Showing posts with label Global Housing Watch. Show all posts

Sunday, August 20, 2017

Housing Finance and Real Estate Markets in Colombia

A new IMF working paper on Colombia says that:

“Overall, risks from the housing market seem to be contained. While the results from the VAR model suggest that a negative house price shock could have sizable implications on activity (GDP, consumption and investment), house prices do not seem to be largely above levels justified by economic fundamentals (the average estimated gap is at 13 percent). Moreover, after the 1999 financial crisis the authorities have adopted macroprudential measures such as the use of LTV limits, which together with other housing financing characteristics, limit the vulnerabilities stemming from the housing market. At the same time, the current slowdown in economic activity should decelerate mortgage growth and impact the growth of house prices, which has started to show some signs of weakening. However, the authorities should continue to monitor closely the developments in credit and house price growth.”

A new IMF working paper on Colombia says that:

“Overall, risks from the housing market seem to be contained. While the results from the VAR model suggest that a negative house price shock could have sizable implications on activity (GDP, consumption and investment), house prices do not seem to be largely above levels justified by economic fundamentals (the average estimated gap is at 13 percent). Moreover, after the 1999 financial crisis the authorities have adopted macroprudential measures such as the use of LTV limits,

Posted by at 6:40 PM

Labels: Global Housing Watch

Friday, August 18, 2017

Housing View – August 18, 2017

On cross-country:

- Housing for the long run? – Financial Times

- Construction: How to build more efficiently – The Economist

- The construction industry: Least improved – The Economist

On the US:

- Worst Case Housing Needs: 2017 Report to Congress – U.S. Department of Housing and Urban Development

- Housing is too expensive for low-skilled workers to move to cities with the highest-paid jobs – Quartz

- S. Housing: The (Young) Kids Are Alright – Roubini Global Economics

- Banking integration and house price comovement – European Systemic Risk Board

- NY Fed President Wants Consumers to Tap Home Equity: Didn’t We Try That Before? – MishTalk

- Affordable Housing Regulations Crushing New Home Construction in L.A. – Reason

On other countries:

- [Australia] Speech on Some Innovative Mortgage Data – Reserve Bank of Australia

- [Australia] Monthly Property Update – CoreLogic

- Assessing China’s Residential Real Estate Market – IMF

- [China] Home Purchase Restriction and Housing Price: A Distribution Dynamics Analysis – Regional Science and Urban Economics

- [Netherlands] Regional house price differences are widening: Dutch Housing Market Quarterly – Rabobank

- [Spain] What has happened in Spain? The real estate bubble, corruption and housing development: A view from the local level – Geoforum

- [United Kingdom] Residential Market Outlook – Cluttons

- [United Kingdom] London mayor targets developers over affordable housing obligations – Financial Times

On cross-country:

- Housing for the long run? – Financial Times

- Construction: How to build more efficiently – The Economist

- The construction industry: Least improved – The Economist

On the US:

- Worst Case Housing Needs: 2017 Report to Congress – U.S. Department of Housing and Urban Development

- Housing is too expensive for low-skilled workers to move to cities with the highest-paid jobs – Quartz

- S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, August 15, 2017

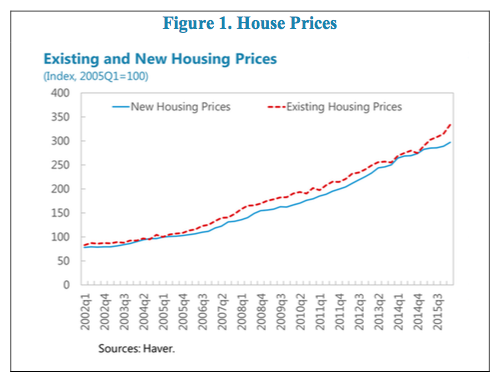

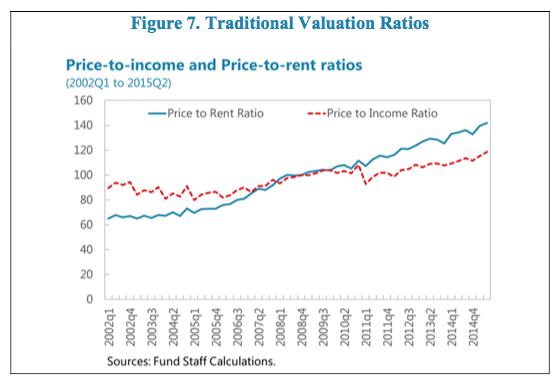

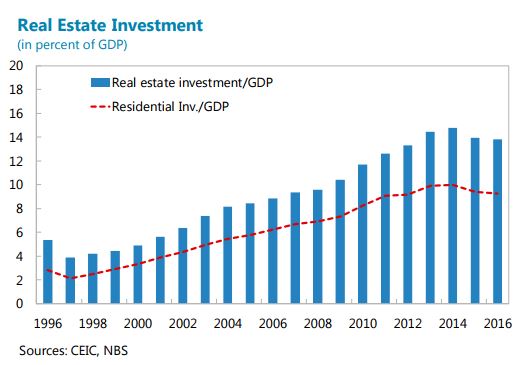

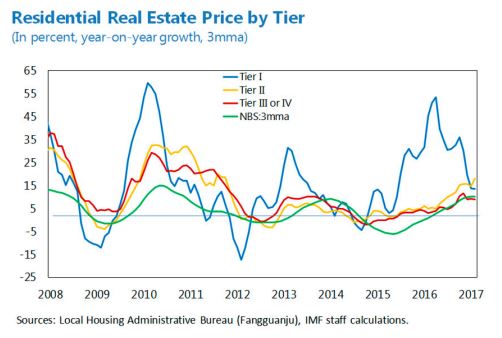

Assessing China’s Residential Real Estate Market

A new IMF report on China says:

- “China’s real estate market rebounded sharply after a temporary slowdown in 2014-2015. The tightening measures since late 2016 seem to have dampened market activity, but house prices and sales remain strong, particularly in smaller cities.”

- “Risks are significant on the downside. If house prices rise further beyond “fundamental” levels and the bubble expands to smaller cities, it would increase the likelihood and costs of a sharp correction, which would weaken overall growth, undermine financial stability, reduce local government spending room, and spur capital outflows.”

- “To stave off such risks, the increasing intensity of macro-prudential and city-specific policies is appropriate, given the diversity in housing conditions, and should continue to be deployed to ensure a smooth adjustment. The government should expand its toolkit to include additional macroprudential measures including more active use of debt servicing-to-income (DSTI) caps and capital requirements on banks’ exposure to the real estate sector.”

- “A longer-term solution to manage better the frequent house price cycles is to introduce recurrent property taxes, resolve land supply constraints in large cities, mitigate local governments’ reliance on land sales, and accelerate reforms of the social security and “hukou” systems.”

A new IMF report on China says:

- “China’s real estate market rebounded sharply after a temporary slowdown in 2014-2015. The tightening measures since late 2016 seem to have dampened market activity, but house prices and sales remain strong, particularly in smaller cities.”

- “Risks are significant on the downside. If house prices rise further beyond “fundamental” levels and the bubble expands to smaller cities, it would increase the likelihood and costs of a sharp correction,

Posted by at 9:28 AM

Labels: Global Housing Watch

Friday, August 11, 2017

Housing View – August 11, 2017

On cross-country:

- Prime Global Cities Index – Knight Frank

On the US:

- Stabilizing the System of Mortgage Finance in the United States – IMF

- Robert Shiller on The Transformation of the ‘American Dream’ – New York Times

- Was there a Housing Price Bubble? Revisited – Marginal Revolution

- Appraising Home Purchase Appraisals – Federal Reserve Bank of Philadelphia

- Finding Common Ground for Land-Use Regulation Reform – Cato Institute

- Significant Improvements in Energy Efficiency Characteristics of the US Housing Stock – Harvard Joint Center for Housing Studies

- Housing Sentiment Dips as High Home Prices Weigh on Buyers and Economic Conditions Weigh on Sellers – Fannie Mae

On other countries:

- [Australia] Mapping the market shows a substantial decline in affordable housing supply in Sydney and Melbourne over the past five years – CoreLogic

- [Canada] New mortgages continue to rise in Canada – CMHC

- [United Kingdom] Housing is a growing political problem for the Conservatives – The Economist

- [United Kingdom] How to solve Britain’s housing crisis – The Economist

On cross-country:

- Prime Global Cities Index – Knight Frank

On the US:

- Stabilizing the System of Mortgage Finance in the United States – IMF

- Robert Shiller on The Transformation of the ‘American Dream’ – New York Times

- Was there a Housing Price Bubble? Revisited – Marginal Revolution

- Appraising Home Purchase Appraisals – Federal Reserve Bank of Philadelphia

- Finding Common Ground for Land-Use Regulation Reform – Cato Institute

- Significant Improvements in Energy Efficiency Characteristics of the US Housing Stock – Harvard Joint Center for Housing Studies

- Housing Sentiment Dips as High Home Prices Weigh on Buyers and Economic Conditions Weigh on Sellers – Fannie Mae

On other countries:

- [Australia] Mapping the market shows a substantial decline in affordable housing supply in Sydney and Melbourne over the past five years – CoreLogic

- [Canada] New mortgages continue to rise in Canada – CMHC

- [United Kingdom] Housing is a growing political problem for the Conservatives – The Economist

- [United Kingdom] How to solve Britain’s housing crisis – The Economist

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, August 8, 2017

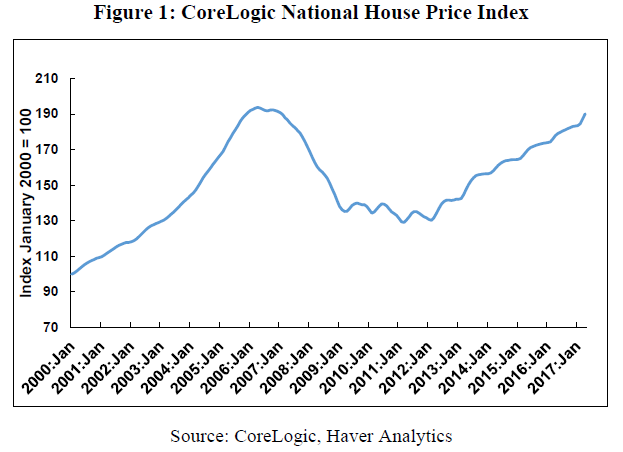

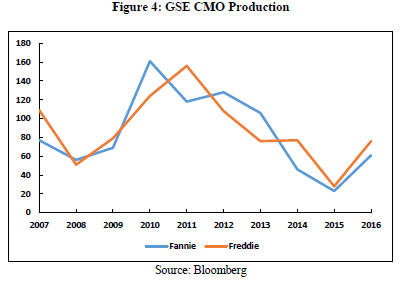

Stabilizing the System of Mortgage Finance in the United States

A new IMF Working Paper by Richard Koss says that “It has been over a decade since the peak of house prices in the US was attained, and while there has been a concerted regulatory response to the subsequent collapse, the two Government Sponsored Enterprises (GSEs) remain in conservatorship. While this action served to forestall a deeper crisis at the time, over the past several years risks related to the system of mortgage finance can be seen building across several dimensions that need to be addressed. While reforms to the GSEs are an important part of dealing with these concerns, this paper argues that broader changes need to be made across the entire mortgage landscape to stabilize the system, even before the final state of the GSEs is fully determined.”

Continue reading here.

A new IMF Working Paper by Richard Koss says that “It has been over a decade since the peak of house prices in the US was attained, and while there has been a concerted regulatory response to the subsequent collapse, the two Government Sponsored Enterprises (GSEs) remain in conservatorship. While this action served to forestall a deeper crisis at the time, over the past several years risks related to the system of mortgage finance can be seen building across several dimensions that need to be addressed.

Posted by at 4:12 PM

Labels: Global Housing Watch

Subscribe to: Posts