Tuesday, August 15, 2017

Assessing China’s Residential Real Estate Market

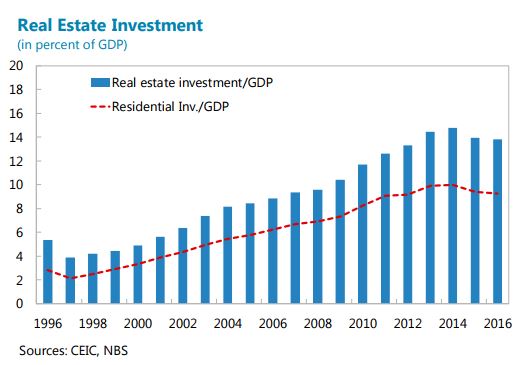

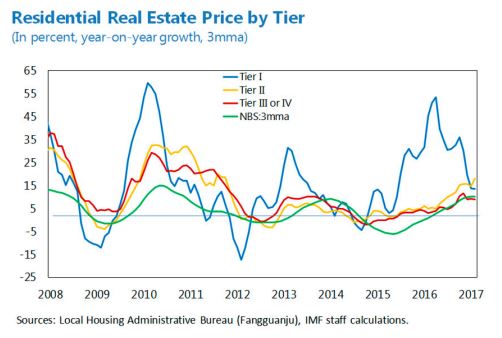

A new IMF report on China says:

- “China’s real estate market rebounded sharply after a temporary slowdown in 2014-2015. The tightening measures since late 2016 seem to have dampened market activity, but house prices and sales remain strong, particularly in smaller cities.”

- “Risks are significant on the downside. If house prices rise further beyond “fundamental” levels and the bubble expands to smaller cities, it would increase the likelihood and costs of a sharp correction, which would weaken overall growth, undermine financial stability, reduce local government spending room, and spur capital outflows.”

- “To stave off such risks, the increasing intensity of macro-prudential and city-specific policies is appropriate, given the diversity in housing conditions, and should continue to be deployed to ensure a smooth adjustment. The government should expand its toolkit to include additional macroprudential measures including more active use of debt servicing-to-income (DSTI) caps and capital requirements on banks’ exposure to the real estate sector.”

- “A longer-term solution to manage better the frequent house price cycles is to introduce recurrent property taxes, resolve land supply constraints in large cities, mitigate local governments’ reliance on land sales, and accelerate reforms of the social security and “hukou” systems.”

Posted by at 9:28 AM

Labels: Global Housing Watch

Subscribe to: Posts