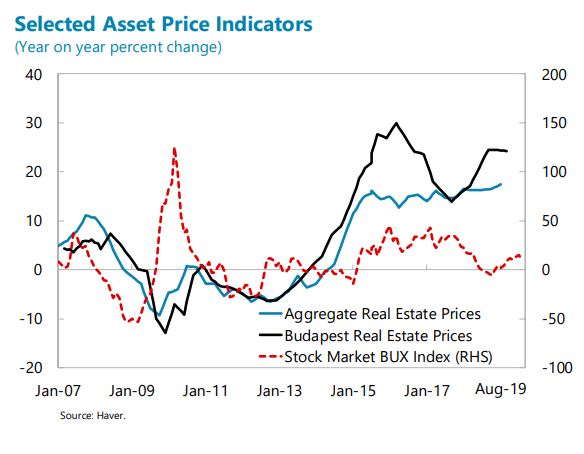

The authorities are monitoring housing prices, especially in Budapest, even though they are still much lower than in comparable cities in Western Europe. They also noted that assessment models do not capture the fact that many of these purchases are for investment and generate rental income. They agree that additional tightening of macro prudential measures is unlikely to have a significant impact. There is preliminary evidence that the introduction of the retail bond MÁP+ coincided with a decline in apartment sales transactions in Budapest. Some of the MNB’s proposals—included in the MNB’s Competitiveness Program, like tightening the rules for purchases of residences for investment purposes and expanding construction capacity, could help moderate the market.”

Posted by at 10:59 AM

Labels: Global Housing Watch

Subscribe to: Posts