Friday, August 19, 2022

Housing View – August 19, 2022

On cross-country:

- Reflections on the Evolution of the Housing Market in Latin America: Realities and Dreams – MIT

On the US:

- House Price Responses to Monetary Policy Surprises: Evidence from the U.S. Listings Data – Institute of Labor Economics

- Decline in Single-Family Permits in June 2022 – NAHB

- Why rent is damn high? – The Atlantic

- Renters Can’t Celebrate Softer Inflation Readings – Bloomberg

- New York City Rents Hit Record Highs Amid Nationwide Housing-Price Increases. Where would you pay over $4,000 a month for a one-bedroom? In 20 of New York City’s neighborhoods. – Wall Street Journal

- The Fed’s Damage to the Housing Market May Last Years. The central bank created major distortions in a market where many Americans have most of their wealth. Why? – Bloomberg

- U.S. Housing Affordability in June Was the Worst Since 1989. Record-high home prices combined with rising mortgage rates to push more buyers out of the market – Wall Street Journal

- Housing Slowdown Chills Investors Who Supercharged US Market. Institutional landlords and small flippers are starting to scale back as higher borrowing costs and slowing sales complicate their strategies. – Bloomberg

- 2 Reasons House Prices Will Start Falling Sooner Than Expected. Why house prices will be less “sticky” this time. – Real Estate Decoded

- Will Housing Prices Flatten — or Collapse? Home values are fast approaching the pace of gains that would be consistent with low inflation. But there’s a high risk of an overshoot. – Bloomberg

- Has COVID Reversed Gentrification in Major U.S. Cities? An Empirical Examination of Residential Mobility in Gentrifying Neighborhoods During the COVID-19 Crisis – Philadelphia Fed

- Rent Inflation Expected to Accelerate Then Moderate in Mid-2023 – Dallas Fed

- The Housing Market Is Bad but Not That Bad – New York Times

- Existing Home Sales Fall to Two-Year Low – NAHB

On China:

- The Bursting Chinese Housing Bubble Compounds Beijing’s Economic Woes. Home sales and prices are dropping in many cities across the country after rising for years, and the damage is spreading – Wall Street Journal

- What’s in Store for China’s Mortgage Market? – Carnegie Endowment for International Peace

- China Growth Slows Across All Fronts in July, Prompting Unexpected Rate Cut. Move comes after a month in which retail sales, property prices and youth unemployment worsened – Wall Street Journal

- China Home Prices Fall for 11th Month as Mortgage Crisis Deepens. Pace of decline widened to 0.11% after mortgage boycotts. Pressure on developers likely to remain due to covid lockdowns – Bloomberg

- China’s Housing Crisis Keeps Brewing in Beijing’s Weak Tea. There are reports of possible bond guarantees but no clear signs of any government action bold enough to revive the property market – Wall Street Journal

- As China’s Economy Stumbles, Homeowners Boycott Mortgage Payments. In a rare act of defiance, people across the country who bought property from indebted developers are refusing to repay loans on their unfinished apartments. – New York Times

On other countries:

- [Canada] Canadian Housing Correction Accelerates, Prices Seen Falling 25%. Desjardins updates forecasts after RBC warns of historic drop. Rate hikes drive rapid reversal of pandemic real-estate frenzy – Bloomberg

- [Denmark] Denmark’s Mortgage Market Is Luring Global Investors. Here’s Why – Bloomberg

- [Ireland] Irish house prices return to 2007 peak for first time – Reuters

- [New Zealand] RBNZ Chief Warns New Zealand Home Prices Will Keep Falling – Bloomberg

- [United Kingdom] Britain’s housing crisis — no longer a nation of homeowners? Four books look beyond the clichés of the property boom to examine the precarious reality of those forced to rely on an overgrown private rental market – FT

- [United Kingdom] Is the UK housing market at a turning point? Interest rates are rising to stem inflation and borrowing costs are increasing fast. Could this signal the end of spiralling house prices? – FT

- [United Kingdom] New UK lender plans 50-year fixed rate mortgages. Perenna secures licence from regulators to issue long-term home loans as inflation soars – FT

- [United Kingdom] UK house price growth slows sharply to 7.8% in June – ONS – Reuters

- [United Kingdom] UK house price growth slows to 7.8% in June, says ONS. Slower rate of increase skewed by tax break changes last year as housebuilder Persimmon warns of economic pressures on sector – FT

On cross-country:

- Reflections on the Evolution of the Housing Market in Latin America: Realities and Dreams – MIT

On the US:

- House Price Responses to Monetary Policy Surprises: Evidence from the U.S. Listings Data – Institute of Labor Economics

- Decline in Single-Family Permits in June 2022 – NAHB

- Why rent is damn high? – The Atlantic

- Renters Can’t Celebrate Softer Inflation Readings – Bloomberg

- New York City Rents Hit Record Highs Amid Nationwide Housing-Price Increases.

Posted by at 7:36 AM

Labels: Global Housing Watch

Wednesday, August 17, 2022

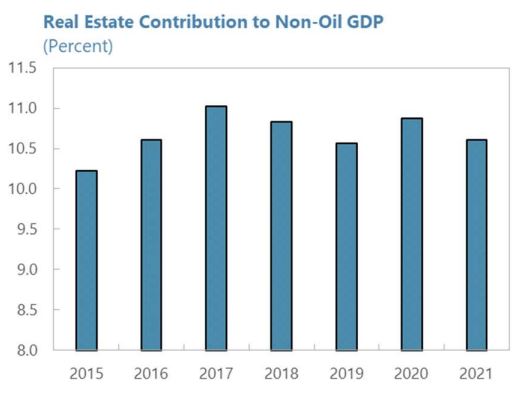

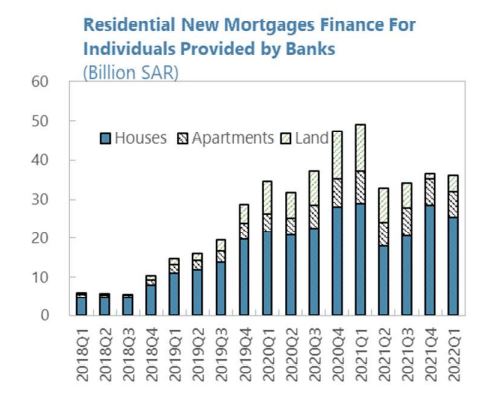

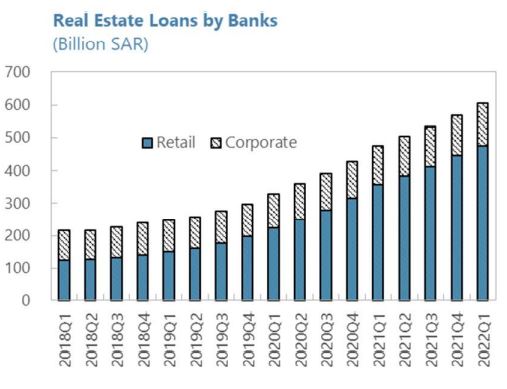

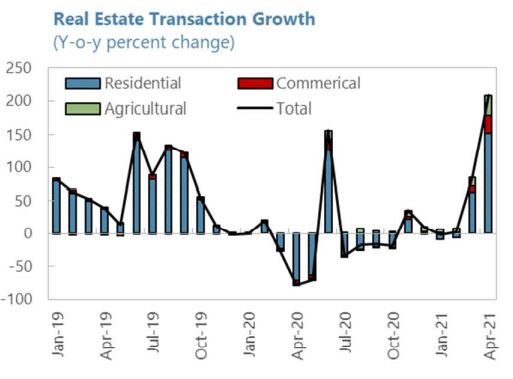

Housing Market in Saudi Arabia

Posted by at 8:41 AM

Labels: Global Housing Watch

Monday, August 15, 2022

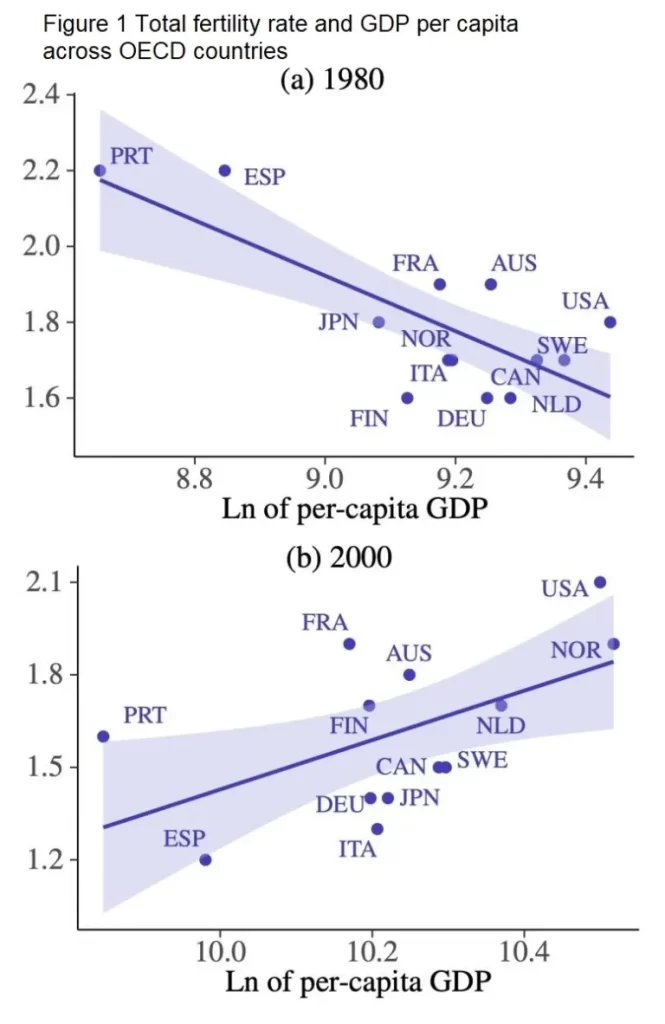

A Fertility Patterns Flip-flop

From Conversable Economist:

“For some decades now, the world has been following the patterns of a demographic transition with life expectancies rising and birth rates falling, as we head for a world where the elderly are a much larger share of the global population. However, Matthias Doepke, Anne Hannusch, Fabian Kindermann, and Michèle Tertilt argue that it’s time for “The New Economics of Fertility” (IZA Discussion Paper #15224, April 2022). For a short readable overview of the main themes, you can check their shorter discussion at the VoxEU website (June 11, 2022).

From the abstract of the academic paper, the authors write:

In this survey, we argue that the economic analysis of fertility has entered a new era. First-generation models of fertility choice were designed to account for two empirical regularities that, in the past, held both across countries and across families in a given country: a negative relationship between income and fertility, and another negative relationship between women’s labor force participation and fertility. The economics of fertility has entered a new era because these stylized facts no longer universally hold. In high-income countries, the income-fertility relationship has flattened and in some cases reversed, and the cross-country relationship between women’s labor force participation and fertility is now positive.

A couple of pictures may help, here. It used to be that countries with higher incomes had lower fertility rates, but among high-income countries, this pattern no longer holds. Here’s a figure taken from the VoxEU overview. The top panel shows that within the group of high-income countries in 1980, countries with higher per capita GDP had lower fertility, but by 2000, countries in this group with higher per capita income had higher fertility.”

Continue reading here.

From Conversable Economist:

“For some decades now, the world has been following the patterns of a demographic transition with life expectancies rising and birth rates falling, as we head for a world where the elderly are a much larger share of the global population. However, Matthias Doepke, Anne Hannusch, Fabian Kindermann, and Michèle Tertilt argue that it’s time for “The New Economics of Fertility” (IZA Discussion Paper #15224,

Posted by at 6:09 AM

Labels: Macro Demystified

Friday, August 12, 2022

Housing View – August 12, 2022

On cross-country:

- Newsletter on credit risk: real estate and leveraged lending – BIS

- Beyond China: Here Are the Next Real Estate Markets to Drop – Barron’s

- Where Should Affluent People Live? it’s not a simple question – Freddie deBoer

On the US:

- Zillow Sees Slowing Demand for Ads in Housing Downturn. Shares fall after earnings forecast misses analyst estimates. Piper Sandler’s Champion says it’s ‘rough’ in real estate now – Bloomberg

- Zillow economists: Here’s the home price shift coming for your local housing market in 2023 – Fortune

- Soaring rent prices have advocates calling on White House to intervene. A coalition of tenant unions, community organizations and legal groups is calling on the Biden administration to launch a full government response to lower rent inflation. – Washington Post

- How big is the housing shortage? – Market Urbanism

- The Snowballing US Rental Crisis Is Sparing Nowhere and No One. Renters across cities and income brackets are struggling to find new homes or pay for the ones they already live in. – Bloomberg

- Housing Affordability Falls to Lowest Level Since Great Recession – NAHB

- Lumber Futures Hit Two-Week High as Canada Cuts Wood Output. West Fraser shutters 2.5% of its North America capacity. Lumber prices may have reached bottom for now, analyst says – Bloomberg

- Housing Solutions Matchmaker Tool – National Association of Counties

- A Quick Note on the GNM – GSE Early Delinquency Gap – Recursion

- Current State of the Housing Market – Calculated Risk

- Mortgage Rates Swing Back Up, Hitting 5.22% in Volatile Market. Housing market is becoming more balanced, Freddie Mac says. Mortgage rates increase for first time in three weeks – Bloomberg

On China:

- China’s mortgage boycotts are a symptom of a broader crisis. The real threat to developers is falling sales – The Economist

- China Property Woes Spark Longest Mortgage Debt Halt Since 2015. Sales of residential mortgage-backed notes set for record drop. Plummeting home sales, developers’ cash crunch weaken demand – Bloomberg

- China property crisis: Why homeowners stopped paying their mortgages – BBC

On other countries:

- [Australia] Why soaring rates are not scaring off property investors. Rising rents and record-low vacancy rates are attracting buyers seeking higher yields and long-term capital growth. – Financial Review

- [India] India’s Top Mortgage Lender Signs ‘World’s Biggest’ Social Loan. HDFC completes $1.1 billion loan to finance affordable housing. HDFC prices social loan at margin of 90 basis points over SOFR – Bloomberg

- [India] Insecure property rights and the housing market: Explaining India’s housing vacancy paradox – Journal of Urban Economics

- [New Zealand] New Zealand House Prices Fall for First Time in 11 Years – Bloomberg

- [Sweden] Stockholm Apartment Prices Fall Most Since Pre-Covid Era – Bloomberg

- [United Kingdom] UK House Prices Fall for First Time in a Year as Crisis Bites. Buyers feeling the effects of inflation, higher mortgage costs. Strain set to worsen as BOE steps up fight on rising prices – Bloomberg

- [United Kingdom] Mortgage misery for millions following rate rise. 40% of fixed-rate deals will end this year, exposing borrowers to higher costs – FT

- [United Kingdom] London tenants facing ‘increasingly unaffordable’ rents. Shortage of accommodation results in private landlords and agents demanding that applicants bid to secure property – FT

- [United Kingdom] Mortgage wake-up call for middle classes. Rising interest rates could cost some borrowers more than rising energy bills – FT

- [United Kingdom] UK Residential Market Survey – RICS

On cross-country:

- Newsletter on credit risk: real estate and leveraged lending – BIS

- Beyond China: Here Are the Next Real Estate Markets to Drop – Barron’s

- Where Should Affluent People Live? it’s not a simple question – Freddie deBoer

On the US:

- Zillow Sees Slowing Demand for Ads in Housing Downturn. Shares fall after earnings forecast misses analyst estimates.

Posted by at 9:27 AM

Labels: Global Housing Watch

Thursday, August 11, 2022

How big is the housing shortage?

From Market Urbanism:

“Two teams of researchers recently released estimates of the U.S. housing shortage – and they differ by a factor of five. Is the national shortage 20 million homes or just 4 million? With a range that big, both published by pro-housing groups, you’d be forgiven for thinking this is an exercise in futility.

But look under the hood and each estimate is asking and answering a different question. Together they offer a useful parallax on the current cost crisis. To oversimplify, here’s how I’m thinking about the studies:

- America needs to find space for about 4 million more households.

- City housing deficits add up to about 20 million dwellings, but the total is less than the sum of the parts.

- If we deregulated everywhere, high-priced places would build much more housing than Up For Growth predicts. And moderate-priced places would build much less housing than the JEC predicts.

JEC: 20 million

The easier report to understand is that produced at the Joint Economic Committee by the classically-named duo Kevin Corinth and Hugo Dante, the latter a GMU/Mercatus alumnus. They use a straightforward supply and demand framework with some simple, defensible assumptions about the housing production function and the demand curve within each county.”

Continue reading here.

From Market Urbanism:

“Two teams of researchers recently released estimates of the U.S. housing shortage – and they differ by a factor of five. Is the national shortage 20 million homes or just 4 million? With a range that big, both published by pro-housing groups, you’d be forgiven for thinking this is an exercise in futility.

But look under the hood and each estimate is asking and answering a different question.

Posted by at 10:53 AM

Labels: Global Housing Watch

Subscribe to: Posts