Showing posts with label Global Housing Watch. Show all posts

Friday, July 12, 2019

Real Estate Prices in Portugal

From the IMF’s latest report on Portugal:

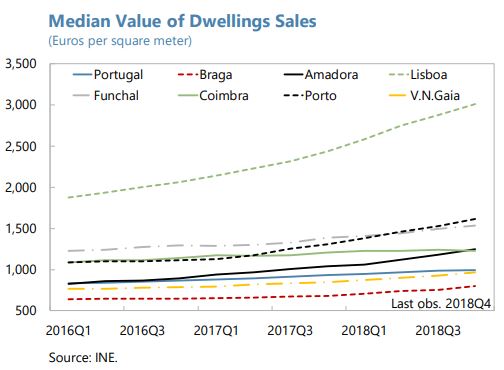

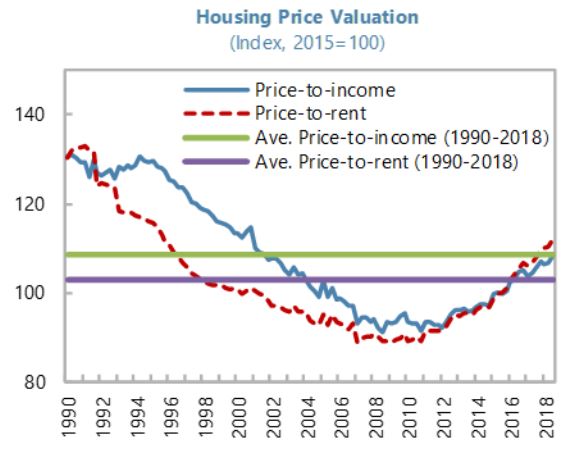

“Growth of the Portuguese House Price Index (HPI) decelerated to 9.3 percent y-o-y in 2018:Q4 from its 12.2 percent y-o-y peak in 2018:Q1. Price increases have been more pronounced for existing dwellings, rising 9.5 percent y-o-y in 2018:Q4 and, in particular, in Lisbon and Porto, with the median value per square meter increasing more than 23 percent y-o-y in 2018:Q4. Data from the OECD (…) indicate that the price-to-rent and price-to-income ratios are slightly above their 2000:Q1–2018:Q3 averages, which suggests that housing markets are not significantly overvalued.

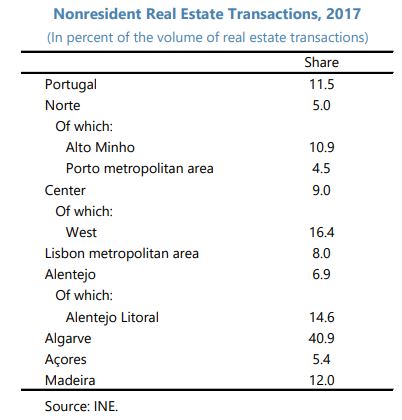

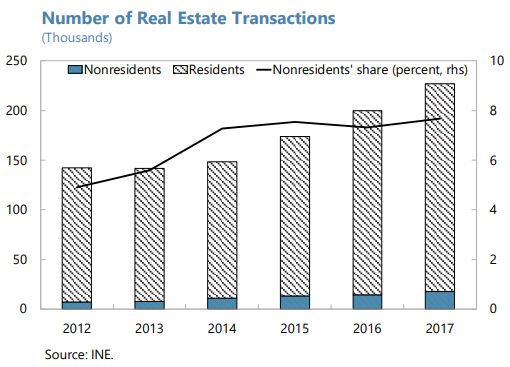

A significant part of the transactions driving real estate prices up in key locations are linked to the strong growth in the tourism sector and direct investments by non-residents. The share of purchases by nonresidents in the total number of transactions has strengthened from 2014 (…). Nonresidents were especially active in the higher end of the property market, with the share of nonresident purchases in the total value of transactions in the >€500k segment exceeding 35 percent during 2013–17. These indicators may understate the participation of foreign investors in the real estate market, because some buyers acquire resident status when they buy a property.”

From the IMF’s latest report on Portugal:

“Growth of the Portuguese House Price Index (HPI) decelerated to 9.3 percent y-o-y in 2018:Q4 from its 12.2 percent y-o-y peak in 2018:Q1. Price increases have been more pronounced for existing dwellings, rising 9.5 percent y-o-y in 2018:Q4 and, in particular, in Lisbon and Porto, with the median value per square meter increasing more than 23 percent y-o-y in 2018:Q4. Data from the OECD (…) indicate that the price-to-rent and price-to-income ratios are slightly above their 2000:Q1–2018:Q3 averages,

Posted by at 9:58 AM

Labels: Global Housing Watch

Housing View – July 12, 2019

On the US:

- Lots of folks over 65 are spending a lot on housing – Richard’s Real Estate and Urban Economics Blog

- To Encourage New Housing, Tax It – Wall Street Journal

- Meeting America’s Affordable Housing Needs Requires GSE Reform, and More – The Harvard Joint Center for Housing Studies

- Recession Signals: Home Sales Trend Lower in All Four Regions – Federal Reserve Bank of St. Louis

- A New Approach on Housing Affordability – New York Times

- Kamala Harris’ Plan To End the Racial Homeownership Gap Doubles Down on the Worst Aspects of U.S. Housing Policy – Reason

- Rebounds in Homeownership Have Not Reduced the Gap for Black Homeowners – The Harvard Joint Center for Housing Studies

- Democrats May Inflate Another Housing Bubble – Wall Street Journal

- Can This Factory Produce a Cheaper Apartment? – Citylab

- Don’t look now, but home equity delinquencies are rising – American Banker

On other countries:

- [Chile] Chile’s house prices are rising strongly – Global Property Guide

- [Portugal] Portugal Passes ‘Right to Housing’ Law As Prices Surge – Citylab

On the US:

- Lots of folks over 65 are spending a lot on housing – Richard’s Real Estate and Urban Economics Blog

- To Encourage New Housing, Tax It – Wall Street Journal

- Meeting America’s Affordable Housing Needs Requires GSE Reform, and More – The Harvard Joint Center for Housing Studies

- Recession Signals: Home Sales Trend Lower in All Four Regions – Federal Reserve Bank of St.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, July 11, 2019

Housing Market in the Euro Area

From the IMF’s latest report on the Euro Area:

“Macroprudential policies should be used more actively to manage financial vulnerabilities in both housing and corporate sectors. France, for example, has tightened large exposure limits for big French banks lending to highly indebted corporates, and some countries have increased their countercyclical capital buffers. However, bank-based tools cannot address risks arising from nonbank loans. As recommended in the 2018 FSAP, borrower-based tools could be legislated where they are currently unavailable, and used more proactively against risky firms and households. In particular a range of borrower-based tools for corporates (such as limits on loan-to-value ratios for commercial real estate, debt/equity caps and minimum ICRs) should be explored, and national macroprudential supervisors should have the authority to use these tools for all financial institutions. The authorities should also monitor liquidity risks in investment funds that are increasingly exposed to lower-grade corporate debt and real estate in search for yield. In order to be effective, comprehensive and comparable credit information systems need to be available in all countries. Urgently addressing data gaps in the area of commercial real estate and nonbank financial institutions is also needed to allow a fuller assessment of financial stability risks.”

From the IMF’s latest report on the Euro Area:

“Macroprudential policies should be used more actively to manage financial vulnerabilities in both housing and corporate sectors. France, for example, has tightened large exposure limits for big French banks lending to highly indebted corporates, and some countries have increased their countercyclical capital buffers. However, bank-based tools cannot address risks arising from nonbank loans. As recommended in the 2018 FSAP, borrower-based tools could be legislated where they are currently unavailable,

Posted by at 11:07 AM

Labels: Global Housing Watch

Wednesday, July 10, 2019

Housing Market in Germany

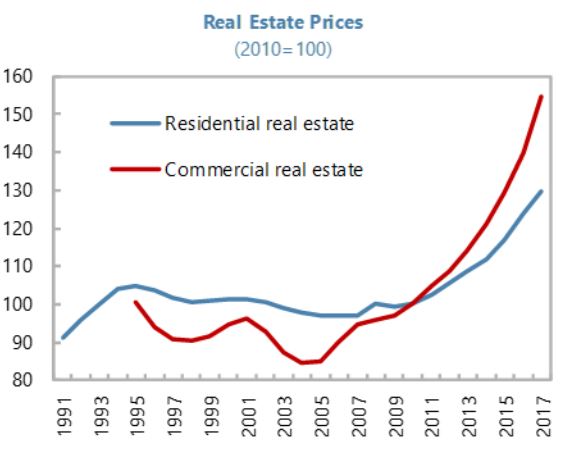

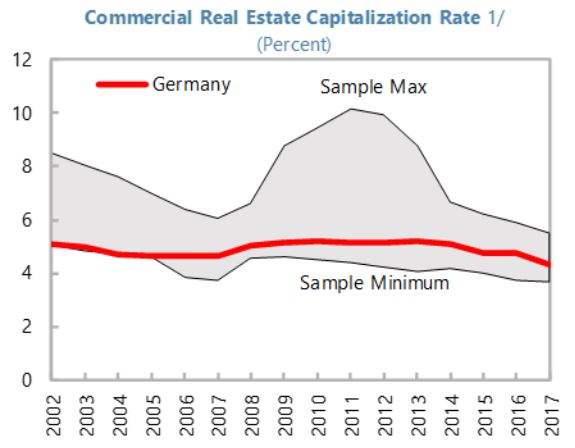

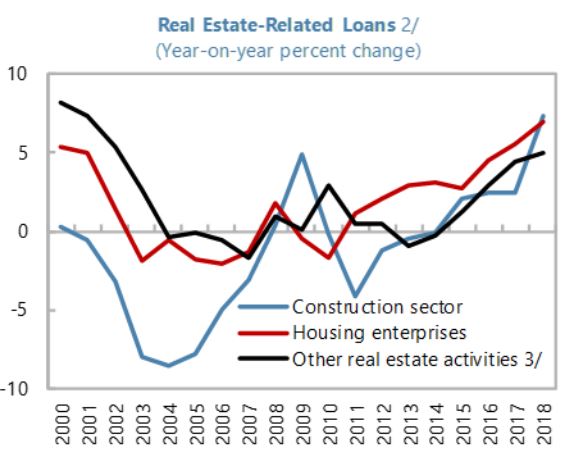

From the IMF’s latest report on Germany:

“Real estate prices continue to rise rapidly while aggregate credit growth remains in check.

- House prices in major cities have continued to rise rapidly, moving further into overvaluation territory. Staff analysis suggests that house prices were overvalued in Germany’s main cities, from 10–15 percent in Stuttgart and Dusseldorf to 25–30 percent in Hannover, Frankfurt and Hamburg and more than 40 percent in Munich in 2017.11 The government has stepped up efforts to increase housing supply, including by allocating €2 billion to build 100,000 new social housing units during 2020–21, selling federally-owned properties to local authorities at reduced prices to build affordable housing, and providing a special depreciation allowance for new rental housing construction. The impact on house prices, however, is expected to be limited.

- Commercial real estate (CRE) prices have risen even faster than house prices (…) with a moderate decline in the yield on CRE investment (…). Price increases have been particularly large in the office sub-segment and banks’ exposure to the sector has risen over the last three years, despite the sizable share of equity-based and foreign-financed investment.

- These rapid price increases have not yet been accompanied by strong increases in credit growth at the aggregate level. Credit growth accelerated to a pace slightly exceeding nominal GDP growth, but the credit-to-GDP ratio remains low from a historical perspective and compared with other advanced economies. Bank lending to CRE-related activities also appears relatively small compared to the EU average, yet the impact of a sharp decline in CRE prices on bank balance sheets could still be important as defaults on CRE tend to be higher than those on residential real estate.

Additional macroprudential action is needed to guard against imbalances in the real estate sector.

- Urgently address data gaps. The Bank Lending Survey suggests that LTV ratios for new mortgage loans have been relatively stable on an aggregate basis (…), yet lack of granular loan information hinders a full assessment of potential financial stability risks in specific market segments. It is essential that these data gaps be addressed.

- Consider prompt activation of the existing borrower-based measures. Absent granular data alongside the prolonged rise in house prices, the authorities should consider implementing an LTV cap and amortization requirements on mortgages.

- Expand the macroprudential toolkit. Germany currently lacks income-based instruments for residential and CRE lending or other borrowerbased instruments for CRE lending. The authorities should consider introducing income-based instruments, such as a debt-toincome or debt-service-to-income cap. In addition, appropriate instruments for CRE should also be considered, taking into account diverse financing structures. As the government is currently reviewing the effectiveness of existing instruments, this is a right time to consider expanding the toolkit.”

From the IMF’s latest report on Germany:

“Real estate prices continue to rise rapidly while aggregate credit growth remains in check.

- House prices in major cities have continued to rise rapidly, moving further into overvaluation territory. Staff analysis suggests that house prices were overvalued in Germany’s main cities, from 10–15 percent in Stuttgart and Dusseldorf to 25–30 percent in Hannover, Frankfurt and Hamburg and more than 40 percent in Munich in 2017.11 The government has stepped up efforts to increase housing supply,

Posted by at 12:11 PM

Labels: Global Housing Watch

Friday, July 5, 2019

Housing View – July 5, 2019

On cross-country:

- For now, residential-property prices are likely to keep rising – The Economist

- Rate cuts cannot curb property boom and bust – Financial Times

- Not just San Francisco: City housing markets all over the world are far too expensive – MarketWatch

- Why financialisation is not causing the housing crisis – Centre for Cities

On the US:

- Waiting for Affordable Housing in New York City – NBER

- Fewer Renters Believe They Are Likely to Ever Own a Home – Wall Street Journal

- Do land use restrictions increase restaurant quality and diversity? – American Enterprise Institute

- A City’s Bold Housing Plan – New York Times

- Changing supply elasticities and regional housing booms – Norges Bank

- I am Jane. Do I pay more in the housing market? – IDEAS

- AEI Housing Market Indicators release on March 2019 data – American Enterprise Institute

- The Government Created Housing Segregation. Here’s How the Government Can End It. – The American Prospect

- Housing: Elizabeth Warren v. John Cochrane – Econospeak

- Oregon Legislature Votes To Essentially Ban Single-Family Zoning – NPR

- The next housing bubble could come from this technology – Los Angeles Times

- The US Housing Finance System: A Flawed Giant – Harvard Joint Center for Housing Studies

- Housing affordability and quality create stress for Heartland families – Brookings Institute

- The Great Price Deceleration – John Burns

On other countries:

- [Brazil] Brazil’s house prices continue to fall – Global Property Guide

- [Egypt] Egypt’s house prices falling sharply – Global Property Guide

- [Macao] Macau’s amazing, incredible, soaring property prices – Global Property Guide

- [Netherlands] Brexit fuels Amsterdam property price boom – Financial Times

- [Singapore] Singapore to Keep Property Curbs for Now as Sell-Off Risk Remote – Bloomberg

- [United Kingdom] Speech by Communities Secretary Rt Hon James Brokenshire MP at the Chartered Institute of Housing conference – GOV

On cross-country:

- For now, residential-property prices are likely to keep rising – The Economist

- Rate cuts cannot curb property boom and bust – Financial Times

- Not just San Francisco: City housing markets all over the world are far too expensive – MarketWatch

- Why financialisation is not causing the housing crisis – Centre for Cities

On the US:

- Waiting for Affordable Housing in New York City – NBER

- Fewer Renters Believe They Are Likely to Ever Own a Home – Wall Street Journal

- Do land use restrictions increase restaurant quality and diversity?

Posted by at 9:29 AM

Labels: Global Housing Watch

Subscribe to: Posts